Medigap plans, also known as Medicare Supplement plans, are designed to cover the gaps in Original Medicare coverage. These plans are offered by private insurance companies and can help pay for out-of-pocket costs such as deductibles, copays, and coinsurance. However, not all hospitals accept Medigap plans. Acceptance varies depending on the hospital's policies and the specific Medigap plan in question. It's essential for individuals to research and understand which hospitals in their area accept their Medigap plan to ensure they receive the expected coverage.

Explore related products

$18.76

What You'll Learn

- Medigap Plan Basics: Understand what a Medigap plan is and how it works with Medicare

- Hospital Network: Check if your preferred hospital is within the Medigap plan's network

- Coverage Details: Review what services and treatments are covered under the Medigap plan

- Cost Comparison: Compare the costs of different Medigap plans and their benefits

- Enrollment Periods: Learn about the enrollment periods for Medigap plans and how to apply

![]()

Medigap Plan Basics: Understand what a Medigap plan is and how it works with Medicare

A Medigap plan, also known as a Medicare Supplement plan, is a type of health insurance that helps cover the gaps in Original Medicare coverage. These plans are designed to pay for certain out-of-pocket costs that Medicare doesn't cover, such as deductibles, copayments, and coinsurance. Medigap plans are offered by private insurance companies and are standardized by the federal government, ensuring that all plans with the same letter designation provide the same coverage.

Medigap plans work in conjunction with Original Medicare, which includes Part A (hospital insurance) and Part B (medical insurance). To be eligible for a Medigap plan, you must have both Part A and Part B. When you have a Medigap plan, Medicare pays its share of your healthcare costs first, and then your Medigap plan pays its share of the remaining costs. This helps to reduce your out-of-pocket expenses.

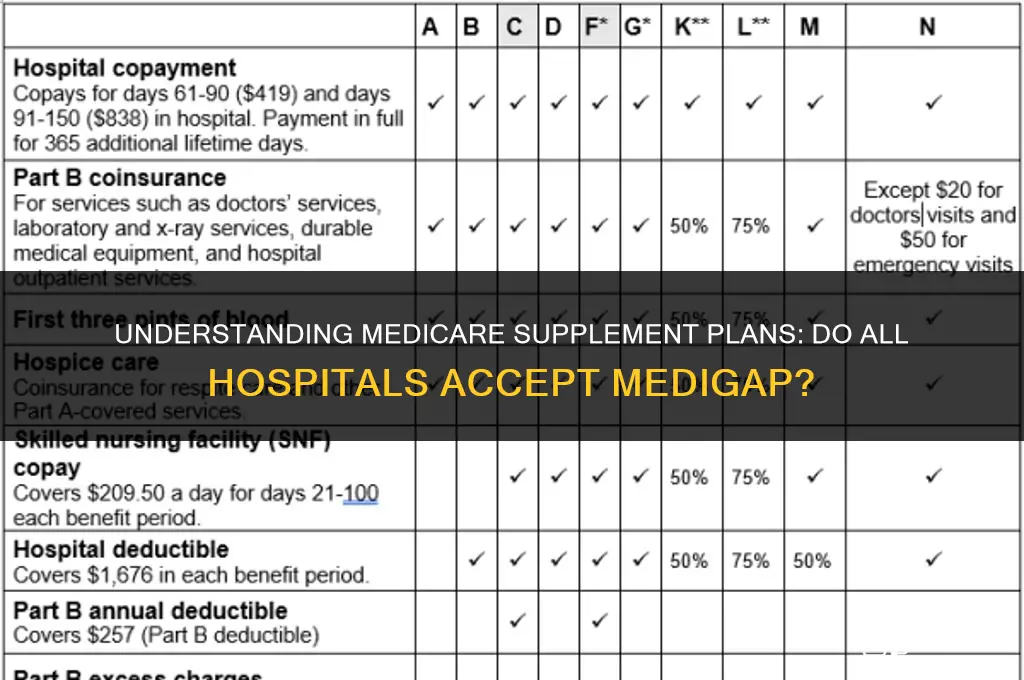

There are several different Medigap plans available, each with its own level of coverage. The most comprehensive plans, such as Plan F and Plan G, cover a wide range of out-of-pocket costs, including the Medicare Part A deductible and excess charges. Other plans, such as Plan A and Plan B, offer more limited coverage. It's important to choose a plan that meets your specific healthcare needs and budget.

One of the key benefits of Medigap plans is that they typically do not have provider networks. This means that you can see any healthcare provider who accepts Medicare, without worrying about whether they are in-network or out-of-network. However, it's still important to check with your provider to ensure that they accept Medicare and your specific Medigap plan.

When considering a Medigap plan, it's important to understand the enrollment process. The best time to enroll is during your Initial Enrollment Period (IEP), which is the six-month period that begins the month you turn 65 and have Part B. During this time, you are guaranteed issue, meaning that you cannot be denied coverage based on your health status. If you miss your IEP, you may have to go through medical underwriting to qualify for a plan.

In summary, Medigap plans are a valuable tool for reducing out-of-pocket healthcare costs for Medicare beneficiaries. By understanding how these plans work and the different options available, you can make an informed decision about whether a Medigap plan is right for you.

Do CMN Hospitals Provide Abortion Services? Facts and Insights

You may want to see also

Explore related products

![]()

Hospital Network: Check if your preferred hospital is within the Medigap plan's network

To ensure that your preferred hospital is within the Medigap plans network, it's essential to conduct thorough research. Start by obtaining a list of hospitals in your area that accept Medigap plans. This information can typically be found on the official Medigap website or by contacting your state's health insurance department. Once you have this list, cross-reference it with the hospitals you are considering for your healthcare needs.

Another crucial step is to verify the specific Medigap plans accepted by your preferred hospital. Not all hospitals accept all Medigap plans, so it's important to confirm which plans are in-network. This can be done by contacting the hospital's billing department or visiting their website. Additionally, consider reaching out to your Medigap plan provider to inquire about any recent changes to their network of participating hospitals.

It's also advisable to check the hospital's reputation and quality of care. While a hospital may accept Medigap plans, it's important to ensure that it meets your standards for healthcare. Look for reviews and ratings from reputable sources, such as the Centers for Medicare & Medicaid Services (CMS) or private healthcare review organizations.

In conclusion, verifying whether your preferred hospital is within the Medigap plans network involves several key steps: obtaining a list of participating hospitals, confirming the specific plans accepted, and evaluating the hospital's reputation and quality of care. By taking these steps, you can ensure that you receive the best possible healthcare while maximizing the benefits of your Medigap plan.

Facial Burns: When to Seek Hospitalization for Proper Treatment

You may want to see also

Explore related products

![]()

Coverage Details: Review what services and treatments are covered under the Medigap plan

Medigap plans, also known as Medicare Supplement plans, are designed to cover the gaps in Original Medicare coverage. These plans can help pay for out-of-pocket costs such as deductibles, copayments, and coinsurance. However, not all services and treatments are covered under Medigap plans. It's essential to review the coverage details of each plan to understand what is included and what is not.

When reviewing Medigap plan coverage, it's important to consider the specific services and treatments you may need. For example, some plans may cover prescription drugs, while others may not. Additionally, some plans may cover dental and vision care, while others may not. It's also important to note that Medigap plans do not cover long-term care or custodial care.

To review the coverage details of a Medigap plan, you can start by looking at the plan's Summary of Benefits. This document provides an overview of the plan's coverage, including the services and treatments that are covered and the out-of-pocket costs you may be responsible for. You can also contact the plan's customer service department to ask specific questions about coverage.

Another important aspect to consider when reviewing Medigap plan coverage is the plan's network. Some plans may have a network of preferred providers, while others may allow you to see any provider that accepts Medicare. It's important to understand the plan's network and how it may impact your ability to access the services and treatments you need.

Finally, it's important to compare the coverage details of different Medigap plans to find the one that best meets your needs. You can use online comparison tools or work with a licensed insurance agent to compare plans and make an informed decision. Remember, the coverage details of Medigap plans can vary significantly, so it's essential to do your research and choose the plan that provides the best coverage for your specific needs.

Unveiling the History: How Old is Memodies Hospital?

You may want to see also

Explore related products

![]()

Cost Comparison: Compare the costs of different Medigap plans and their benefits

Medigap plans, also known as Medicare Supplement plans, are designed to cover the gaps in Original Medicare coverage. These plans can vary significantly in terms of cost and benefits, making it essential to compare them carefully before making a decision.

One of the primary factors to consider when comparing Medigap plans is the premium cost. Premiums can range widely depending on the plan, the insurance company, and your location. For example, Plan G, which is one of the most popular Medigap plans, can have premiums that vary by hundreds of dollars per year between different insurers. It's crucial to shop around and get quotes from multiple companies to find the best rate for your specific situation.

In addition to premium costs, it's important to compare the out-of-pocket costs associated with each plan. These can include deductibles, copayments, and coinsurance. Some plans, like Plan F, cover all Medicare-approved expenses, while others, like Plan G, require you to pay the Medicare Part B deductible. Understanding these out-of-pocket costs can help you estimate your total healthcare expenses for the year and choose a plan that fits your budget.

Another key aspect to consider is the benefits provided by each plan. While all Medigap plans cover certain basic benefits, such as hospital coinsurance and medical expenses, some plans offer additional coverage. For instance, Plan D includes prescription drug coverage, which can be a significant advantage for those who take multiple medications. Other plans may offer extra benefits like dental, vision, or wellness programs. It's essential to review the benefits of each plan and determine which ones align with your healthcare needs.

When comparing Medigap plans, it's also important to consider the insurance company's reputation and customer service. Some companies may have lower premiums but higher customer complaints or lower satisfaction ratings. Researching the company's financial stability and customer reviews can help you make an informed decision and avoid potential headaches down the road.

In conclusion, comparing the costs and benefits of different Medigap plans requires careful consideration of premium costs, out-of-pocket expenses, benefits, and the insurance company's reputation. By taking the time to shop around and evaluate your options, you can find a Medigap plan that provides the right balance of coverage and affordability for your specific needs.

Parenteral Nutrition in Hospitals: Timing and Clinical Decision-Making Guide

You may want to see also

Explore related products

![]()

Enrollment Periods: Learn about the enrollment periods for Medigap plans and how to apply

Enrollment periods for Medigap plans are critical to understand for beneficiaries looking to supplement their Medicare coverage. Medigap, also known as Medicare Supplement Insurance, helps cover costs that Medicare doesn't, such as copayments, coinsurance, and deductibles. The enrollment periods are specific times when individuals can purchase a Medigap policy without facing medical underwriting, which means they won't be denied coverage or charged higher premiums based on their health status.

The Initial Enrollment Period (IEP) is the first opportunity to enroll in a Medigap plan. This period begins the month before an individual turns 65 and continues for seven months after their 65th birthday. During this time, beneficiaries can choose any Medigap plan available in their area without worrying about their health conditions. It's essential to enroll during this period to avoid potential delays in coverage and to secure the best rates.

Outside of the IEP, there are other enrollment periods, such as the Annual Enrollment Period (AEP), which runs from October 15 to December 7 each year. During the AEP, beneficiaries can switch Medigap plans or enroll in a new one. However, they may be subject to medical underwriting, which could affect their eligibility and premiums. Additionally, there are Special Enrollment Periods (SEPs) triggered by specific events, such as losing employer-sponsored health coverage or moving to a new area. These SEPs allow individuals to enroll in a Medigap plan without facing medical underwriting.

To apply for a Medigap plan, beneficiaries should research the available options in their area, compare the coverage and costs, and then contact the insurance company directly to enroll. It's advisable to work with a licensed insurance agent who specializes in Medicare products to ensure the best fit for individual needs and circumstances. Remember, understanding and acting on the enrollment periods is crucial for securing the right Medigap coverage at the right time.

Dr. Phil's Education: Did He Study at Menninger's Hospital in Topeka, KS?

You may want to see also

Frequently asked questions

Not all hospitals accept Medigap plans. While many do, it's important to check with the specific hospital or healthcare provider to confirm their acceptance of Medigap insurance.

Several factors can influence a hospital's decision to accept Medigap plans, including the hospital's size, location, the number of Medicare patients they serve, and their overall insurance acceptance policies.

You can find out if a specific hospital accepts Medigap plans by contacting the hospital's billing or admissions department directly. Additionally, you can check with your Medigap insurance provider for a list of participating hospitals.

If a hospital does not accept Medigap plans, patients may be responsible for paying the full cost of their healthcare services out-of-pocket. This can lead to significant financial burdens, especially for those with limited income or savings.