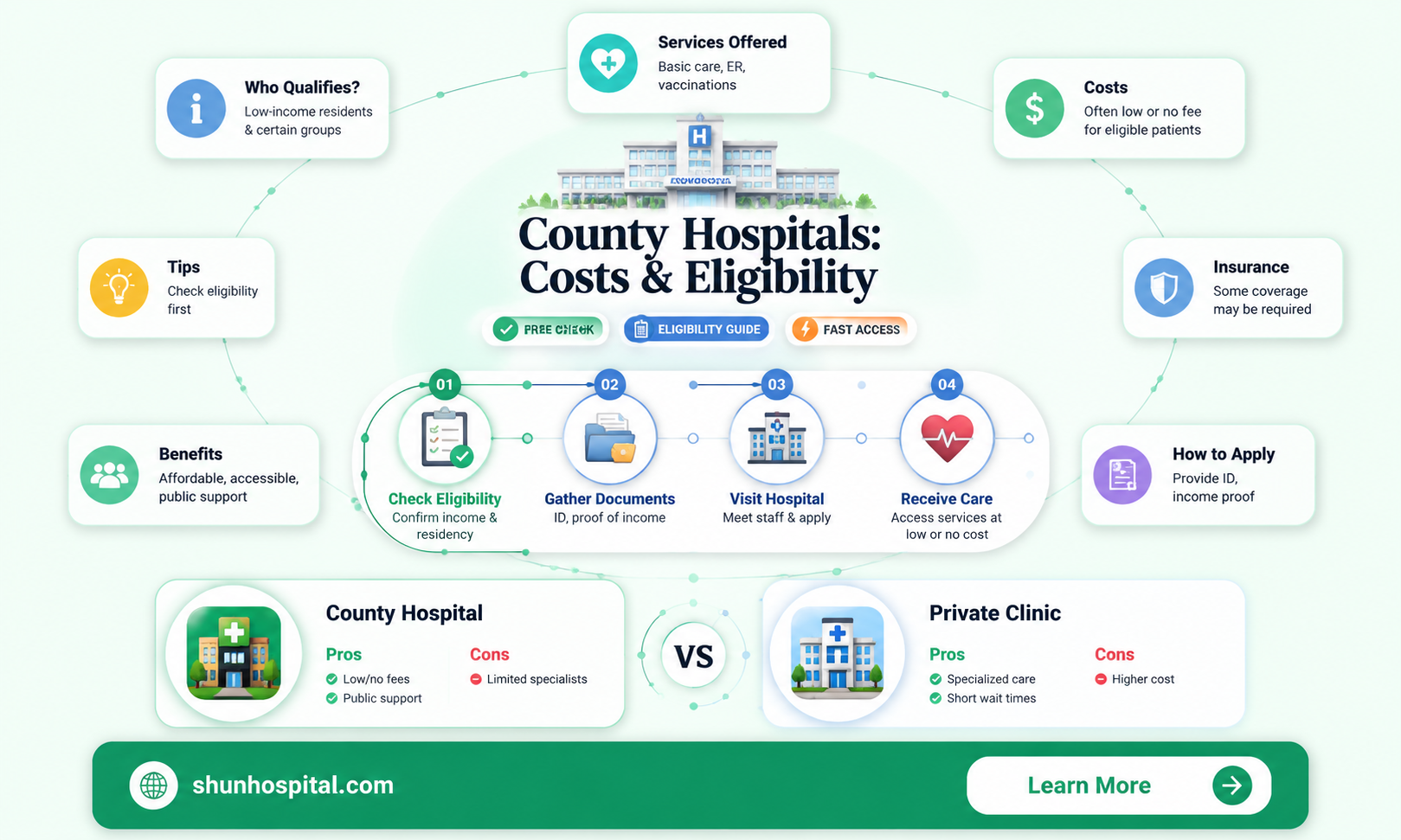

The question of whether county hospitals are free is a common one, often stemming from the assumption that publicly funded institutions offer cost-free services. County hospitals, typically operated by local governments, primarily serve to provide healthcare to underserved populations, including those without insurance. While they often offer sliding-scale fees or financial assistance programs based on income, they are not entirely free. Patients may still incur charges for services, though these are generally more affordable than private hospitals. Understanding the financial structure of county hospitals is crucial for individuals seeking accessible healthcare, as it helps manage expectations and plan for potential costs.

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for free hospital care based on income, insurance, or medical condition

- Government Programs: How Medicaid, Medicare, or state-funded programs cover hospital costs for eligible individuals

- Emergency Care: Legal requirements for hospitals to provide free emergency treatment regardless of payment ability

- Charity Care: Hospitals offering free or discounted services to low-income, uninsured patients

- Hidden Costs: Potential fees for medications, tests, or follow-up care not covered by free programs

![]()

Eligibility Criteria: Who qualifies for free hospital care based on income, insurance, or medical condition

In the United States, the eligibility criteria for free hospital care are primarily governed by federal and state programs, with income, insurance status, and medical condition serving as the cornerstone determinants. For instance, individuals with incomes at or below 138% of the federal poverty level (FPL) in Medicaid expansion states may qualify for Medicaid, which covers a broad range of hospital services. However, eligibility thresholds vary by state, with some setting lower income limits or imposing additional requirements. Understanding these nuances is crucial, as they dictate whether a patient can access free or subsidized care.

To navigate these criteria effectively, consider the following steps. First, assess your household income relative to the FPL, which is updated annually. For example, in 2023, the FPL for a single individual is $14,580, while for a family of four, it is $30,000. If your income falls below these thresholds, you may qualify for Medicaid or other state-specific programs. Second, evaluate your insurance status. Uninsured individuals often face stricter eligibility requirements but may still qualify for free care through hospital charity programs, which typically require proof of income and assets. Lastly, certain medical conditions, such as chronic illnesses or emergency cases, may expedite eligibility, especially under programs like Emergency Medicaid for undocumented immigrants in need of urgent care.

A comparative analysis reveals disparities in eligibility criteria across states. For example, in California, the income limit for Medicaid (Medi-Cal) is higher than in Texas, which has not expanded Medicaid under the Affordable Care Act. This means a family of three earning $28,000 annually might qualify in California but not in Texas. Additionally, some states offer more lenient criteria for specific populations, such as pregnant women or children, under programs like CHIP (Children’s Health Insurance Program). These variations underscore the importance of researching state-specific guidelines to determine eligibility accurately.

Persuasively, it’s worth noting that hospitals are legally obligated under the Emergency Medical Treatment and Labor Act (EMTALA) to provide emergency care regardless of ability to pay. However, this does not equate to free ongoing treatment. To secure long-term free care, patients must proactively apply for programs like Medicaid or hospital financial assistance. Practical tips include gathering all necessary documentation (e.g., pay stubs, tax returns) before applying and contacting hospital financial counselors for guidance. For those with partial insurance coverage, negotiating bills or applying for charity care can reduce out-of-pocket costs significantly.

In conclusion, eligibility for free hospital care hinges on a complex interplay of income, insurance, and medical condition, with significant variations by state and program. By understanding these criteria and taking proactive steps, individuals can maximize their chances of accessing the care they need without incurring overwhelming costs. Whether through Medicaid, state-specific programs, or hospital charity care, informed navigation of these systems is key to securing financial relief in healthcare.

Medieval England: Hospitals and Healthcare

You may want to see also

Explore related products

![]()

Government Programs: How Medicaid, Medicare, or state-funded programs cover hospital costs for eligible individuals

In the United States, hospital costs can be a significant financial burden, but government programs like Medicaid, Medicare, and state-funded initiatives provide essential coverage for eligible individuals. These programs are designed to ensure that low-income families, seniors, and people with disabilities have access to necessary healthcare services without facing overwhelming expenses. For instance, Medicaid, a joint federal and state program, covers a broad range of medical services, including hospital stays, doctor visits, and prescription drugs, for those who meet income and asset criteria. Eligibility varies by state, but generally, individuals earning up to 138% of the federal poverty level may qualify, offering a lifeline to millions who might otherwise forgo care due to cost.

Medicare, on the other hand, primarily serves individuals aged 65 and older, as well as younger people with certain disabilities or end-stage renal disease. It is divided into parts, with Part A covering hospital stays, skilled nursing facility care, and hospice care, often with no monthly premium for those who have paid Medicare taxes for at least 10 years. Part B covers outpatient services and requires a monthly premium, while Part D helps with prescription drug costs. Understanding these distinctions is crucial, as gaps in coverage can still leave beneficiaries with out-of-pocket expenses, such as deductibles and copayments. For example, while Part A covers hospital stays, it only pays for the first 60 days in full, after which beneficiaries must pay a daily coinsurance fee.

State-funded programs further bridge gaps in coverage by offering additional assistance to those who may not qualify for Medicaid or Medicare but still struggle with healthcare costs. These programs often target specific populations, such as children, pregnant women, or individuals with chronic conditions. For instance, the Children’s Health Insurance Program (CHIP) provides low-cost health coverage for children in families who earn too much to qualify for Medicaid but cannot afford private insurance. Similarly, some states offer programs like Medicaid buy-in options for working individuals with disabilities, allowing them to maintain healthcare coverage while employed. These state initiatives highlight the importance of localized solutions in addressing healthcare disparities.

To maximize the benefits of these programs, eligible individuals should take proactive steps to understand their coverage and explore additional resources. For Medicaid and Medicare beneficiaries, enrolling in supplemental plans, such as Medicare Advantage or Medigap policies, can help reduce out-of-pocket costs. Additionally, many states offer programs to help with premiums, copayments, and deductibles for those with limited incomes. Practical tips include regularly reviewing eligibility criteria, as changes in income or family size may affect coverage, and staying informed about annual enrollment periods to make necessary adjustments to plans. By leveraging these government programs effectively, individuals can significantly reduce the financial strain of hospital costs and access the care they need.

A comparative analysis of these programs reveals their complementary roles in the healthcare system. While Medicare provides a safety net for seniors and certain disabled individuals, Medicaid and state-funded programs address the needs of low-income populations across all age groups. Together, they form a multifaceted approach to ensuring healthcare accessibility, though challenges remain, such as varying eligibility criteria across states and gaps in coverage for certain services. For example, Medicaid expansion under the Affordable Care Act has increased access in many states, but not all states have adopted it, leaving some low-income individuals without coverage. Despite these limitations, these programs remain vital in making hospital care more affordable and accessible for millions of Americans.

Over-Liquid Hospitals: Risks, Consequences, and Financial Stability Concerns

You may want to see also

Explore related products

![]()

Emergency Care: Legal requirements for hospitals to provide free emergency treatment regardless of payment ability

Hospitals in the United States are legally obligated to provide emergency medical care to anyone, regardless of their ability to pay, under the Emergency Medical Treatment and Labor Act (EMTALA). Enacted in 1986, this federal law mandates that Medicare-participating hospitals with emergency departments must offer a medical screening exam to anyone seeking treatment for an emergency medical condition. If such a condition exists, the hospital must stabilize the patient before considering transfer or discharge. This requirement ensures that individuals in dire need of care are not turned away due to financial constraints, addressing a critical gap in access to healthcare.

The scope of EMTALA is both broad and specific. It defines an "emergency medical condition" as a situation where the absence of immediate medical attention could result in serious jeopardy to the patient’s health, including severe pain. For instance, a hospital must treat a patient experiencing a heart attack, severe injury, or active labor, even if they lack insurance or cannot pay. However, the law does not require hospitals to provide non-emergency services for free. Once stabilized, patients may be billed for the services rendered, but the hospital cannot withhold treatment during the emergency phase due to payment concerns.

Despite EMTALA’s clear mandate, challenges persist in its implementation. Hospitals often struggle with uncompensated care costs, which can strain resources and affect overall financial stability. Patients, on the other hand, may face unexpected bills after treatment, as the law does not eliminate charges—it only ensures access to care. For example, a patient treated for a broken leg in the emergency room will still receive a bill afterward, but the hospital cannot refuse treatment upfront. This distinction highlights the law’s focus on immediate care rather than long-term financial relief.

To navigate this landscape, patients should be aware of their rights under EMTALA. If denied emergency care due to payment concerns, individuals can file a complaint with the Centers for Medicare & Medicaid Services (CMS), which enforces the law. Hospitals found in violation may face penalties, including fines or loss of Medicare funding. Practically, patients should also explore financial assistance programs offered by hospitals, which often provide discounts or payment plans for low-income individuals. Understanding these options can mitigate the financial burden while ensuring compliance with legal protections.

In summary, EMTALA serves as a critical safeguard, ensuring that emergency care is accessible to all, regardless of financial status. While it does not make emergency treatment free in the long term, it guarantees immediate care during life-threatening situations. Both hospitals and patients must understand their roles and responsibilities under this law to ensure its effective implementation and protect the right to emergency medical care.

Data Collection Methods in Hospitals Explained

You may want to see also

Explore related products

$788.98

![]()

Charity Care: Hospitals offering free or discounted services to low-income, uninsured patients

Hospitals in the United States are not universally free, but a little-known provision called Charity Care bridges the gap for low-income, uninsured patients. This program, mandated by federal law for non-profit hospitals, offers free or discounted medical services based on income and assets. Eligibility varies by hospital, but generally, individuals earning below 200% of the federal poverty level qualify. For a family of four, this translates to an annual income of approximately $55,500 or less in 2023.

Optimizing Gabapentin Prescribing for Pain Management in Hospital Settings

You may want to see also

Explore related products

![]()

Hidden Costs: Potential fees for medications, tests, or follow-up care not covered by free programs

While many countries offer free or subsidized healthcare, the reality is that "free" often comes with asterisks. Even in systems boasting universal coverage, hidden costs can lurk in the shadows, catching patients off guard. Medications, diagnostic tests, and follow-up care, though essential for effective treatment, frequently fall outside the scope of free programs, leaving individuals facing unexpected financial burdens.

A common scenario involves a patient diagnosed with a chronic condition like diabetes. While the initial consultation and basic bloodwork might be covered, the ongoing costs of insulin, blood glucose monitors, and regular specialist visits can quickly add up. A single vial of insulin can cost upwards of $300 in the US, and without adequate insurance, this expense becomes a monthly struggle. Similarly, a patient requiring an MRI scan for a suspected tumor might find that the procedure itself is covered, but the contrast dye used to enhance the images carries a separate, often substantial, fee.

These hidden costs disproportionately affect vulnerable populations. Elderly individuals on fixed incomes, low-wage earners, and those with pre-existing conditions are particularly susceptible. For example, a 70-year-old with heart disease might require regular echocardiograms, each costing several hundred dollars, to monitor their condition. Without supplementary insurance, these tests become a financial strain, potentially leading to delayed or skipped appointments, jeopardizing their health.

The impact extends beyond individual finances. Unpaid medical bills can lead to debt, affecting credit scores and overall financial stability. Furthermore, the fear of hidden costs can deter individuals from seeking necessary care, leading to worsening health outcomes and potentially more costly interventions down the line.

To navigate this complex landscape, patients must become proactive advocates for their health. Scrutinizing insurance policies, understanding coverage limitations, and inquiring about potential out-of-pocket expenses for medications and procedures are crucial steps. Exploring generic medication options, seeking financial assistance programs, and negotiating payment plans with healthcare providers can also help mitigate the burden of hidden costs. Ultimately, while the concept of "free" healthcare is appealing, it's essential to recognize the potential pitfalls and take steps to protect oneself from the financial surprises that often lurk beneath the surface.

The Evolution of Hospice to Hospital: A Historical Perspective

You may want to see also

Frequently asked questions

County hospitals are not entirely free; they typically offer services on a sliding scale fee basis, depending on the patient's income and insurance status. Uninsured or low-income individuals may qualify for reduced or waived fees, but costs can still apply.

County hospitals are required by law (EMTALA) to provide emergency care regardless of a patient's ability to pay, but this does not mean the care is free. Patients may still receive a bill, though financial assistance or charity care programs may be available.

Yes, anyone can use county hospital services without insurance, but they will likely be billed for the services. Financial assistance programs are often available to help reduce or cover costs for uninsured or low-income patients.