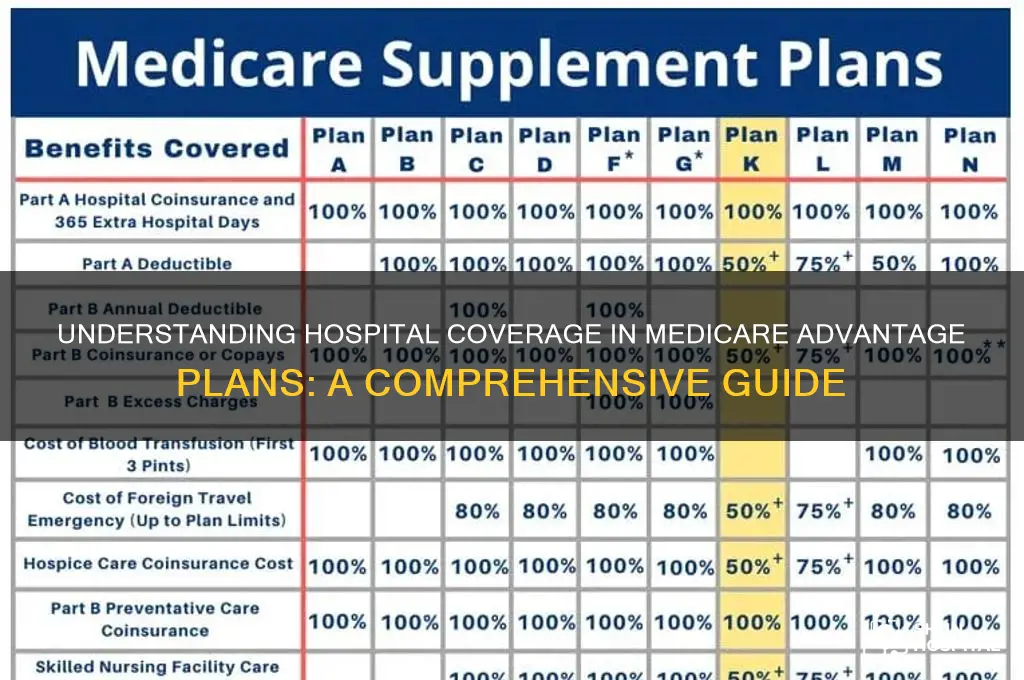

Hospital coverage under a Medicare Advantage plan, also known as Medicare Part C, is typically more comprehensive than Original Medicare, as these plans are offered by private insurance companies approved by Medicare. Medicare Advantage plans often include Part A (hospital insurance) and Part B (medical insurance) benefits, along with additional services like prescription drug coverage, vision, dental, and hearing care. When it comes to hospital stays, Medicare Advantage plans usually cover inpatient care, skilled nursing facility stays, and hospice care, similar to Original Medicare. However, the specifics of coverage, such as copayments, coinsurance, and deductibles, can vary depending on the plan. It’s essential for beneficiaries to review their plan’s Summary of Benefits to understand their out-of-pocket costs and any network restrictions, as some plans may require using in-network hospitals to maximize coverage. Additionally, prior authorization may be needed for certain hospital services, so understanding these requirements is crucial for seamless care.

Explore related products

What You'll Learn

- In-network vs. out-of-network hospitals: Coverage differences and costs for Medicare Advantage plan members

- Prior authorization requirements: When and how hospitals need approval for services under the plan

- Emergency room coverage: Medicare Advantage plan policies for emergency hospital visits and care

- Specialist referrals: Rules for accessing hospital-based specialists under your Medicare Advantage plan

- Out-of-area coverage: Hospital services available when traveling outside your plan’s service area

![]()

In-network vs. out-of-network hospitals: Coverage differences and costs for Medicare Advantage plan members

Medicare Advantage (MA) plans, also known as Medicare Part C, offer an alternative to Original Medicare by providing coverage through private insurance companies. One critical aspect of these plans is how they handle hospital coverage, particularly the differences between in-network and out-of-network hospitals. Understanding these distinctions is essential for MA plan members to manage costs and ensure access to necessary care. In-network hospitals are facilities that have agreements with the MA plan provider, while out-of-network hospitals do not. MA plans typically encourage members to use in-network hospitals by offering lower out-of-pocket costs and streamlined coverage.

Coverage Differences: In-network hospitals provide comprehensive coverage under MA plans, often with predictable copayments or coinsurance. Members usually pay less for services like inpatient stays, emergency care, and surgeries when using in-network facilities. Out-of-network hospitals, on the other hand, may have limited coverage or require higher out-of-pocket expenses. Some MA plans may not cover out-of-network hospital services at all, except in emergencies. It’s crucial for members to verify their plan’s specific policies regarding out-of-network care to avoid unexpected costs.

Cost Implications: The cost differences between in-network and out-of-network hospitals can be significant. In-network hospital services are generally more affordable due to pre-negotiated rates between the plan and the hospital. Members often face lower deductibles, copayments, and coinsurance when staying within the network. Out-of-network hospitals may charge higher rates, and members could be responsible for a larger portion of the bill. Additionally, some MA plans impose out-of-network deductibles or require prior authorization for non-emergency out-of-network care, further complicating cost management.

Emergency Care Exceptions: One important exception to in-network vs. out-of-network distinctions is emergency care. Regardless of whether a hospital is in-network or out-of-network, MA plans are required by law to cover emergency services. Members cannot be charged higher out-of-pocket costs for emergency care received at an out-of-network hospital. However, non-emergency care received at an out-of-network hospital during the same visit may not be covered or could result in higher costs.

Plan Variations and Provider Directories: MA plans vary widely in their network structures and coverage rules. Some plans, like Health Maintenance Organizations (HMOs), may require members to use in-network hospitals exclusively, except in emergencies. Others, like Preferred Provider Organizations (PPOs), offer more flexibility but still incentivize in-network usage with lower costs. Members should consult their plan’s provider directory to identify in-network hospitals and understand the specific coverage and cost implications of using out-of-network facilities.

In summary, Medicare Advantage plan members must carefully consider the differences between in-network and out-of-network hospitals to optimize their coverage and manage costs. While in-network hospitals offer predictable and affordable care, out-of-network facilities can lead to higher expenses and limited coverage. Familiarizing oneself with plan details, including emergency care exceptions and network restrictions, is essential for making informed healthcare decisions.

Johns Hopkins Hospital: Where to Park?

You may want to see also

Explore related products

![Vakly Extra Large Super-Absorbent Contoured Hospital Style Pad Liners [Pack of 20] 7" Wide X 14" Long - Maternity Pads for Heavier Post Birth Protection - Incontinence Liners 7x14 inches](https://m.media-amazon.com/images/I/613EQTRmDYL._AC_UL320_.jpg)

![]()

Prior authorization requirements: When and how hospitals need approval for services under the plan

Under a Medicare Advantage (MA) plan, prior authorization requirements play a critical role in managing hospital services, ensuring that care is both medically necessary and cost-effective. Prior authorization is a process where hospitals must obtain approval from the MA plan before performing certain procedures or admitting patients for specific treatments. This requirement is designed to prevent unnecessary or inappropriate care, reduce costs, and ensure that services align with the plan’s coverage guidelines. Hospitals must be familiar with the specific prior authorization rules of the MA plan they are working with, as these can vary significantly between different insurers.

The need for prior authorization typically arises for high-cost, elective, or specialized services, such as surgeries, advanced imaging (e.g., MRIs, CT scans), inpatient admissions, and certain outpatient procedures. For example, if a patient requires a joint replacement surgery, the hospital must submit a request to the MA plan detailing the medical necessity of the procedure, supported by clinical documentation. The plan then reviews the request to determine if the service meets its criteria for coverage. Failure to obtain prior authorization when required can result in denied claims, leaving the hospital or patient financially responsible for the service.

The process for obtaining prior authorization involves several steps. First, the hospital’s healthcare provider must submit a request to the MA plan, often through an online portal, fax, or phone call. This request must include specific information, such as the patient’s diagnosis, the proposed service, and supporting medical records. The plan then reviews the request, which may take anywhere from a few hours to several days, depending on the urgency of the service and the plan’s policies. Hospitals should be proactive in submitting requests well in advance to avoid delays in patient care, especially for scheduled procedures.

It is essential for hospitals to understand the timelines and exceptions to prior authorization requirements. Some MA plans offer expedited review processes for urgent or emergency situations, ensuring that patients receive timely care. Additionally, certain services may be exempt from prior authorization, such as emergency room visits or routine care for chronic conditions. Hospitals should carefully review the plan’s provider manual or contact the insurer directly to clarify which services require prior authorization and under what circumstances.

Non-compliance with prior authorization requirements can have significant financial and operational consequences for hospitals. Denied claims due to lack of prior authorization can lead to lost revenue and administrative burdens associated with appeals. To mitigate these risks, hospitals should implement robust systems for tracking and managing prior authorization requests, including assigning dedicated staff to handle these tasks. Training healthcare providers and administrative staff on the importance of prior authorization and the specific requirements of each MA plan is also crucial.

In summary, prior authorization is a key component of hospital coverage under Medicare Advantage plans, ensuring that services are medically necessary and align with the plan’s guidelines. Hospitals must navigate this process carefully, understanding when prior authorization is required, how to submit requests, and the potential consequences of non-compliance. By staying informed and organized, hospitals can minimize disruptions to patient care and maintain financial stability while working within the framework of MA plans.

UAB Hospital: University-Run or Independent Entity?

You may want to see also

Explore related products

$24.99 $29.99

$28.04 $37.99

![]()

Emergency room coverage: Medicare Advantage plan policies for emergency hospital visits and care

Medicare Advantage plans, also known as Medicare Part C, are required to cover emergency services, ensuring that beneficiaries have access to urgent care when needed. These plans must provide coverage for emergency room visits in the same way that Original Medicare does, but with some specific policies and procedures in place. When a Medicare Advantage plan member experiences a medical emergency, they can seek treatment at any emergency room, regardless of whether the hospital is within the plan's network. This is a crucial aspect of emergency care, as it allows individuals to receive immediate attention without the added stress of finding an in-network facility during a crisis.

In the context of emergency room coverage, Medicare Advantage plans typically cover services such as emergency room physician fees, hospital services, and ambulance transportation. The plan will generally pay for these services at the same rate as Original Medicare, ensuring that beneficiaries are not burdened with additional costs. However, it is important to note that some plans may require prior authorization for non-emergency ambulance transportation, so members should be aware of their plan's specific requirements. During an emergency, the focus is on providing immediate care, and Medicare Advantage plans are designed to facilitate this by offering comprehensive coverage.

One key aspect of Medicare Advantage plans is their utilization of provider networks. While emergency services are covered both in-network and out-of-network, the plan's network can still play a role in cost-sharing. If a plan member visits an in-network emergency room, they may have lower out-of-pocket costs, such as copayments or coinsurance, compared to visiting an out-of-network facility. It is advisable for beneficiaries to understand their plan's network and associated costs to make informed decisions, especially when it comes to follow-up care after an emergency, which may be subject to different coverage rules.

After receiving emergency care, Medicare Advantage plan members should be aware of the potential need for prior authorization for subsequent hospital services. This means that if a patient is admitted to the hospital following an emergency room visit, the plan may require approval for continued care. This process ensures that the services provided are medically necessary and covered under the plan's benefits. Beneficiaries should familiarize themselves with their plan's prior authorization requirements to avoid unexpected costs and ensure a smooth transition from emergency care to any necessary ongoing treatment.

In summary, Medicare Advantage plans offer comprehensive emergency room coverage, allowing members to access urgent care without the constraints of provider networks during critical situations. These plans cover essential services, including physician fees and ambulance transportation, at levels comparable to Original Medicare. Understanding the nuances of in-network and out-of-network costs, as well as prior authorization requirements, empowers beneficiaries to navigate emergency hospital visits and subsequent care effectively, ensuring they receive the necessary treatment without unforeseen financial burdens. This aspect of Medicare Advantage plans provides peace of mind and financial protection during medical emergencies.

Coastal Carolina Hospital Food Delivery Services: Who Brings Meals?

You may want to see also

Explore related products

$26.99 $32.99

![]()

Specialist referrals: Rules for accessing hospital-based specialists under your Medicare Advantage plan

Under a Medicare Advantage (MA) plan, accessing hospital-based specialists typically requires adherence to specific referral rules designed to manage care coordination and costs. Unlike Original Medicare, which allows beneficiaries to visit any specialist who accepts Medicare, MA plans often operate within a network of providers. To see a hospital-based specialist, you usually need a referral from your primary care physician (PCP). This referral ensures that the specialist visit is medically necessary and aligns with your overall care plan. Without a proper referral, the MA plan may not cover the specialist visit, leaving you responsible for out-of-pocket costs.

The process for obtaining a referral varies by plan but generally involves scheduling an appointment with your PCP to discuss your symptoms or condition. If your PCP determines that a specialist consultation is needed, they will initiate the referral process, which may include submitting documentation to the MA plan for approval. Some MA plans require pre-authorization for specialist visits, especially for hospital-based specialists, to ensure the service is covered under your plan’s benefits. It’s crucial to understand your plan’s specific referral and authorization requirements to avoid unexpected expenses.

In some cases, MA plans may allow out-of-network referrals for hospital-based specialists if in-network options are unavailable or inadequate. However, these out-of-network referrals often come with higher out-of-pocket costs. Beneficiaries should carefully review their plan’s network directory to identify in-network hospital-based specialists. If a referral to an out-of-network specialist is necessary, contact your plan to understand the coverage limitations and potential costs.

For urgent or emergency situations, MA plans typically waive referral requirements, allowing you to access hospital-based specialists directly. However, it’s important to notify your plan as soon as possible after receiving emergency care to ensure proper billing and coverage. Non-emergency care without a referral may not be covered, so always consult your plan’s guidelines or customer service for clarification.

Lastly, some MA plans, particularly Health Maintenance Organizations (HMOs), have stricter referral rules compared to Preferred Provider Organizations (PPOs). HMO plans often require all specialist visits to be coordinated through your PCP, while PPOs may offer more flexibility in accessing specialists directly, though still within the plan’s network. Understanding your plan type and its referral policies is essential for navigating hospital-based specialist care under Medicare Advantage. Always review your plan’s Evidence of Coverage (EOC) document for detailed information on specialist referrals and hospital coverage.

Language Training: A Hospital Budget Priority?

You may want to see also

Explore related products

$28.99

![]()

Out-of-area coverage: Hospital services available when traveling outside your plan’s service area

When you're enrolled in a Medicare Advantage plan and find yourself traveling outside your plan's service area, understanding your out-of-area hospital coverage is crucial. Medicare Advantage plans, also known as Medicare Part C, typically have a network of healthcare providers within a specific geographic region. However, most plans offer some level of coverage for emergency and urgent care services when you're away from home. In the event of an emergency, you can seek treatment at any hospital that accepts Medicare, regardless of whether it's in your plan's network or not. This ensures that you have access to necessary medical care when unexpected situations arise during your travels.

Out-of-area coverage for hospital services under a Medicare Advantage plan generally includes emergency care and urgent care needs. Emergency services are covered worldwide, meaning if you require immediate medical attention due to a sudden illness or injury, your plan will cover the costs, typically at the same rate as in-network services. For urgent care, which refers to situations that require prompt medical attention but are not life-threatening, coverage may vary. Some plans might require you to pay a higher copayment or coinsurance for out-of-network urgent care services, so it's essential to review your plan's specifics.

It's important to note that non-emergency hospital services are usually not covered outside your plan's service area. This means that if you're traveling and need a scheduled hospital procedure or treatment that can wait until you return home, it's advisable to do so. However, if your health condition changes and becomes an emergency while waiting, you would then be covered for the necessary emergency services. Understanding this distinction can help you make informed decisions about your healthcare when traveling.

To make the most of your out-of-area coverage, it's recommended to carry your Medicare Advantage plan ID card with you at all times when traveling. This card provides essential information about your plan and can facilitate the billing process at out-of-network hospitals. Additionally, contacting your plan's customer service before seeking non-emergency care can help clarify coverage details and potentially save you from unexpected costs. Being proactive and informed about your coverage ensures that you can focus on your health and enjoy your travels with peace of mind.

In summary, out-of-area hospital coverage under a Medicare Advantage plan primarily focuses on emergency and urgent care services when you're outside your plan's service area. While emergency care is comprehensively covered, urgent care coverage may come with additional costs. Non-emergency services are typically not covered, emphasizing the importance of planning ahead for any scheduled medical needs. By familiarizing yourself with these coverage details and keeping your plan information handy, you can navigate healthcare services effectively during your travels.

New York Methodist Hospital's Opening: A Historical Overview

You may want to see also

Frequently asked questions

A Medicare Advantage plan (Part C) is an all-in-one alternative to Original Medicare (Part A and Part B) offered by private insurance companies. It typically includes hospital coverage (Part A), medical coverage (Part B), and often prescription drug coverage (Part D). Unlike Original Medicare, Medicare Advantage plans may have different provider networks, costs, and additional benefits, but they must cover at least the same hospital services as Original Medicare.

Yes, Medicare Advantage plans cover inpatient hospital stays, just like Original Medicare Part A. This includes semi-private rooms, meals, general nursing, and other hospital services and supplies for medically necessary stays. However, costs like copays or coinsurance may vary depending on the specific plan.

Yes, out-of-pocket costs for hospital coverage under a Medicare Advantage plan can include copayments, coinsurance, or deductibles. These costs vary by plan, and some plans may offer $0 premiums or lower out-of-pocket maximums. It’s important to review your plan’s Summary of Benefits to understand your financial responsibility.

Most Medicare Advantage plans have provider networks, meaning you may need to use specific hospitals or facilities to receive full coverage. Some plans, like HMOs, require you to stay in-network (except for emergencies), while PPOs may allow out-of-network care at a higher cost. Always check your plan’s network before seeking hospital care.

Yes, Medicare Advantage plans cover emergency hospital visits, regardless of whether the hospital is in-network or out-of-network. You have the right to receive emergency care anywhere in the U.S. and its territories, and your plan cannot require prior authorization for emergency services. However, you may still be responsible for copays or coinsurance.

![Vakly Extra Long Postpartum Maternity Pads with Tails [24 Pack] Large 3''x20'' Maximum Absorbency Heavy Flow Postpartum Incontinence Pads - Ultra Soft Disposable Nursing Pads for New Moms (24)](https://m.media-amazon.com/images/I/71k6WhXNFfL._AC_UL320_.jpg)