Medicare Part F, often confused with other Medicare plans, does not exist as a standalone coverage option; instead, it is a term sometimes mistakenly used to refer to Medicare Supplement plans, which are labeled differently (e.g., Plan G or Plan F). When considering hospital stays, Medicare Part A typically covers inpatient hospital care, including the first day of a hospital stay, provided the admission meets Medicare’s criteria for medical necessity. However, beneficiaries may still face out-of-pocket costs such as deductibles, coinsurance, or copayments, which is where Medicare Supplement plans like Plan F or Plan G can step in to cover these gaps. Understanding the specifics of your Medicare coverage is crucial to avoid unexpected expenses and ensure comprehensive care during a hospital stay.

Explore related products

What You'll Learn

- Medicare Part F Overview: Understanding Part F basics and its coverage scope

- Hospital Stay Coverage: Does Part F include first-day hospital stay expenses

- Part F vs. Other Parts: Comparing Part F coverage to Medicare Part A and B

- Eligibility Criteria: Who qualifies for Part F and its hospital stay benefits

- Out-of-Pocket Costs: Potential costs for first-day hospital stay under Part F

![]()

Medicare Part F Overview: Understanding Part F basics and its coverage scope

Medicare Part F is a type of Medicare Supplement Insurance (Medigap) plan designed to help cover some of the out-of-pocket costs that Original Medicare (Part A and Part B) doesn’t fully pay for. While Medicare Part A typically covers hospital stays, it often leaves beneficiaries with significant expenses, such as deductibles, coinsurance, and copayments. This is where Medicare Part F comes in, offering comprehensive coverage to fill these gaps. However, it’s important to note that as of 2020, Medicare Part F is no longer available to new Medicare enrollees, though those who enrolled before this date can keep their plan. Understanding the basics of Part F and its coverage scope is crucial for current beneficiaries to maximize their benefits.

One common question among Medicare beneficiaries is whether Medicare Part F covers the first day of a hospital stay. Original Medicare Part A typically covers hospital stays after the beneficiary meets the Part A deductible, which in 2023 is $1,600 per benefit period. Medicare Part F, being a Medigap plan, steps in to cover this deductible, ensuring that the first day of a hospital stay is fully covered without out-of-pocket costs for the beneficiary. This is a significant advantage, as hospital stays can quickly become expensive, and having the deductible covered can provide financial peace of mind.

In addition to covering the Part A deductible, Medicare Part F also covers other costs associated with hospital stays, such as coinsurance for days 61-90 and beyond, as well as hospice care coinsurance or copayments. It also covers the first three pints of blood, which Original Medicare does not fully cover. Furthermore, Part F provides coverage for skilled nursing facility care coinsurance, foreign travel emergency care, and Medicare Part B excess charges, which are fees charged by healthcare providers who do not accept Medicare’s approved amount as full payment.

It’s essential to understand that while Medicare Part F offers extensive coverage, it does not cover everything. For instance, it does not cover long-term care, vision or dental care, hearing aids, eyeglasses, or private-duty nursing. Additionally, Part F does not include prescription drug coverage, so beneficiaries would need to enroll in a separate Medicare Part D plan for medication coverage. Despite these limitations, Part F remains one of the most comprehensive Medigap plans available to those who enrolled before 2020.

For current Medicare Part F beneficiaries, knowing the scope of coverage is key to avoiding unexpected medical bills. By covering the Part A deductible and other hospital-related costs, Part F ensures that beneficiaries can focus on their health without the added stress of financial burdens. However, beneficiaries should regularly review their plan to ensure it continues to meet their healthcare needs, especially as their health status or medical requirements change over time. Understanding the basics of Medicare Part F and its coverage scope empowers beneficiaries to make informed decisions about their healthcare and financial planning.

Homeopathy Hospitals: Why Did They Vanish in the 1900s?

You may want to see also

Explore related products

![]()

Hospital Stay Coverage: Does Part F include first-day hospital stay expenses?

When considering hospital stay coverage under Medicare, it's essential to understand the specifics of each part, particularly Part F. However, it's important to clarify that Medicare does not have a Part F. Medicare is divided into several parts: Part A (Hospital Insurance), Part B (Medical Insurance), Part C (Medicare Advantage), and Part D (Prescription Drug Coverage). The confusion might arise from Medicare Supplement plans, which are labeled with letters, including Plan F. These supplement plans are designed to cover gaps in Original Medicare (Part A and Part B), but they are not part of Medicare itself.

Medicare Part A primarily covers hospital stays, including the first day of hospitalization. It helps pay for inpatient care in hospitals, skilled nursing facility care, hospice care, and some home health care. For the first day of a hospital stay, Part A covers the costs after the deductible is met. In 2023, the Part A deductible is $1,600 per benefit period. This means that once you pay this deductible, Part A covers the remaining costs for up to 60 days of hospitalization. Understanding this coverage is crucial for beneficiaries to plan their healthcare expenses effectively.

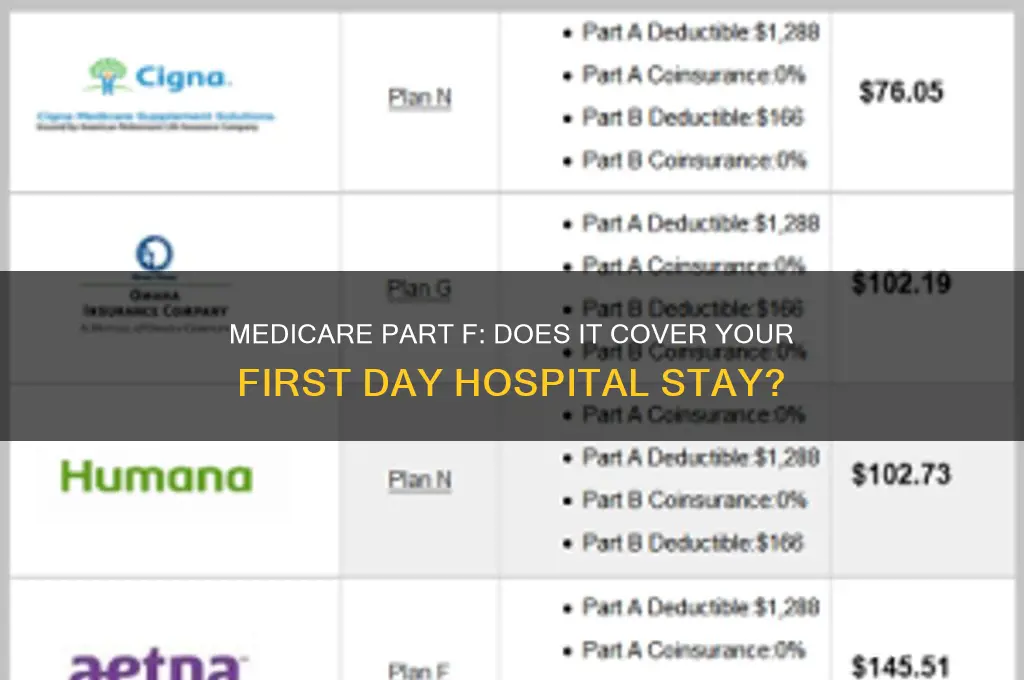

Medicare Supplement Plan F, often referred to as Medigap Plan F, is a private insurance plan that can help cover some of the out-of-pocket costs associated with Original Medicare, including Part A and Part B. Plan F is one of the most comprehensive Medigap plans available, covering the Part A deductible, Part B deductible, and other costs like copayments, coinsurance, and excess charges. This means that if you have Plan F, it can cover the $1,600 Part A deductible for your first day of hospitalization, effectively reducing your out-of-pocket expenses to zero for this aspect of your hospital stay.

However, it's important to note that as of January 1, 2020, Plan F is no longer available to new Medicare beneficiaries. If you became eligible for Medicare before this date, you may still be able to purchase Plan F. For those who became eligible after this date, Medicare Supplement Plan G is a popular alternative. Plan G is similar to Plan F but does not cover the Part B deductible. Despite this difference, Plan G still provides significant coverage for hospital stays, including the first day, by covering the Part A deductible and other associated costs.

In summary, while Medicare Part A covers the first day of a hospital stay after the deductible is met, Medicare Supplement Plan F (for those eligible) can cover this deductible, ensuring that beneficiaries have minimal out-of-pocket expenses. For those who cannot enroll in Plan F, Plan G offers a comparable level of coverage. Understanding these details is vital for Medicare beneficiaries to make informed decisions about their healthcare coverage and financial planning. Always consult with a Medicare specialist or review the official Medicare guidelines to ensure you have the most accurate and up-to-date information regarding your coverage options.

Tenet Healthcare: A Comprehensive Network of Hospitals and Facilities

You may want to see also

Explore related products

![]()

Part F vs. Other Parts: Comparing Part F coverage to Medicare Part A and B

Medicare Part F, often referred to as a Medicare Supplement plan, is designed to work alongside Original Medicare (Part A and Part B) to help cover out-of-pocket costs such as copayments, coinsurance, and deductibles. When comparing Part F to Medicare Part A and Part B, it’s essential to understand the distinct roles each part plays in covering healthcare services, particularly in the context of a hospital stay, including the first day. Medicare Part A primarily covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care. It typically covers the first day of a hospital stay after the beneficiary meets the Part A deductible. Part B, on the other hand, covers outpatient services, doctor visits, preventive care, and medically necessary services. Neither Part A nor Part B is designed to cover all costs, which is where Part F comes in.

Part F, as a Medigap plan, helps fill the gaps in Original Medicare coverage. For instance, it can cover the Part A deductible for hospital stays, including the first day, which is a significant benefit for beneficiaries. Unlike Part A, which requires beneficiaries to pay a deductible for each benefit period, Part F ensures that this cost is covered, reducing financial burden. Additionally, Part F may cover excess charges that occur when a healthcare provider charges more than the Medicare-approved amount, a scenario not addressed by Part A or Part B alone. This makes Part F a comprehensive option for those seeking more predictable and manageable healthcare expenses.

When comparing Part F to Part B, the differences become even more pronounced. Part B covers outpatient services but requires beneficiaries to pay a monthly premium, an annual deductible, and 20% coinsurance for most services. Part F can cover these out-of-pocket costs, including the Part B deductible and coinsurance, providing a more complete coverage solution. For example, if a beneficiary requires outpatient services during a hospital stay or after discharge, Part F ensures that the associated Part B costs are minimized or eliminated, whereas Part B alone would leave the beneficiary responsible for a portion of these expenses.

Another critical aspect of Part F is its coverage of emergency care during foreign travel, a benefit not offered by Part A or Part B. While Part A covers hospital stays within the U.S. and its territories, and Part B covers medically necessary services, neither extends to international travel. Part F covers 80% of emergency care costs during the first 60 days of a trip outside the U.S., up to specific limits. This added benefit highlights how Part F complements Original Medicare by addressing gaps in coverage that Part A and Part B do not.

In summary, Part F offers a layer of financial protection that Part A and Part B do not provide on their own. It covers the Part A deductible for hospital stays, including the first day, and addresses Part B coinsurance and deductibles, making it a valuable addition for beneficiaries seeking comprehensive coverage. While Part A and Part B form the foundation of Medicare, Part F ensures that beneficiaries are better shielded from unexpected out-of-pocket costs, particularly during hospital stays. Understanding these differences is crucial for making informed decisions about Medicare coverage.

Car Seat Safety: Do Hospitals Provide Newborn Seats?

You may want to see also

Explore related products

![]()

Eligibility Criteria: Who qualifies for Part F and its hospital stay benefits?

Medicare Part F, also known as Medicare Supplement Plan F, is a comprehensive supplemental insurance plan designed to cover costs that Original Medicare (Part A and Part B) does not fully cover. However, it’s important to note that Medicare Part F is no longer available to new enrollees as of January 1, 2020, due to changes in federal law. Only individuals who were eligible for Medicare before this date can still enroll in Plan F. For those who qualify, understanding the eligibility criteria and hospital stay benefits is crucial.

To be eligible for Medicare Part F, individuals must first be enrolled in both Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). Part A covers hospital stays, while Part B covers outpatient services. Once enrolled in these plans, beneficiaries can purchase Part F from private insurance companies. Eligibility is not based on income or medical history, but rather on enrollment in Original Medicare. Beneficiaries must pay a monthly premium for Part F in addition to their Part B premium.

Regarding hospital stay benefits, Medicare Part F covers the Part A deductible for hospital stays, which includes the first day of hospitalization. Original Medicare Part A typically requires beneficiaries to pay a deductible for each benefit period, which can change annually. Part F eliminates this out-of-pocket cost, ensuring that the first day and subsequent days of a hospital stay are fully covered. This benefit is particularly valuable for individuals who anticipate frequent hospital visits or extended stays.

Additionally, Part F covers Part B excess charges, foreign travel emergency care, and skilled nursing facility coinsurance, among other benefits. However, the primary focus for hospital stays is the coverage of the Part A deductible. Beneficiaries must ensure they are enrolled in both Part A and Part B to qualify for these benefits. It’s also important to note that Part F does not cover long-term care, vision, dental, or prescription drugs, which may require additional coverage.

For individuals who were eligible for Medicare before 2020 and are considering Part F, it’s advisable to compare it with other Medicare Supplement plans, such as Plan G, which is now more commonly recommended. Plan G offers similar benefits but does not cover the Part B deductible, which is typically lower than the Part A deductible. Consulting with a licensed insurance agent can help determine the best plan based on individual healthcare needs and costs.

In summary, eligibility for Medicare Part F and its hospital stay benefits requires enrollment in both Medicare Part A and Part B, with the plan covering the Part A deductible for the first day and beyond. While Part F is no longer available to new enrollees, those who qualify can benefit from its comprehensive coverage, particularly for hospital stays. Understanding these eligibility criteria ensures beneficiaries can make informed decisions about their healthcare coverage.

Weekend Hospital Surveys: Does the State Inspect Acute Care Facilities?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Out-of-Pocket Costs: Potential costs for first-day hospital stay under Part F

Medicare Part F, also known as Medicare Supplement Plan F, is a comprehensive supplemental insurance plan designed to cover many of the out-of-pocket costs that Original Medicare (Part A and Part B) does not fully cover. However, it’s important to clarify that Medicare Part F does not directly cover the first-day hospital stay costs, as Original Medicare Part A typically includes coverage for hospital stays after the beneficiary meets the Part A deductible. Despite this, Part F plays a crucial role in minimizing out-of-pocket expenses associated with hospital stays, including those incurred on the first day.

One of the primary out-of-pocket costs for a first-day hospital stay under Original Medicare is the Part A deductible. As of the latest updates, this deductible can exceed $1,600 per benefit period. Medicare Part F covers this deductible in full, ensuring that beneficiaries do not have to pay this amount out of pocket. This is a significant benefit, as the Part A deductible applies each time a beneficiary is admitted to the hospital after a 60-day gap in inpatient care. Without Part F, this cost would be the responsibility of the beneficiary.

In addition to the Part A deductible, beneficiaries may face daily coinsurance charges if their hospital stay extends beyond 60 days. While this coinsurance typically does not apply to the first day, Part F covers these additional costs if they arise during a prolonged stay. Furthermore, Part F covers the Part B deductible and coinsurance, which could apply if a beneficiary receives outpatient services during their hospital stay, such as doctor visits or medical procedures billed under Part B.

Another potential out-of-pocket cost is related to skilled nursing facility (SNF) care, which might be required after a hospital stay. Original Medicare covers the first 20 days in a SNF, but days 21 through 100 require a daily coinsurance payment. Part F covers this coinsurance, reducing financial burden on beneficiaries. However, it’s important to note that Part F does not cover long-term care or custodial care, which are not typically associated with the first-day hospital stay but could become relevant in extended care scenarios.

Lastly, beneficiaries should be aware that Part F also covers emergency care during foreign travel, up to plan limits. While this is not directly related to the first-day hospital stay, it highlights the comprehensive nature of Part F in managing out-of-pocket costs across various healthcare scenarios. In summary, while Medicare Part F does not directly cover the first-day hospital stay, it significantly reduces associated out-of-pocket costs by covering the Part A deductible, coinsurance, and other related expenses, making it a valuable supplement to Original Medicare.

Finding Theme Hospital Save Game Files: A Quick Location Guide

You may want to see also

Frequently asked questions

Medicare Part F does not exist; it may be a confusion with Medicare Supplement Plans. However, Medicare Part A typically covers hospital stays, including the first day, after meeting the deductible.

No, Medicare Part F is not a valid plan. Medicare Part A covers hospital stays, including the first day, after the deductible is paid.

Medicare does not offer Part F. First-day hospital coverage is provided by Medicare Part A, subject to the deductible.

Medicare Part F is not a legitimate plan. Coverage for the first day of a hospital stay is available under Medicare Part A, after the deductible.

There is no Medicare Part F. The first day of a hospital stay is covered by Medicare Part A, once the deductible is met.