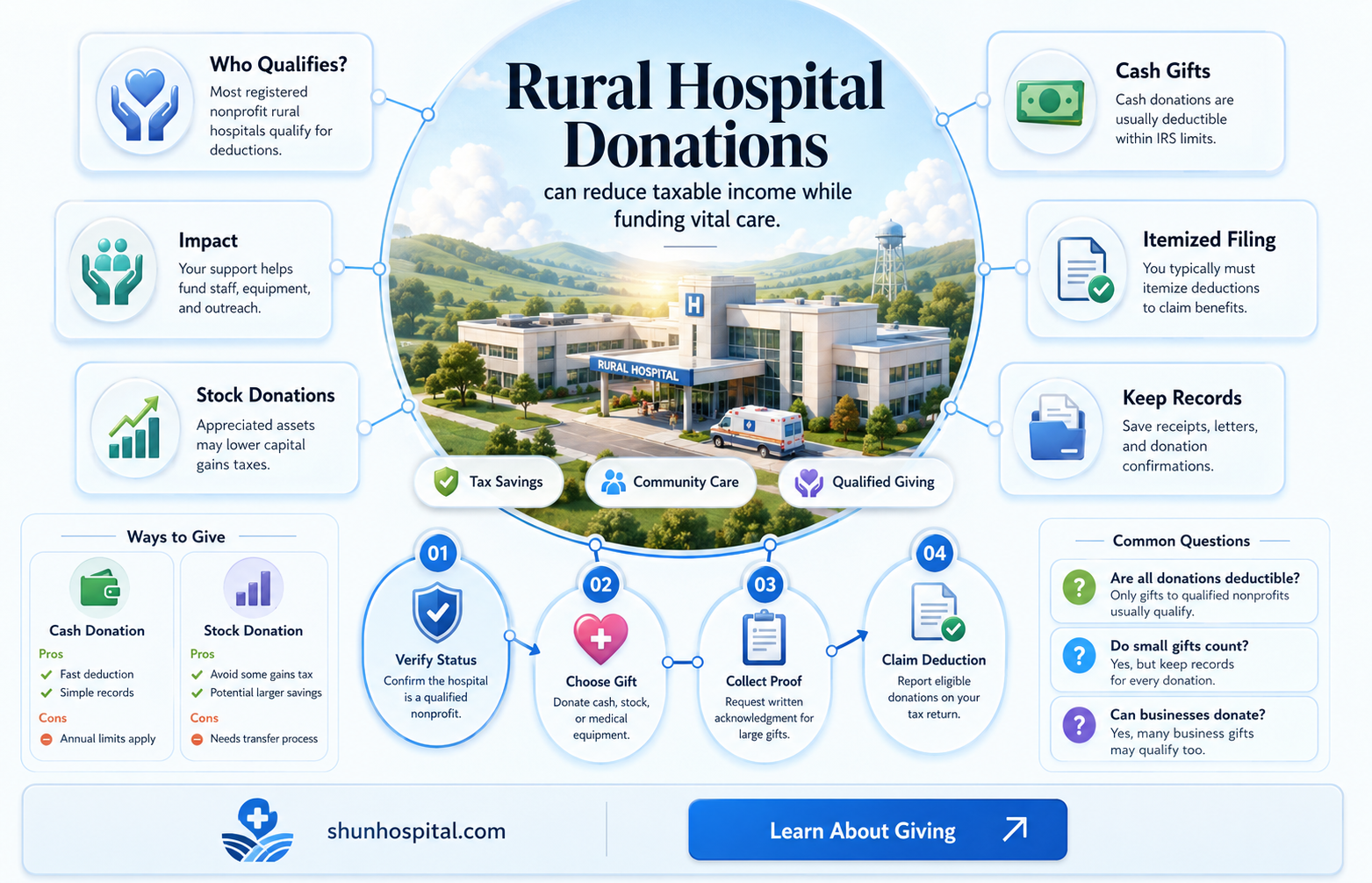

Rural hospitals in the United States often face financial difficulties and rely on various funding sources, including government programs and private donations, to stay afloat. In recognition of the unique challenges faced by these hospitals, some states have introduced tax credit programs to encourage donations. These programs offer incentives for individuals and businesses to contribute to rural hospitals by providing tax breaks or credits against their state income tax liability. One example is Georgia's Rural Hospital Tax Credit Program, which allows taxpayers to receive credits against their Georgia income tax when they donate to eligible rural hospitals within the state. These tax credit programs can help improve access to healthcare in underserved rural communities and ensure the continued operation of vital medical facilities.

| Characteristics | Values |

|---|---|

| Location | Georgia |

| Effective Date | January 1, 2025 |

| Annual Aggregate Amount of Tax Credits | $100 million |

| Maximum Contribution by Individual Owners of Pass-Through Entities | $25,000 in the first six months of the year |

| Payment Deadlines | Within 180 days after DOR preapproval for taxpayers preapproved by DOR on or before September 30 |

| Tax Credit Program | Georgia HEART Hospital Tax Credit Program |

| Tax Credit Limit | $4 million annual contribution limit per hospital |

| Unused Tax Credit | Can be used against the taxpayer's succeeding five years' tax liability |

| Use of Donor Contributions by RHOs | Must be used for healthcare-related purposes, including capital expenditures facilitating healthcare-related services |

| Reporting Requirements for RHOs | Annual reporting on the use of contributions to the DCH |

Explore related products

$13.9 $25

What You'll Learn

![]()

The Georgia Rural Hospital Tax Credit Program

Each year, the Georgia Department of Community Health (DCH) posts an updated list of eligible organizations by financial need and in alphabetical order, along with updated timelines. To be included on the list, each eligible organization must submit a financial proxy form (990) to the DCH, as well as a five-year viability and stability plan.

For more information about the Georgia Rural Hospital Tax Credit Program, individuals can visit www.georgiaheart.org or contact Georgia HEART staff at [email protected].

Stockton County Hospital: Alignment Insurance Coverage

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-One]: Start & Grow Your Business While Saving on Taxes – Insider Strategies, Bookkeeping Hacks & Smart Accounting Tips](https://m.media-amazon.com/images/I/61QksxYPu+L._AC_UL320_.jpg)

![]()

Tax credits for contributions to rural hospitals

In Georgia, taxpayers who contribute to rural hospitals may be eligible for tax credits under the Georgia HEART hospital tax credit program. This program was established under the Georgia Rural Hospital Tax Credit Program, which came into effect on January 1, 2017. The program offers taxpayers the opportunity to receive a Georgia income tax credit in exchange for their contributions to eligible rural hospitals.

To participate in the program, taxpayers must be pre-approved by the Georgia Department of Revenue (DOR). There are limits to the total amount of tax credits available, which is currently $100 million annually. Individual owners of pass-through entities, such as limited liability companies or Subchapter 'S' corporations, can contribute up to $25,000 in the first six months of the year. After this period, contributions from this taxpayer type are unlimited.

Taxpayers can estimate their potential Georgia income tax liability by reviewing their prior year's Georgia income tax return (Form 500) and consulting with tax professionals. If taxpayers pay their Georgia income taxes on a quarterly basis, they can reduce a portion of each payment by contributing to a HEART Rural Hospital Organization (RHO) within the same year. Any unused tax credit may be carried forward and applied against the taxpayer's succeeding five years of tax liability but cannot be used for prior years.

RHOs are required to use the contributions for healthcare-related purposes, including capital expenditures that facilitate the provision of healthcare services. They must report annually to the Georgia Department of Community Health (DCH) on how they have utilized the contributions, and the DCH, in turn, reports this information to lawmakers.

Tewksbury to Winchester Hospital: How Far Is It?

You may want to see also

Explore related products

![]()

HEART program tax credits

In Georgia, taxpayers can receive a state income tax credit for 100% of the amount they contribute to qualified rural hospital organisations (RHOs) under the Georgia HEART Hospital Program. The program is designed to financially support rural hospitals in the state at no cost to taxpayers.

The Georgia HEART program is limited to rural hospitals that meet specific qualification criteria, including county population size (50,000 or fewer, excluding military personnel), tax-exempt status or public hospital authority management, acceptance of Medicare and Medicaid, and a minimum annual provision of indigent or uncompensated care. To qualify, rural hospitals must file a five-year plan with the Georgia Department of Community Health (DCH).

From 2018 to 2022, Georgia taxpayers could access $60 million of RHO tax credits each year, with each qualified RHO having access to $4 million of tax credits. In 2023, the cap on RHO tax credits was increased to $75 million annually, with each qualified RHO still having access to $4 million of tax credits. During the first six months of each year, a qualified RHO may only accept $2 million of corporate contributions and $2 million of individual contributions. After June 30 of each year, as long as tax credits are available, individual taxpayers may make unlimited contributions to RHOs for a corresponding 100% Georgia income tax credit.

For example, if you contribute $1,200 to a HEART RHO in March, you will receive a corresponding Georgia income tax credit. Normally, you would make an estimated income tax payment to the state of $2,500 on April 15, June 15, September 15, and January 15 (of the following year). However, because you redirected $1,200 of your Georgia income tax payments to a HEART RHO, you can reduce each of these estimated income tax payments by $300 ($1,200 divided by four). As a result, your new quarterly estimated income tax payment due to the state of Georgia will be $2,200.

Hospitals and Their Cash Reserves: A Mystery

You may want to see also

Explore related products

![]()

Annual contribution limits

In the United States, contributions to charitable organizations may be tax-deductible. The Internal Revenue Service (IRS) outlines the rules for tax deductions for charitable contributions. The amount of charitable cash contributions that taxpayers can deduct is usually limited to a percentage of their adjusted gross income (AGI). For most taxpayers, this percentage is 60% of their AGI. However, qualified contributions are not subject to this limitation, and individuals may deduct qualified contributions of up to 100% of their AGI. Corporations may deduct qualified contributions of up to 25% of their taxable income, and any excess contributions can be carried over to the next tax year.

Contributions must be made in cash or other property before the end of the tax year to be deductible. If a taxpayer donates property other than cash to a qualified organization, they can typically deduct the fair market value of the property. However, if the property has appreciated in value, adjustments may need to be made, as outlined in Publication 561 by the IRS. It's important to note that contributions of non-cash property do not qualify for unlimited deductions like cash contributions.

There are different rules and limitations for contributions to specific types of organizations. For example, contributions to certain private foundations, veterans' organizations, fraternal societies, and cemetery organizations are limited to 30% of the taxpayer's AGI. Additionally, a special rule allows businesses to claim enhanced deductions for contributions of food inventory for the care of the ill, needy, or infants. The deductible amount for such contributions is usually limited to 15% of the taxpayer's aggregate net income or taxable income. In 2020, businesses could deduct up to 25% of their aggregate net income or taxable income for contributions of food inventory.

Furthermore, some states have specific programs and tax credits for contributions to rural hospitals. For example, Georgia has the Georgia HEART Hospital Program, which allows taxpayers to receive a Georgia income tax credit for contributions to eligible rural hospitals. The annual aggregate amount of tax credits allowed under this program is $100 million. Individual owners of pass-through entities can contribute up to $25,000 in the first six months of the year, and contributions from this taxpayer type are unlimited in the second half. Additionally, pass-through businesses may contribute through the HEART program at the same limits as C Corporations during the first six months of the year.

Hospital Indemnity Plans: Deductible or No Deductible?

You may want to see also

Explore related products

![]()

Reporting requirements for RHOs

The reporting requirements for Rural Housing Organisations (RHOs) can vary depending on the state and the specific programs in question. However, there are some standard reporting obligations that all RHOs must fulfil.

Firstly, financial transparency is crucial, and RHOs are typically required to submit financial proxy forms (990) to the relevant state department, such as the Georgia Department of Community Health (DCH). This ensures that the organisation's finances are in order and that they are compliant with tax regulations.

Secondly, RHOs often need to demonstrate long-term viability and stability. This is usually done by submitting a five-year plan to the appropriate department, outlining their financial projections and operational strategies. This plan is essential for maintaining their tax status and securing funding.

Additionally, RHOs are subject to the same reporting requirements as other hospitals regarding public health emergencies. For example, during the COVID-19 Public Health Emergency (PHE), the CDC, CMS, and ASPR mandated reporting requirements for all hospitals to maintain situational awareness and address patient needs. These requirements included regular reporting on confirmed infections and bed capacity.

Furthermore, RHOs must adhere to any state-specific reporting mandates. For instance, the Georgia Rural Hospital Tax Credit Program requires eligible organisations to submit Donation and Expenditure Forms annually. These forms outline the financial contributions and allocations of the RHO, ensuring compliance with tax credit regulations.

Overall, RHOs have a responsibility to maintain detailed records and submit various reports to remain compliant with state and federal regulations. These reporting requirements are essential to ensure the organisations' financial stability, operational effectiveness, and ability to serve their communities effectively.

Pacifiers at the Hospital: Are They Necessary?

You may want to see also

Frequently asked questions

Yes, the Georgia Rural Hospital Tax Credit Program allows tax credits for contributions made to rural hospitals.

Taxpayers who wish to participate in the Georgia HEART hospital tax credit program must be pre-approved by the Georgia Department of Revenue (DOR). Taxpayers can determine their potential Georgia income tax liability by looking at their Georgia income tax return (Form 500) for their income tax liability for the prior tax year and estimating their tax liability accordingly.

Yes, rural hospital organizations (RHOs) must use contributions for healthcare-related purposes, including capital expenditures that facilitate the provision of healthcare services. RHOs must report how they used the contributions to the Georgia Department of Community Health (DCH) annually.

Yes, any unused tax credit may be carried over and used against the taxpayer's succeeding five years' tax liability. However, it cannot be applied against prior years' tax liability.