Hospitals often engage in a practice known as cost shifting, which occurs when they transfer the financial burden of uncompensated care or underfunded services to paying patients, typically those with private insurance. This phenomenon arises because hospitals must cover their operational costs, including treating uninsured or underinsured patients, as well as those on Medicaid, which often reimburses at rates below the cost of care. As a result, hospitals may increase charges for privately insured patients to offset these losses, leading to higher healthcare costs for individuals and employers. This practice has sparked significant debate about its fairness and its impact on the overall affordability and accessibility of healthcare. Understanding cost shifting is crucial for policymakers, healthcare providers, and consumers alike, as it highlights the complex financial pressures within the healthcare system and the need for sustainable solutions to ensure equitable care.

| Characteristics | Values |

|---|---|

| Definition | Cost shifting occurs when hospitals offset financial losses from underpaid services (e.g., Medicare/Medicaid) by increasing charges for privately insured patients. |

| Primary Drivers | Low reimbursement rates from public payers (Medicare/Medicaid), rising operational costs, and uncompensated care. |

| Impact on Private Payers | Higher charges for privately insured patients to compensate for losses, leading to increased premiums and out-of-pocket costs. |

| Evidence | Studies show hospitals charge private insurers 2-3 times more than Medicare rates (RAND Corporation, 2023). |

| Controversy | Critics argue it inflates healthcare costs, while hospitals claim it’s necessary for financial survival. |

| Regulatory Response | Some states have implemented price transparency laws and rate-setting policies to curb cost shifting. |

| Recent Trends | Increased scrutiny from policymakers and insurers, with efforts to standardize reimbursement rates. |

| Patient Impact | Higher costs for privately insured individuals, potentially reducing access to care. |

| Hospital Perspective | Viewed as a survival strategy in the face of underfunded public programs and rising expenses. |

| Data Source | Latest data from RAND Corporation (2023), American Hospital Association (AHA), and Healthcare Financial Management Association (HFMA). |

Explore related products

What You'll Learn

- Medicare/Medicaid Reimbursement Rates: Low government payments force hospitals to shift costs to private insurers

- Uncompensated Care Costs: Hospitals offset losses from uninsured/underinsured patients by charging more to others

- Private Insurance Negotiations: Hospitals charge private insurers higher rates to compensate for lower public payments

- Fixed vs. Variable Costs: Hospitals spread fixed costs across payers, increasing charges for privately insured

- Market Power Dynamics: Hospitals with monopoly power raise prices on private insurers to cover shortfalls

![]()

Medicare/Medicaid Reimbursement Rates: Low government payments force hospitals to shift costs to private insurers

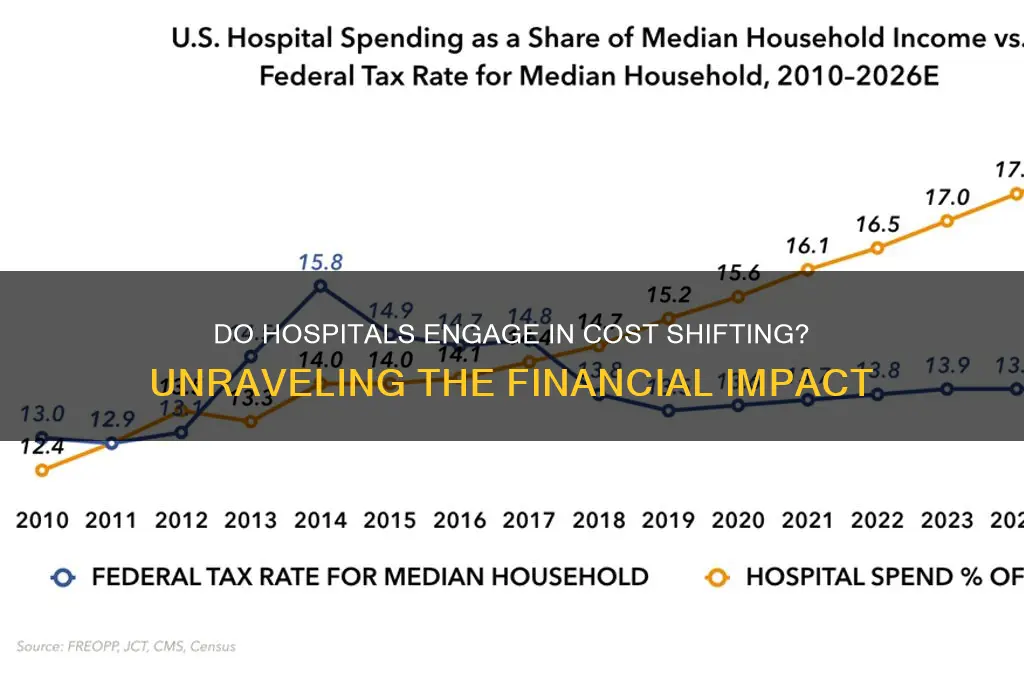

Hospitals across the United States face a financial conundrum when treating patients covered by Medicare and Medicaid. These government-funded programs, while essential for providing healthcare to millions of Americans, often reimburse hospitals at rates significantly below the actual cost of care. For instance, Medicare reimbursements typically cover only 85-90% of the cost of treating a patient, leaving hospitals to absorb the remaining 10-15%. This disparity forces hospitals to adopt a practice known as cost-shifting, where they offset these losses by charging private insurers higher rates. This financial balancing act ensures hospitals remain operational but raises ethical and economic questions about the sustainability of such a system.

Consider the practical implications of this cost-shifting mechanism. When a hospital treats a Medicare patient for a hip replacement, the procedure might cost $30,000, but Medicare reimburses only $25,000. To recover the $5,000 shortfall, the hospital may charge a private insurer $35,000 for the same procedure. This practice effectively subsidizes underfunded government programs with revenue from privately insured patients. While this approach keeps hospitals afloat, it disproportionately burdens individuals and employers who rely on private insurance, leading to higher premiums and out-of-pocket costs. This cycle perpetuates the rising cost of healthcare, impacting everyone in the system.

From a policy perspective, addressing this issue requires a multifaceted approach. Increasing Medicare and Medicaid reimbursement rates to match the actual cost of care would alleviate the need for cost-shifting. However, such a solution demands significant federal funding, which may be politically challenging to secure. Alternatively, implementing transparent pricing models and capping what hospitals can charge private insurers could mitigate the financial strain on privately insured patients. For example, setting a maximum markup of 10% above the Medicare reimbursement rate could balance hospital revenue needs with consumer protection. Policymakers must weigh these options carefully, considering both the financial health of hospitals and the affordability of healthcare for all Americans.

The impact of cost-shifting extends beyond hospitals and insurers to affect patient care directly. When hospitals rely on private insurers to subsidize losses, they may prioritize services that generate higher reimbursements, potentially neglecting areas like primary care or mental health. This misalignment of incentives can lead to inefficiencies and inequities in healthcare delivery. For instance, a hospital might invest in a state-of-the-art cardiac unit while underfunding its maternity ward, reflecting the financial realities of reimbursement rates rather than community health needs. Addressing this issue requires not only financial reforms but also a reevaluation of how healthcare resources are allocated to ensure equitable access to essential services.

In conclusion, the practice of cost-shifting driven by low Medicare and Medicaid reimbursement rates highlights the complexities of the U.S. healthcare system. While it serves as a temporary solution for hospitals, it exacerbates broader issues of affordability and equity. Stakeholders—from policymakers to healthcare providers—must collaborate to develop sustainable solutions that balance financial viability with the imperative to provide accessible, high-quality care. Without such reforms, the burden of cost-shifting will continue to weigh heavily on privately insured individuals, undermining the very purpose of a healthcare system designed to serve all.

Evaluating Hospital Size: Key Metrics Beyond Bed Count and Facilities

You may want to see also

Explore related products

![]()

Uncompensated Care Costs: Hospitals offset losses from uninsured/underinsured patients by charging more to others

Hospitals in the United States face a financial conundrum when treating uninsured or underinsured patients. These individuals often cannot pay their medical bills, leaving hospitals with uncompensated care costs. In 2020, US hospitals provided approximately $42 billion in uncompensated care, according to the American Hospital Association. This staggering figure highlights the challenge hospitals face in maintaining financial stability while serving their communities. To offset these losses, hospitals employ a practice known as cost-shifting, where they charge higher prices to patients with private insurance or Medicare.

Consider the case of a rural hospital that treats a significant number of uninsured patients due to the area's high poverty rate. The hospital might provide $5 million in uncompensated care annually. To recoup these losses, the hospital negotiates higher reimbursement rates with private insurers. For instance, the hospital may charge $1,500 for a routine MRI to a privately insured patient, while the actual cost is around $800. This price difference helps subsidize the care provided to uninsured patients. However, this practice has broader implications, as it contributes to the overall rise in healthcare costs for insured individuals and employers.

From a policy perspective, cost-shifting is a double-edged sword. On one hand, it allows hospitals to continue operating and providing essential services to vulnerable populations. On the other hand, it exacerbates affordability issues for those with insurance. For example, a family with employer-sponsored health insurance might face higher premiums or out-of-pocket costs due to their insurer paying elevated hospital charges. This dynamic underscores the interconnectedness of the healthcare system and the need for comprehensive solutions. Policymakers must address the root causes of uncompensated care, such as expanding Medicaid coverage or implementing subsidies for low-income individuals.

To mitigate the impact of cost-shifting, individuals can take proactive steps to manage their healthcare expenses. First, understand your insurance plan’s coverage and negotiate medical bills when possible. Many hospitals offer financial assistance programs for uninsured or underinsured patients, so inquire about eligibility. Additionally, consider using transparent pricing tools or healthcare advocates to compare costs across providers. For instance, a patient needing a knee replacement could save thousands of dollars by choosing an ambulatory surgery center over a hospital. These actions not only reduce personal financial burden but also exert pressure on the system to become more transparent and fair.

Ultimately, uncompensated care costs and the resulting cost-shifting reflect deeper systemic issues in the US healthcare system. While hospitals must balance their budgets, relying on inflated charges to insured patients is unsustainable. Addressing this issue requires a multi-faceted approach, including policy reforms, increased funding for safety-net programs, and greater price transparency. Until then, both providers and patients must navigate this complex landscape, seeking equitable solutions that ensure access to care without compromising financial stability.

Are Hospital Security Officers Armed? Exploring Safety Measures in Healthcare Facilities

You may want to see also

Explore related products

$12.59 $15.9

![]()

Private Insurance Negotiations: Hospitals charge private insurers higher rates to compensate for lower public payments

Hospitals often engage in a practice known as cost-shifting, where they charge private insurers higher rates to offset financial losses incurred from treating patients covered by public programs like Medicare and Medicaid. This strategy is a direct response to the reimbursement gap between private and public payers. For instance, Medicare reimburses hospitals at approximately 88 cents for every dollar spent on patient care, while Medicaid rates can be even lower, sometimes covering only 60-70% of costs. To maintain financial viability, hospitals negotiate aggressively with private insurers, demanding higher rates to subsidize the shortfall from public programs. This dynamic creates a complex pricing landscape where privately insured patients effectively subsidize care for those on public insurance.

Consider the negotiation process between hospitals and private insurers as a high-stakes game of leverage. Hospitals use their market power, often as dominant providers in a region, to secure favorable contracts. Private insurers, meanwhile, push back by threatening to exclude hospitals from their networks, which could reduce patient volume. The result is a delicate balance where hospitals charge private insurers 200-300% more than Medicare rates. For example, a routine MRI might cost Medicare $400, but a private insurer could be billed $1,200 for the same procedure. This disparity highlights how cost-shifting directly impacts private insurance premiums, as insurers pass these higher costs onto consumers through increased premiums and out-of-pocket expenses.

To illustrate the practical implications, imagine a family with private insurance facing a $5,000 deductible. A hospital stay for a minor procedure could result in a bill significantly higher than what Medicare would pay, due to the inflated rates charged to private insurers. This scenario underscores the financial burden cost-shifting places on privately insured individuals. Policymakers and advocates argue that this practice exacerbates healthcare inequality, as those with private insurance indirectly fund care for public program beneficiaries, often without realizing it. Understanding this mechanism is crucial for patients to advocate for transparency in pricing and for insurers to negotiate fairer contracts that mitigate the impact of cost-shifting.

Addressing cost-shifting requires a multi-faceted approach. Hospitals could improve efficiency by reducing administrative costs or adopting value-based care models, which tie reimbursement to patient outcomes rather than volume of services. Insurers, on the other hand, could collaborate with hospitals to establish reference pricing, setting a standard rate for common procedures across all payers. Patients can contribute by demanding price transparency and exploring bundled payment options for elective procedures. While these solutions are not without challenges, they offer a pathway toward a more equitable healthcare system where the financial burden is distributed more fairly, and cost-shifting becomes less of a necessity for hospitals.

Thoughtful Gifts to Welcome Loved Ones Home from the Hospital

You may want to see also

Explore related products

![]()

Fixed vs. Variable Costs: Hospitals spread fixed costs across payers, increasing charges for privately insured

Hospitals face a financial tightrope walk, balancing fixed costs like building maintenance and staff salaries against variable expenses tied to patient care. This dynamic often leads to a practice known as cost-shifting, where hospitals spread fixed costs across different payer groups, disproportionately burdening privately insured patients. Imagine a hospital with a $10 million annual mortgage. Regardless of patient volume, that payment remains constant. To cover it, the hospital might charge a privately insured patient $200 for a basic blood test, while Medicaid reimburses only $50 for the same service. This disparity isn’t arbitrary; it’s a survival strategy in a system where government and uninsured patients often pay less than the cost of care.

Consider the mechanics of this cost-shifting. Fixed costs, such as medical equipment leases or administrative salaries, don’t fluctuate with patient volume. Variable costs, like medications or disposable supplies, rise and fall with the number of patients treated. When government programs like Medicare and Medicaid reimburse hospitals at rates below the actual cost of care, hospitals must recoup the shortfall elsewhere. Privately insured patients, whose insurers often negotiate higher rates, become the target. For instance, a study by the Health Care Cost Institute found that private insurers paid hospitals 247% more than Medicare for the same services in 2020. This isn’t a value-added service; it’s a financial necessity for hospitals to keep their doors open.

The consequences of this system are far-reaching. Privately insured individuals and their employers bear the brunt of inflated costs, driving up premiums and out-of-pocket expenses. Meanwhile, hospitals argue that cost-shifting is essential to offset underpayments from government programs and uncompensated care for the uninsured. Critics counter that this practice lacks transparency and exacerbates healthcare inequality. For example, a privately insured patient undergoing a routine appendectomy might face a $15,000 bill, while a Medicaid patient’s reimbursement covers only $4,000 of the hospital’s costs. This disparity fuels debates about healthcare reform, with proposals ranging from site-neutral payments to global budgets aimed at curbing cost-shifting.

To navigate this landscape, patients and employers can take proactive steps. First, understand your insurance plan’s negotiated rates and compare them to Medicare benchmarks. Tools like Healthcare Bluebook or FAIR Health provide cost estimates for common procedures. Second, advocate for price transparency by asking hospitals for detailed cost breakdowns before procedures. Third, consider joining employer coalitions that negotiate directly with hospitals for fairer rates. Policymakers, meanwhile, must address the root causes of cost-shifting by reevaluating reimbursement models and ensuring hospitals are adequately funded without penalizing privately insured patients.

In conclusion, the fixed vs. variable cost dilemma in hospitals isn’t merely an accounting issue—it’s a systemic challenge with real-world implications. While cost-shifting allows hospitals to survive, it perpetuates a cycle of high costs and inequity. Addressing this requires a multifaceted approach: greater transparency, smarter reimbursement models, and collective action from patients, employers, and policymakers. Until then, privately insured patients will continue to shoulder a disproportionate share of healthcare costs, highlighting the urgent need for reform.

Queen Elizabeth II Hospitalized: What We Know So Far

You may want to see also

Explore related products

![]()

Market Power Dynamics: Hospitals with monopoly power raise prices on private insurers to cover shortfalls

Hospitals with significant market power often exploit their dominant position by engaging in cost-shifting, a practice where they charge private insurers higher rates to offset financial shortfalls from underfunded public programs like Medicare and Medicaid. This dynamic is particularly pronounced in regions where a single hospital or health system controls a large share of the market, leaving private insurers with little choice but to accept inflated prices. For instance, a 2018 study by the Health Care Cost Institute found that prices for common hospital procedures were 2.4 times higher for privately insured patients compared to Medicare beneficiaries. This disparity highlights how hospitals leverage their monopoly power to balance their budgets at the expense of private payers.

To understand the mechanics of this cost-shifting, consider the following scenario: a hospital faces a $10 million shortfall due to Medicare reimbursements that cover only 85% of the cost of care for its elderly patients. To recoup this loss, the hospital negotiates with private insurers to increase rates for services like MRI scans or surgical procedures. If the hospital has a 70% market share in its region, insurers are forced to agree to these higher rates to maintain access to the hospital’s services for their enrollees. This results in higher premiums for privately insured individuals and families, effectively shifting the financial burden from underfunded public programs to private payers.

The implications of this practice extend beyond immediate financial strain. Higher premiums discourage employers from offering comprehensive health insurance, leading to underinsurance or lack of coverage for some workers. Moreover, cost-shifting exacerbates healthcare disparities, as privately insured patients subsidize care for public program beneficiaries, often without realizing it. Policymakers and regulators must address this issue by promoting market competition, capping price increases, or adjusting public program reimbursement rates to reflect the true cost of care. Without intervention, hospitals will continue to exploit their market power, distorting the healthcare economy and burdening private payers.

A comparative analysis of states with and without hospital market consolidation reveals the extent of this problem. In California, where hospital mergers have reduced competition, private insurer costs are 30% higher than in Texas, where antitrust regulations have preserved a more competitive landscape. This comparison underscores the need for targeted policy solutions, such as antitrust enforcement and price transparency initiatives, to curb cost-shifting. For consumers, understanding this dynamic is crucial when selecting insurance plans or advocating for healthcare reform. By recognizing how hospitals use their monopoly power, stakeholders can push for systemic changes that ensure fair pricing and equitable access to care.

Exploring the City Home to University of Pennsylvania Hospital

You may want to see also

Frequently asked questions

Cost shifting refers to the practice where hospitals offset financial losses from treating Medicare, Medicaid, or uninsured patients by increasing charges for privately insured patients.

Hospitals engage in cost shifting because government and public insurance programs often reimburse at rates below the cost of care, forcing them to recover losses from patients with private insurance.

Yes, cost shifting can lead to higher out-of-pocket costs and insurance premiums for privately insured patients, as hospitals charge them more to compensate for underpayments from other payers.

Yes, cost shifting is legal and widely practiced in the U.S. healthcare system, though it remains a controversial topic due to its impact on healthcare affordability.