Understanding how hospital coverage interacts with Medicare Part A and Blue Cross Blue Shield (BCBS) is crucial for navigating the complexities of healthcare insurance. Medicare Part A primarily covers inpatient hospital stays, skilled nursing facility care, and some home health services, serving as a foundational layer of coverage for eligible individuals. When paired with BCBS, which often acts as a supplementary or primary insurer depending on the plan, patients can benefit from expanded coverage, including reduced out-of-pocket costs for services not fully covered by Medicare. BCBS plans may also offer additional benefits such as prescription drug coverage, preventive care, and access to a broader network of healthcare providers. However, the coordination between Medicare Part A and BCBS can vary, requiring careful review of policy details to ensure seamless coverage and avoid gaps in care. Effective management of these interactions ensures that patients maximize their benefits while minimizing financial burdens.

Explore related products

What You'll Learn

![]()

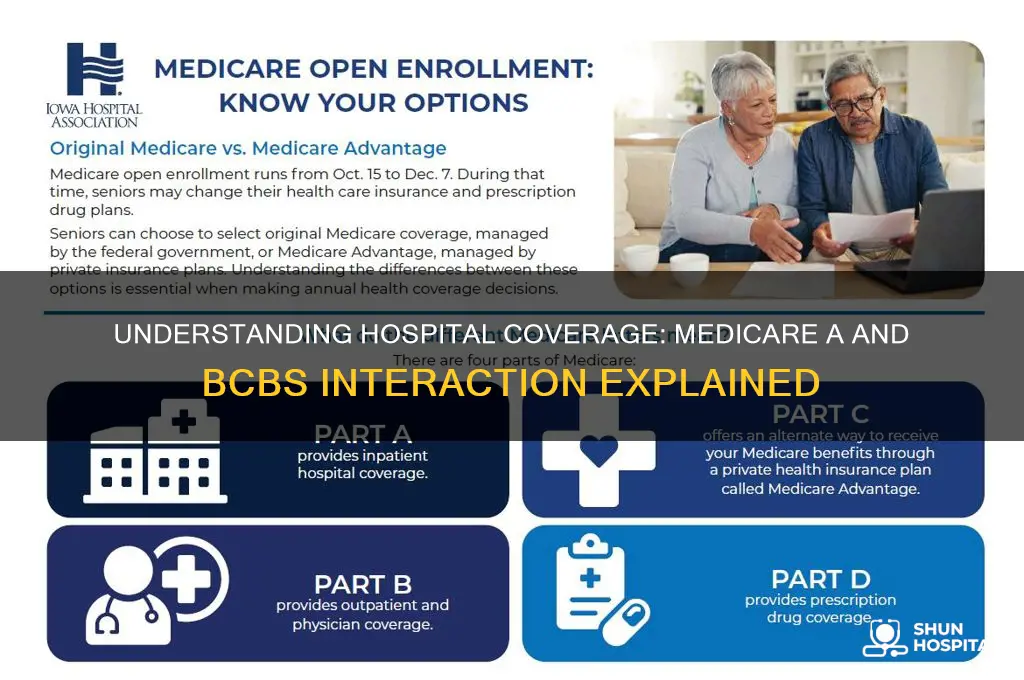

Medicare A coverage limits in hospitals

Medicare Part A, often referred to as hospital insurance, is a critical component of healthcare coverage for individuals aged 65 and older, as well as certain younger people with disabilities. When it comes to hospital coverage, understanding the limits of Medicare Part A is essential for beneficiaries to navigate their healthcare needs effectively. One of the primary coverage limits under Medicare Part A is the benefit period, which begins the day a patient is admitted to a hospital or skilled nursing facility (SNF) and ends when they have been out of the hospital or SNF for 60 consecutive days. During this benefit period, Medicare Part A covers up to 90 days of inpatient hospital care, but with specific conditions. For the first 60 days, there is no coinsurance cost for the beneficiary, but from day 61 to day 90, a daily coinsurance fee applies, which can be substantial.

Beyond the initial 90 days, Medicare Part A provides an additional lifetime reserve of 60 days, often called "lifetime reserve days." These days can only be used once during a beneficiary's lifetime and come with a high daily coinsurance cost. Once these reserve days are used, Medicare Part A will no longer cover inpatient hospital stays, and the beneficiary becomes responsible for all costs unless they have supplemental insurance. It’s important to note that Medicare Part A does not cover long-term or indefinite hospital stays; it is designed for short-term acute care needs. After the 90th day of hospitalization, if a beneficiary has not used their lifetime reserve days, they must either pay out-of-pocket for continued care or rely on other insurance coverage, such as Blue Cross Blue Shield (BCBS) or a Medicare Supplement plan, to cover the gap.

Another critical aspect of Medicare Part A’s coverage limits in hospitals is the requirement for a three-day inpatient stay before Medicare will cover care in a skilled nursing facility. This means that if a patient is admitted to a hospital as an outpatient or under observation, those days do not count toward the three-day requirement, potentially leaving the beneficiary responsible for SNF costs. This "observation status" loophole has been a source of confusion and financial burden for many Medicare beneficiaries, highlighting the importance of understanding the nuances of Part A coverage. Beneficiaries should always confirm their admission status with the hospital to ensure they meet the criteria for SNF coverage under Medicare Part A.

In the context of how Medicare Part A interacts with BCBS or other supplemental insurance, it’s crucial to recognize that Medicare Part A is the primary payer for hospital services, but it does not cover all costs. BCBS or other supplemental plans can help cover deductibles, coinsurance, and copayments that Medicare Part A does not fully cover. For example, if a beneficiary exhausts their 90 days of inpatient hospital coverage under Part A, a BCBS plan might provide additional coverage for extended stays, depending on the policy. However, beneficiaries should carefully review their BCBS policy to understand its limitations, as not all plans cover the same services or costs. Coordination between Medicare Part A and BCBS is essential to maximize coverage and minimize out-of-pocket expenses.

Lastly, Medicare Part A’s coverage limits also extend to mental health care in hospitals. Part A covers up to 190 days of inpatient psychiatric hospital care in a beneficiary’s lifetime, but this is separate from the 90-day benefit period for general inpatient care. Once the 190-day limit is reached, Medicare will no longer cover psychiatric hospital stays, and beneficiaries must rely on other insurance or pay out-of-pocket. This lifetime limit underscores the importance of beneficiaries planning for potential gaps in coverage, especially for those with chronic or severe mental health conditions. Understanding these limits and how they interact with supplemental insurance like BCBS is vital for beneficiaries to make informed decisions about their healthcare and financial planning.

Discover the Location of Hospitality Building on USF Campus

You may want to see also

Explore related products

![]()

BCBS hospital network restrictions

When considering how hospital coverage interacts with Medicare Part A and Blue Cross Blue Shield (BCBS), it’s essential to understand the restrictions within the BCBS hospital network. BCBS, like many private insurers, operates through a network of healthcare providers, including hospitals, which have agreed to provide services at negotiated rates. If a hospital is in-network with BCBS, the insurer typically covers a larger portion of the costs, while out-of-network hospitals may result in higher out-of-pocket expenses or limited coverage. For individuals with both Medicare Part A and BCBS (often through a Medicare Supplement or Advantage plan), the interaction between these networks becomes critical. Medicare Part A covers inpatient hospital stays, but BCBS may impose additional restrictions based on its network agreements.

One key restriction is that BCBS plans often require policyholders to use in-network hospitals to receive full coverage benefits. If a hospital is not in the BCBS network, the insurer may deny coverage entirely or significantly reduce the amount paid, leaving the patient responsible for the remaining balance. This is particularly important for individuals with Medicare Part A, as Part A only covers 80% of inpatient costs after the deductible, and BCBS (as a supplement) typically covers the remaining 20%. However, if the hospital is out-of-network, BCBS may not fulfill its supplemental role, leaving the patient with unexpected costs.

Another restriction arises in BCBS Medicare Advantage plans, which often have narrower networks compared to traditional BCBS plans. These plans combine Medicare Part A and Part B benefits and may include additional coverage like prescription drugs. However, they typically require policyholders to use hospitals within their specific network. If a patient seeks care at an out-of-network hospital, the costs may not be covered unless it’s an emergency situation. This can be confusing for individuals who assume Medicare Part A provides universal hospital coverage, as BCBS network restrictions can limit access to certain facilities.

BCBS may also impose prior authorization requirements for certain hospital services, even within its network. This means that before a procedure or admission is covered, the hospital or physician must obtain approval from BCBS. Failure to comply with these requirements can result in denied claims, even if the hospital is in-network. For patients with Medicare Part A, this adds an extra layer of complexity, as they must navigate both Medicare’s coverage rules and BCBS’s authorization processes.

Lastly, BCBS network restrictions can vary by plan type and geographic location. For example, a BCBS plan in one state may have a different network of hospitals compared to another state. This variability requires individuals to carefully review their plan’s network list and understand which hospitals are covered. For those with Medicare Part A, it’s crucial to ensure that the BCBS network aligns with their preferred hospitals, as Medicare Part A does not override BCBS network restrictions. In summary, while Medicare Part A provides foundational hospital coverage, BCBS network restrictions can significantly impact access and costs, making it essential to understand these limitations when choosing a plan.

Black Widow Bite: Uncovering the Cost of Hospital Treatment

You may want to see also

Explore related products

![]()

Coordination between Medicare A and BCBS

When it comes to understanding how hospital coverage interacts with Medicare Part A and Blue Cross Blue Shield (BCBS), coordination between these two entities is crucial for maximizing benefits and minimizing out-of-pocket expenses. Medicare Part A, often referred to as hospital insurance, covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care services. BCBS, on the other hand, is a private insurance provider that offers supplemental coverage, which can include hospital services, doctor visits, and prescription drugs, depending on the plan. The coordination between Medicare Part A and BCBS ensures that beneficiaries receive comprehensive coverage without gaps or duplications.

In the context of hospital coverage, Medicare Part A typically serves as the primary payer for inpatient hospital services. This means that when a Medicare beneficiary is admitted to a hospital, Medicare Part A will cover the majority of the costs, including room and board, nursing care, and other medically necessary services. However, Medicare Part A does not cover all expenses, such as deductibles, coinsurance, and copayments. This is where BCBS comes into play as a secondary payer. BCBS plans, often referred to as Medigap policies, are designed to fill in the gaps left by Medicare, covering costs that Medicare Part A does not, such as the Part A deductible and coinsurance for hospital stays beyond 60 days.

Coordination between Medicare Part A and BCBS is facilitated through a process known as "coordination of benefits" (COB). During COB, the two insurers communicate to determine which plan is the primary payer and which is the secondary payer. For hospital services, Medicare Part A is almost always the primary payer, and BCBS acts as the secondary payer. This coordination ensures that claims are processed correctly, and beneficiaries are not overcharged or left with unexpected bills. It is essential for beneficiaries to inform both Medicare and BCBS when they receive hospital services to ensure seamless coordination and accurate billing.

Another critical aspect of coordination between Medicare Part A and BCBS is understanding the specific benefits and limitations of each plan. For instance, while Medicare Part A covers inpatient hospital stays, it does not cover custodial care or long-term care in a nursing home. BCBS plans may offer additional coverage for these services, depending on the policy. Beneficiaries should review their BCBS policy details to understand what is covered beyond Medicare Part A. Additionally, some BCBS plans may offer extra benefits, such as coverage for emergency medical services abroad, which are not covered by Medicare Part A.

Effective coordination also involves being aware of enrollment periods and eligibility requirements for both Medicare Part A and BCBS. Medicare Part A is typically available to individuals aged 65 and older, as well as certain younger individuals with disabilities. BCBS Medigap policies have specific enrollment periods, such as the initial enrollment period when one first becomes eligible for Medicare Part B. Missing these enrollment periods can result in higher premiums or limited plan options. Beneficiaries should plan their enrollment carefully to ensure continuous and coordinated coverage between Medicare Part A and BCBS.

Lastly, beneficiaries should maintain open communication with both Medicare and BCBS to address any issues that arise during the coordination process. This includes verifying that providers accept both Medicare and BCBS, understanding pre-authorization requirements, and keeping track of claims and explanations of benefits (EOBs). By staying informed and proactive, beneficiaries can ensure that the coordination between Medicare Part A and BCBS works in their favor, providing comprehensive hospital coverage and peace of mind.

Hospital Horrors: Why Do People Get Grossed Out?

You may want to see also

Explore related products

![]()

Out-of-pocket costs with dual coverage

When you have dual coverage through Medicare Part A and Blue Cross Blue Shield (BCBS), understanding your out-of-pocket costs is crucial for managing healthcare expenses effectively. Medicare Part A typically covers inpatient hospital stays, skilled nursing facility care, and some home health care, but it does not cover all costs. For instance, beneficiaries are responsible for a deductible per benefit period, which can change annually. In 2023, the Part A deductible is $1,600 per benefit period. If your hospital stay extends beyond 60 days, you’ll also face daily coinsurance costs, which increase significantly after 90 days. BCBS, as a secondary insurer, may cover some of these out-of-pocket costs, but the extent of coverage depends on your specific plan.

BCBS, as a secondary payer, coordinates benefits with Medicare to reduce your out-of-pocket expenses. After Medicare pays its portion, BCBS may cover some or all of the remaining costs, such as deductibles, copayments, and coinsurance. However, this depends on whether you have a Medigap (Supplemental) plan or a Medicare Advantage plan through BCBS. Medigap plans are designed to fill the gaps in Original Medicare, potentially reducing out-of-pocket costs significantly. For example, Medigap Plan G covers the Part A deductible and coinsurance, leaving you with minimal expenses for hospital stays. In contrast, Medicare Advantage plans through BCBS may have different cost-sharing structures, including copays and maximum out-of-pocket limits, which can vary widely.

One key consideration with dual coverage is understanding which insurer is primary and which is secondary. Medicare is typically the primary payer for hospital services if you have Original Medicare. BCBS then steps in as the secondary payer to cover costs Medicare doesn’t. However, if you have a BCBS Medicare Advantage plan, BCBS becomes the primary payer, and the plan’s rules dictate your out-of-pocket costs. This distinction is critical because it determines how much you’ll pay for services like hospital stays, surgeries, or emergency care. Always verify with both insurers how costs will be split to avoid unexpected bills.

Out-of-pocket costs can also arise from services not fully covered by either Medicare or BCBS. For example, Medicare Part A does not cover long-term care or custodial care, and BCBS may not cover these services either, depending on your plan. Additionally, if you receive care from a provider who does not accept Medicare assignment, you may face higher out-of-pocket costs, as BCBS may not cover the excess charges. It’s essential to check your BCBS plan’s network and coverage details to understand what is and isn’t covered when Medicare is involved.

Finally, prescription drug coverage is another area where out-of-pocket costs can add up, even with dual coverage. Medicare Part A does not cover prescription drugs, so you’ll need a Part D plan or a BCBS plan that includes prescription coverage. If you have both, Medicare Part D is typically the primary payer for medications, and BCBS may provide additional coverage for drugs not covered by Part D. However, you may still face copays, deductibles, or coverage gaps, such as the Part D “donut hole.” Reviewing both plans’ drug formularies and cost-sharing structures can help you minimize out-of-pocket expenses for medications.

In summary, dual coverage with Medicare Part A and BCBS can significantly reduce out-of-pocket costs, but it requires careful coordination and understanding of both plans. Medicare Part A covers hospital stays but leaves beneficiaries with deductibles and coinsurance, which BCBS may cover as the secondary payer. The type of BCBS plan you have (Medigap or Medicare Advantage) greatly influences your costs. Always verify how expenses are split between the two insurers, and be aware of services not covered by either plan. By proactively managing your dual coverage, you can better control healthcare expenses and avoid financial surprises.

Volunteering at Hospitals: A Rewarding Experience

You may want to see also

Explore related products

![]()

Hospital billing processes for dual plans

When a patient has dual coverage through Medicare Part A and Blue Cross Blue Shield (BCBS), hospital billing processes become more intricate but follow a structured coordination of benefits (COB) framework. Medicare Part A typically serves as the primary payer for hospital services, covering inpatient stays, skilled nursing facility care, and some home health services. BCBS, as the secondary payer, steps in to cover costs that Medicare does not fully pay, such as deductibles, coinsurance, or services not covered by Medicare. Hospitals must first bill Medicare Part A for covered services and await their payment determination before submitting a secondary claim to BCBS. This sequential billing ensures compliance with federal regulations and maximizes reimbursement for both the hospital and the patient.

The hospital billing process begins with verifying the patient’s eligibility under both Medicare Part A and BCBS. This involves confirming active coverage, understanding the specifics of each plan, and identifying which plan is primary and which is secondary. Once eligibility is confirmed, the hospital submits a claim to Medicare Part A, which processes the claim based on its fee schedule and coverage rules. Medicare pays its portion directly to the hospital, and the Explanation of Benefits (EOB) from Medicare outlines the approved amount, patient responsibility, and any unpaid balance. This EOB is critical for the next step in the billing process.

After receiving the Medicare EOB, the hospital submits a secondary claim to BCBS, attaching the Medicare EOB to the claim. BCBS then processes the claim to cover the remaining balance, including deductibles, coinsurance, or services not covered by Medicare. BCBS’s payment is contingent on the terms of the patient’s policy, such as whether it includes supplemental coverage for Medicare gaps. Hospitals must carefully review BCBS’s Explanation of Benefits to ensure accurate payment and identify any patient responsibility, such as copays or non-covered services. This two-step process requires meticulous documentation and adherence to both Medicare and BCBS billing guidelines.

One challenge in dual-plan billing is coordinating benefits to avoid overpayment or underpayment. Hospitals must understand the COB rules, which dictate the order of payment and the responsibilities of each insurer. For instance, if BCBS is the primary payer for certain services not covered by Medicare, the hospital must bill BCBS first. Additionally, hospitals must be aware of BCBS policies that may limit coverage when Medicare is involved, such as exclusions for services already covered by Medicare. Proper training for billing staff and the use of billing software that handles COB rules can streamline this process and reduce errors.

Finally, patient communication is essential in dual-plan billing. Hospitals should provide clear explanations of how Medicare Part A and BCBS interact, including what each plan covers and the patient’s financial responsibility. Patients should receive itemized bills that detail Medicare’s payment, BCBS’s payment, and any remaining balance. Transparency in billing helps build trust and ensures patients understand their obligations. Hospitals should also have a process for addressing patient inquiries or disputes related to dual-plan billing, such as discrepancies between Medicare and BCBS payments or unexpected out-of-pocket costs. Effective management of dual-plan billing not only ensures compliance but also enhances patient satisfaction and financial outcomes for the hospital.

Charity Hospitals in Louisiana: Where Are They?

You may want to see also

Frequently asked questions

Medicare Part A primarily covers inpatient hospital stays, including semi-private rooms, meals, general nursing, and other hospital services. It also covers care in skilled nursing facilities, hospice, and home health care under certain conditions. Most people do not pay a premium for Part A if they or their spouse paid Medicare taxes while working.

Yes, you can have both Medicare Part A and BCBS coverage. BCBS plans, such as Medicare Supplement (Medigap) policies or Medicare Advantage plans, can help cover costs that Medicare Part A doesn’t, like deductibles, copayments, and coinsurance. Coordination between the two depends on the specific BCBS plan you have.

BCBS plans may cover additional hospital services or costs not covered by Medicare Part A, depending on the plan. For example, some BCBS plans may cover extended hospital stays beyond Medicare limits or provide coverage for certain treatments not included in Part A. Always check your specific BCBS plan details for exact coverage.