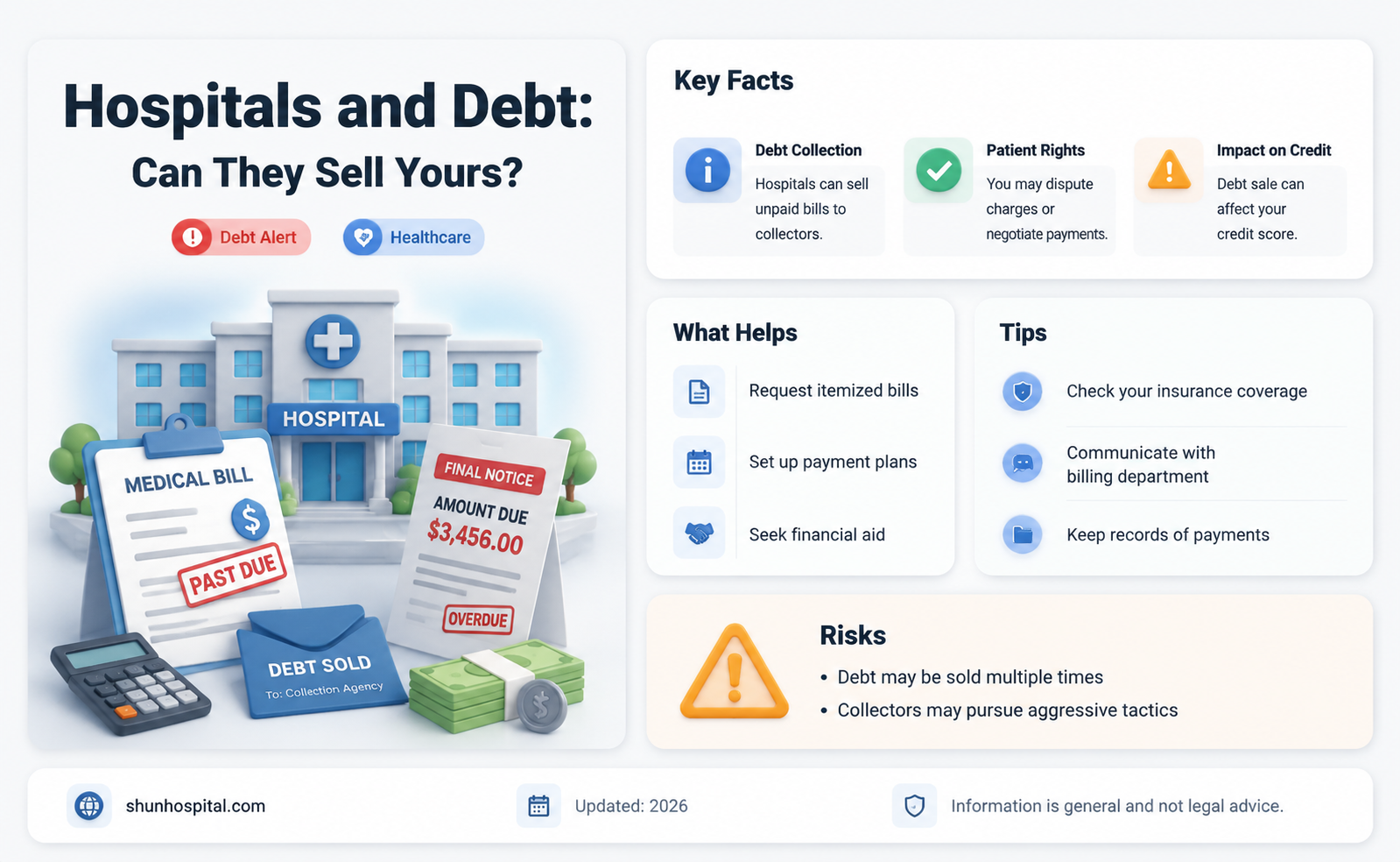

Medical debt is a unique type of debt that arises from a visit to a healthcare provider, such as a hospital, clinic, doctor, or nurse. Unlike other forms of debt, consumers rarely plan to take on medical debt. Medical debt is the most common collection type reported on consumer credit records, and consumers report being contacted by debt collectors about medical debt more than any other type of debt. Medical debt can be sold to third-party debt buyers, who then sue consumers for the full amount owed. This can result in reduced access to credit, increased risk of bankruptcy, avoidance of medical care, and difficulty securing employment. While there are some protections in place for consumers with medical debt, such as the No Surprises Act, which protects consumers from unexpected medical bills, and free or reduced care for those who cannot afford to pay, hospitals are generally allowed to sell medical debt to debt buyers.

| Characteristics | Values |

|---|---|

| Definition | Medical debt is a debt that arises from a visit or interaction with a healthcare provider, such as a hospital, clinic, doctor, or nurse. |

| Extent of the Problem | According to a 2022 report, $88 billion of outstanding medical bills are currently in collections, affecting one in five Americans. |

| Impact on Individuals | Medical debt can impact an individual's ability to buy or rent a home, increase insurance and car prices, and make it harder to find a job. |

| Consumer Rights | Consumers have the right to verify, dispute, negotiate, and resolve any debt, including medical debt. They can also request a "good faith" estimate of expected charges before receiving treatment. |

| State and Federal Laws | State and federal laws protect consumers from abusive, deceptive, or unfair debt collection practices. Federal laws also limit wage garnishment, and most states require court orders for this and other practices like placing a lien on a patient's home. |

| Hospital Requirements | Hospitals are required to provide itemized bills with plain language descriptions of services before sending accounts to collections. Non-profit hospitals must have written financial assistance policies and offer assistance to eligible patients. |

| Third-Party Involvement | Third-party debt buyers may purchase medical debt from hospitals and then sue consumers for the full amount, obscuring the medical origin of the lawsuit. |

| State Court Involvement | State courts can play a role in collecting medical debts, but there is limited recognition of this, and consumers often struggle to dispute or resolve medical debt issues through the courts. |

Explore related products

What You'll Learn

- Hospitals must offer financial assistance and payment plans to eligible patients

- Debt collectors must verify the debt and provide information about the collector and bill

- Medical debt can impact your ability to buy or rent a home, or find a job

- Debt collectors can contact other people to get your contact information

- Nonprofit hospitals must have a written financial assistance policy

![]()

Hospitals must offer financial assistance and payment plans to eligible patients

Hospitals are allowed to sell your debt to a third-party debt buyer if you are ineligible for financial assistance or have not responded to their attempts to offer assistance for 180 days. Medical debt is unique because consumers rarely plan to take it on and often have little control over the healthcare provider they receive care from. This, combined with the confusing and difficult-to-navigate billing and collections practices, means that medical debt is the most common type of debt reported on consumer credit records.

To address this issue, federal policies have been implemented to help patients better understand the cost of their care. The No Surprises Act, for example, requires healthcare providers to offer uninsured or self-pay patients a "good faith" estimate of their expected charges. Additionally, the Affordable Care Act (ACA) requires hospitals to have a written Financial Assistance Policy (FAP) that includes eligibility criteria and whether the care is free or discounted. Hospitals must provide this policy for free to anyone who requests it, and it must be widely publicized. Nonprofit hospitals are required by law to offer financial assistance programs, and many other providers are willing to work out payment plans.

Some states have also implemented their own policies to protect patients from medical debt. For example, Colorado requires hospitals to provide a payment plan and limit monthly payments to 4% of a patient's monthly gross income. Other states like California, Connecticut, Illinois, and Maine have charity care laws that require hospitals to provide free or discounted care to patients who meet certain requirements, often based on income.

If you are concerned about your hospital's financial assistance policy or are unable to resolve a billing dispute, there are several options for help. Many states provide Consumer Assistance Programs for consumers experiencing problems with their health insurance. You can also contact the Centers for Medicare & Medicaid Services, which offers detailed information about your protections against surprise medical bills and provides a help desk for medical billing questions.

Skin-to-Skin Contact: A Priceless Moment or a Hospital Charge?

You may want to see also

Explore related products

![]()

Debt collectors must verify the debt and provide information about the collector and bill

Hospitals can sell your debt to a third-party debt buyer, but only if you are ineligible for financial assistance or have not responded to their attempts to offer assistance for 180 days. Medical debt is unique because consumers often have no choice but to take it on, and billing and collections practices can be confusing and difficult to navigate.

If you are contacted by a debt collector, you have rights and protections under federal law, including the Fair Debt Collection Practices Act (FDCPA). This Act makes it illegal for debt collectors to use abusive, unfair, or deceptive practices when collecting debts. Debt collectors are also not permitted to report a medical bill to credit reporting companies without first attempting to collect the debt from you.

If you believe a debt collector's practices violate your rights, you can take action to enforce your rights. You can report them or sue a collector in state or federal court.

Opiates in Psychiatric Hospitals: Treatment or Hindrance?

You may want to see also

Explore related products

![]()

Medical debt can impact your ability to buy or rent a home, or find a job

Hospitals are allowed to sell your debt to a third-party debt buyer, but only if you are ineligible for financial assistance or have not responded to the hospital's attempt to offer assistance for 180 days. Medical debt is unique because consumers often have less ability to shop around for medical services, and billing and collections practices can be confusing and difficult to navigate.

Medical debt can impact your ability to buy or rent a home, as debt is a big part of your credit score. A low credit score can make it harder to secure a mortgage loan. In addition, medical debt can affect your debt-to-income ratio, which is another critical factor in mortgage loan approval. However, some changes have been made to reduce the impact of medical debt on credit scores. As of July 2022, many forms of medical debt should be removed from credit reports, and medical debt of less than $500 in collections will no longer be reported as of 2023. Furthermore, FHA-backed mortgages have eliminated medical debt from consideration when evaluating a borrower's creditworthiness. These changes aim to help potential homebuyers, especially those from low-income and minority groups, who are disproportionately affected by medical debt.

Medical debt can also impact your ability to rent a home. Landlords often run credit checks on prospective tenants, and a low credit score due to medical debt may make it more challenging to find rental housing.

Additionally, medical debt can make it more difficult to find a job. A low credit score can hinder employment opportunities, especially in industries where credit history is considered during the hiring process. However, it's important to note that the impact of medical debt on credit scores is being reevaluated, and the lending industry has reduced its reliance on medical debt as a predictor of credit risk.

The impact of medical debt on an individual's ability to buy or rent a home, or find a job, is significant. It can lead to long-term financial distress, with many individuals cutting back on necessities, taking on additional jobs, or working longer hours to repay their medical debt.

Ocala to Shands Hospital: Quickest Route and Distance

You may want to see also

Explore related products

![]()

Debt collectors can contact other people to get your contact information

Medical debt is a debt that arises from a visit or interaction with a healthcare provider, such as a hospital, clinic, doctor, or nurse. Two-thirds of medical debts are the result of a one-time or short-term medical expense arising from an acute medical need.

If a debt collector is representing you, they must communicate with your attorney instead of you. They may contact you if your attorney fails to respond within a reasonable time frame or agrees that the collector can contact you. Debt collectors may ask your employer for your address or phone number. If your employer does not allow you to receive personal calls at work, you should inform the debt collector. If a debt collector is aware that you are not permitted to receive their calls at work, they are not allowed to call you there.

Once a collection company receives your letter, it can only contact you to confirm that it will stop contacting you or to inform you of its intention to take legal action, such as filing a lawsuit. If you are concerned that a debt collector's practices violate your rights, you can take action to enforce your rights. You have rights and protections under federal law, including how and when debt collectors can contact you.

Tennessee Hospitals: Proper Pharma Waste Disposal

You may want to see also

Explore related products

![]()

Nonprofit hospitals must have a written financial assistance policy

Hospitals are allowed to sell your debt to a third-party debt buyer, but only if you are ineligible for financial assistance or have not responded to the hospital's attempt to offer assistance for 180 days. Medical debt is unique because consumers rarely plan to take it on and often have little choice over their healthcare providers. This makes medical billing and collections practices confusing and difficult to navigate.

Nonprofit hospitals are required by law to offer financial assistance programs. They must have a written financial assistance policy (FAP) that is widely publicized and includes eligibility criteria for financial assistance, the basis for calculating patient charges, and whether such assistance includes free or discounted care. The FAP must also include information on how to apply, as well as the website address and physical location where individuals can obtain copies of the FAP and FAP application form.

The IRS requires hospitals to make reasonable efforts to inform patients of their financial assistance policy. However, a 2019 analysis by Kaiser Health News found that hospitals often attempt to collect debt from people who would have qualified for financial assistance under the hospitals' policies if they had filled out the applications. Federal law and some state laws require hospitals to have written policies outlining eligibility criteria and application requirements to receive financial assistance. Under the Affordable Care Act, nonprofit hospitals must widely publicize these financial assistance policies, provide paper copies to patients during the intake or discharge process, display the policies in public spaces, and include website links and contact information on billing statements.

Some states provide incentives for hospitals to have well-funded financial assistance initiatives and effective distribution of funds, such as property, income, and sales tax exemptions. However, other states have no legislation governing the provision of financial assistance. There is a lack of systematic evidence on the impact of state-level financial assistance policies, and it is unclear whether they help or hinder eligible patients in obtaining financial assistance.

Robert Wood Johnson Hospital: How Far Is It?

You may want to see also

Frequently asked questions

Yes, hospitals are allowed to sell patient debt to third-party debt buyers. However, there are laws in place that protect consumers from unfair debt collection practices, such as the No Surprises Act, which protects consumers from unexpected medical bills. Additionally, nonprofit hospitals are required by law to offer financial assistance programs.

If you cannot pay your medical bills, you have the right to dispute, negotiate, and resolve the debt. You can also look into financial assistance programs offered by the hospital or seek help from a credit counselor.

Medical debt can impact your credit score and show up on your credit report. As of 2021, medical debt was the most common collection type reported on consumer credit records. Starting in 2023, major credit bureaus will stop adding medical debt that's less than $500 to credit reports.