Hospitals' acceptance of Medicare Advantage plans is a critical consideration for beneficiaries seeking comprehensive healthcare coverage. Medicare Advantage, an alternative to Original Medicare, is offered by private insurance companies approved by Medicare, and it often includes additional benefits such as vision, dental, and prescription drug coverage. While most hospitals do accept Medicare Advantage plans, the extent of acceptance can vary depending on the specific plan, the hospital's network agreements, and geographic location. Beneficiaries should verify with both their chosen hospital and their Medicare Advantage provider to ensure seamless access to care and avoid unexpected out-of-pocket costs. Understanding these dynamics is essential for making informed decisions about healthcare coverage and treatment options.

Explore related products

What You'll Learn

- Eligibility Criteria: Understanding Medicare Advantage enrollment requirements for hospital acceptance

- Network Providers: Checking if hospitals are in-network for specific Medicare Advantage plans

- Coverage Limits: Exploring hospital services covered under Medicare Advantage policies

- Out-of-Pocket Costs: Analyzing copays, deductibles, and coinsurance for hospital visits

- Prior Authorization: Determining if hospitals require pre-approval for Medicare Advantage patients

![]()

Eligibility Criteria: Understanding Medicare Advantage enrollment requirements for hospital acceptance

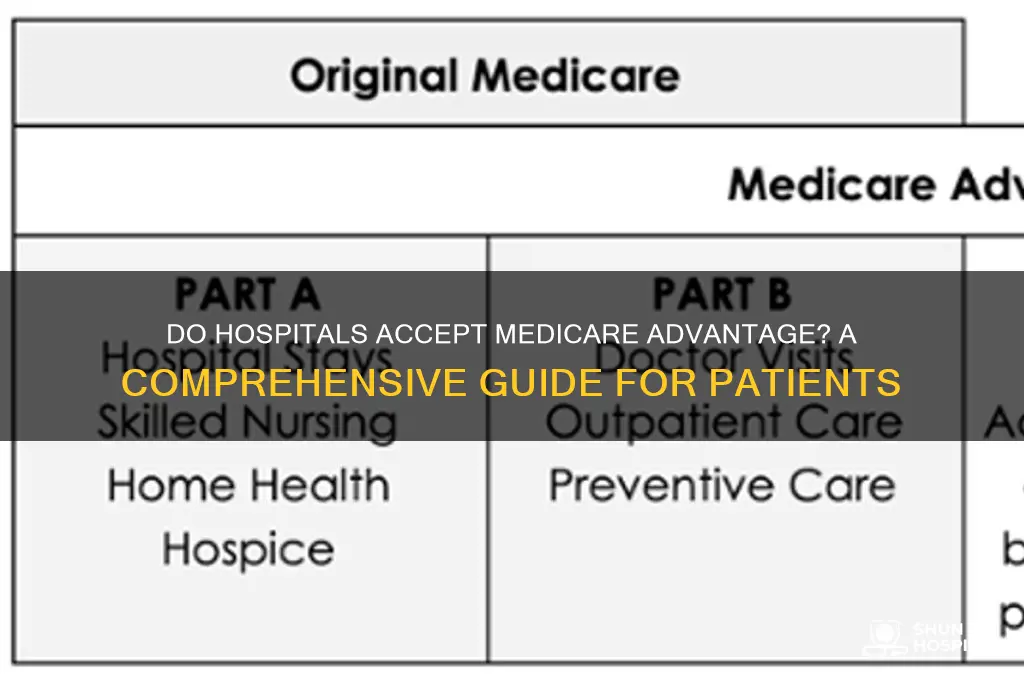

Medicare Advantage plans, also known as Medicare Part C, are an alternative to Original Medicare, offering additional benefits and often including prescription drug coverage. However, enrolling in a Medicare Advantage plan doesn't automatically guarantee acceptance at every hospital. Understanding the eligibility criteria is crucial for beneficiaries to ensure seamless access to healthcare services.

Enrollment Periods and Eligibility: To be eligible for a Medicare Advantage plan, individuals must first have Medicare Part A and Part B. The initial enrollment period is a 7-month window surrounding one's 65th birthday, but there are also special enrollment periods for specific circumstances, such as moving or losing employer coverage. During these periods, beneficiaries can join, switch, or drop a Medicare Advantage plan. It's essential to enroll during these designated times to avoid potential penalties and ensure coverage when needed.

Network Restrictions and Hospital Acceptance: One of the critical aspects of Medicare Advantage plans is their network structure. These plans often have network restrictions, meaning they contract with specific healthcare providers, including hospitals. Beneficiaries must use in-network hospitals and doctors to receive full coverage benefits. Out-of-network services may result in higher out-of-pocket costs or even denial of coverage. Therefore, when considering a Medicare Advantage plan, individuals should carefully review the plan's network to ensure their preferred hospitals are included.

Prior Authorization and Referral Requirements: Some Medicare Advantage plans may require prior authorization for certain services, including hospital admissions. This means that before a beneficiary can be admitted to a hospital, the plan must approve the service as medically necessary. Additionally, referrals from a primary care physician might be necessary for specialist consultations or hospital visits. Understanding these requirements is vital to avoid unexpected costs and ensure a smooth healthcare experience.

Geographic Considerations: Medicare Advantage plans are regionally specific, and their availability and coverage can vary by location. When traveling or relocating, beneficiaries should be aware that their plan's network and benefits may not extend to other areas. In such cases, understanding the plan's emergency coverage policies is essential, as well as knowing how to access urgent care services outside the network.

In summary, enrolling in a Medicare Advantage plan requires careful consideration of various eligibility criteria and plan specifics. Beneficiaries should review enrollment periods, network restrictions, authorization requirements, and geographic limitations to ensure their chosen plan aligns with their healthcare needs and preferred hospital choices. Being well-informed about these aspects can help individuals navigate the Medicare Advantage system effectively and make the most of their healthcare coverage.

Filing Hospital Indemnity Claims for Your Child: A Step-by-Step Guide

You may want to see also

Explore related products

$10.9 $19.99

$32.99 $34.99

![Vakly Extra Large Postpartum Maternity Pads [40 Pack] Hospital Style Super-Absorbent Contoured Pad Liners - 7" Wide X 14" Long - Heavier Overnight Post Birth Protection for Women - Incontinence Liners](https://m.media-amazon.com/images/I/71tRex25D8L._AC_UL320_.jpg)

![]()

Network Providers: Checking if hospitals are in-network for specific Medicare Advantage plans

Hospitals’ acceptance of Medicare Advantage plans hinges on their inclusion in the plan’s provider network, a detail often overlooked until care is urgently needed. Unlike Original Medicare, which allows beneficiaries to visit any hospital that accepts Medicare, Medicare Advantage plans typically operate within a restricted network of providers. This means a hospital’s participation in one Medicare Advantage plan does not guarantee acceptance in another, even if both plans are offered by the same insurer. Beneficiaries must verify network status for their specific plan to avoid unexpected out-of-pocket costs or denied coverage.

To check if a hospital is in-network, start by reviewing the plan’s provider directory, usually available on the insurer’s website or through their customer service line. For example, if you’re enrolled in a Humana Medicare Advantage plan, log into your account or call Humana directly to access their provider list. Cross-reference the hospital’s name and location to ensure it’s included. Be cautious of partial network participation—some hospitals may be in-network for certain services (e.g., emergency care) but out-of-network for others (e.g., elective surgeries). If the directory is unclear, contact the hospital’s billing department to confirm their relationship with your specific plan.

A practical tip for beneficiaries aged 65 and older or those with disabilities: use the Medicare Plan Finder tool on Medicare.gov. This resource allows you to enter your location and plan details to search for in-network hospitals. For instance, if you’re considering a UnitedHealthcare Medicare Advantage plan in Florida, the tool will display participating hospitals in your area. Pair this with a direct call to the hospital to verify their current network status, as directories may not always reflect real-time changes.

The consequences of using an out-of-network hospital can be financially significant. While emergency services are typically covered regardless of network status, non-emergency care at an out-of-network facility may result in higher copays, coinsurance, or even full out-of-pocket costs. For example, a routine knee replacement surgery at an in-network hospital might cost $500 in copays, whereas the same procedure at an out-of-network hospital could exceed $5,000. To avoid such scenarios, make network verification a priority during open enrollment or when selecting a Medicare Advantage plan.

Finally, consider the dynamic nature of provider networks. Hospitals and insurers renegotiate contracts annually, meaning a hospital in-network today may not be in-network next year. For instance, a 2022 study found that 12% of Medicare Advantage plans changed their hospital networks from the previous year. To stay informed, review your plan’s Annual Notice of Changes (ANOC) each fall and recheck hospital network status before scheduling non-emergency procedures. Proactive verification ensures continuity of care and minimizes financial surprises.

How to Get Your Birth Certificate: Hospital or Government?

You may want to see also

Explore related products

![]()

Coverage Limits: Exploring hospital services covered under Medicare Advantage policies

Medicare Advantage plans, also known as Medicare Part C, are required by law to cover everything that Original Medicare (Part A and Part B) covers, but they often include additional benefits and may impose different coverage limits. When it comes to hospital services, understanding these limits is crucial for beneficiaries to avoid unexpected out-of-pocket costs. For instance, while Original Medicare typically covers inpatient hospital stays under Part A with a deductible of $1,600 per benefit period (as of 2023), Medicare Advantage plans may have different cost-sharing structures, such as lower deductibles but higher copays for each hospital day. Beneficiaries should carefully review their plan’s Summary of Benefits to understand these variations.

One key area to explore is the coverage of specialized hospital services, such as intensive care unit (ICU) stays or emergency room visits. Medicare Advantage plans often have networks of providers, and out-of-network hospital services may be covered at a lower rate or not at all. For example, an ICU stay in an out-of-network hospital might require a 50% coinsurance payment, compared to 20% in-network. Additionally, some plans may limit the number of days covered for certain services, such as skilled nursing facility care after a hospital stay, which is typically capped at 100 days under Original Medicare but may vary under Medicare Advantage.

Another critical aspect is preauthorization requirements, which are more common in Medicare Advantage plans than in Original Medicare. Hospitals may require preauthorization for non-emergency procedures like joint replacements or cardiac surgeries. Failure to obtain preauthorization could result in denied coverage or higher costs. For example, a beneficiary scheduled for a knee replacement might need to ensure their surgeon and hospital are in-network and that the procedure is preauthorized to avoid a $5,000 out-of-pocket expense. This underscores the importance of proactive communication between beneficiaries, their healthcare providers, and their insurance plan.

Comparatively, while Original Medicare covers hospital services uniformly across the country, Medicare Advantage plans can vary significantly by region and provider. For instance, a plan in rural Texas might offer more comprehensive coverage for local hospitals but limited options for out-of-state care, whereas a plan in urban California might prioritize access to specialized hospitals but with higher out-of-pocket costs. Beneficiaries should consider their healthcare needs and geographic location when selecting a plan to ensure adequate hospital coverage.

Finally, practical tips for navigating coverage limits include regularly reviewing the Annual Notice of Changes (ANOC) sent by the plan each fall, as coverage limits and costs can change annually. Beneficiaries should also keep detailed records of hospital visits, preauthorizations, and payments to dispute any billing discrepancies. For those with chronic conditions requiring frequent hospital services, choosing a plan with lower out-of-pocket maximums and robust in-network hospital options can provide financial stability. By understanding and proactively managing these coverage limits, Medicare Advantage beneficiaries can maximize their hospital benefits while minimizing unexpected costs.

Hospitals and Debt: How Does It Affect Your Credit?

You may want to see also

Explore related products

$42.95

$19.99 $26.99

![]()

Out-of-Pocket Costs: Analyzing copays, deductibles, and coinsurance for hospital visits

Hospitals across the United States overwhelmingly accept Medicare Advantage plans, but understanding the out-of-pocket costs associated with hospital visits under these plans requires a closer look at copays, deductibles, and coinsurance. Unlike Original Medicare, which has standardized costs, Medicare Advantage plans vary widely by provider and region. For instance, a hospital stay might incur a $250 copay per day under one plan, while another may require a $1,000 deductible before coverage kicks in. These differences highlight the importance of scrutinizing plan details before enrollment.

To minimize unexpected expenses, beneficiaries should first identify whether their Medicare Advantage plan uses a Health Maintenance Organization (HMO) or Preferred Provider Organization (PPO) structure. HMO plans typically require in-network hospital visits to avoid higher out-of-pocket costs, while PPO plans offer more flexibility but often charge higher coinsurance rates for out-of-network care. For example, an in-network hospital stay might result in a 20% coinsurance rate after the deductible, whereas an out-of-network visit could double that rate. Always verify a hospital’s network status with your plan provider to avoid costly surprises.

Deductibles play a pivotal role in out-of-pocket costs for hospital visits. Some Medicare Advantage plans bundle medical and hospital deductibles, while others separate them. A plan with a $500 medical deductible and a $1,500 hospital deductible could leave beneficiaries paying the full hospital cost until the higher threshold is met. Conversely, plans with no deductible for hospital stays are available but often come with higher monthly premiums. Analyzing your healthcare usage patterns—such as frequency of hospital visits—can help determine which deductible structure aligns best with your financial situation.

Coinsurance and copays further complicate the cost landscape. For example, a plan might charge a $300 copay for the first three days of a hospital stay and 20% coinsurance thereafter. If a five-day stay costs $10,000, the beneficiary would pay $300 for the first three days and $1,400 (20% of $7,000) for the remaining two days, totaling $1,700. Understanding these tiered cost structures is crucial, especially for individuals with chronic conditions or those at higher risk of hospitalization. Tools like plan comparison charts or consultations with insurance brokers can simplify this analysis.

Finally, out-of-pocket maximums provide a safety net for Medicare Advantage beneficiaries. Once this limit is reached—typically ranging from $4,000 to $7,550 annually—the plan covers all additional costs. However, not all services count toward this maximum, so beneficiaries should confirm which expenses qualify. For instance, prescription drugs or certain specialist visits might not contribute to the out-of-pocket limit. By carefully reviewing these caps and exclusions, individuals can better predict their financial liability and choose a plan that offers both comprehensive coverage and manageable costs.

Enhancing Hospital Care: Strategies for Quality Improvement

You may want to see also

Explore related products

$24.99 $29.99

![]()

Prior Authorization: Determining if hospitals require pre-approval for Medicare Advantage patients

Hospitals often require prior authorization for Medicare Advantage patients to ensure services align with plan coverage and medical necessity. This process, while designed to manage costs and quality, can delay care if not navigated efficiently. Understanding the nuances of prior authorization is crucial for both providers and patients to avoid unexpected denials or out-of-pocket expenses.

For instance, a Medicare Advantage patient needing an MRI might face a prior authorization requirement. The hospital must submit documentation proving the procedure’s medical necessity, often including diagnostic codes (e.g., ICD-10 codes for chronic back pain) and treatment history. Failure to provide this information can result in claim denial, leaving the patient responsible for costs. Providers should verify the specific requirements of the patient’s Medicare Advantage plan, as these can vary widely between insurers like UnitedHealthcare, Humana, or Aetna.

To streamline prior authorization, hospitals should implement a structured process. First, identify if the service requires pre-approval by checking the plan’s coverage guidelines. Second, gather all necessary documentation, including physician notes, lab results, and imaging reports. Third, submit the request electronically, if possible, to expedite processing. Patients can assist by ensuring their provider has up-to-date insurance information and by inquiring about the status of their authorization request.

A comparative analysis reveals that traditional Medicare rarely requires prior authorization for hospital services, whereas Medicare Advantage plans frequently do. This disparity highlights the administrative burden placed on hospitals and patients under managed care models. For example, a study found that 90% of Medicare Advantage plans require prior authorization for outpatient surgeries, compared to 10% under traditional Medicare. This underscores the importance of verifying requirements early in the care planning process.

In conclusion, prior authorization is a critical step in ensuring Medicare Advantage patients receive covered hospital services without financial surprises. By understanding plan-specific requirements, maintaining thorough documentation, and leveraging electronic submission tools, hospitals can minimize delays and denials. Patients should proactively engage with their providers to confirm authorization status, ensuring a smoother healthcare experience.

Unveiling the 1999 Incident at Shady Grove Adventist Hospital SGHA

You may want to see also

Frequently asked questions

No, not all hospitals accept Medicare Advantage plans. Acceptance depends on whether the hospital is in-network with the specific Medicare Advantage plan. Always check with both the hospital and your plan provider to confirm coverage.

You can verify if a hospital accepts your Medicare Advantage plan by contacting your plan’s customer service, checking the plan’s provider directory, or directly calling the hospital’s billing department.

If you visit a hospital that is out-of-network with your Medicare Advantage plan, you may be responsible for higher out-of-pocket costs or the full cost of services, unless it’s an emergency situation.

Yes, Medicare Advantage plans are required by law to cover emergency services at any hospital, even if it’s out-of-network. However, follow-up care may need to be provided by in-network providers to avoid additional costs.