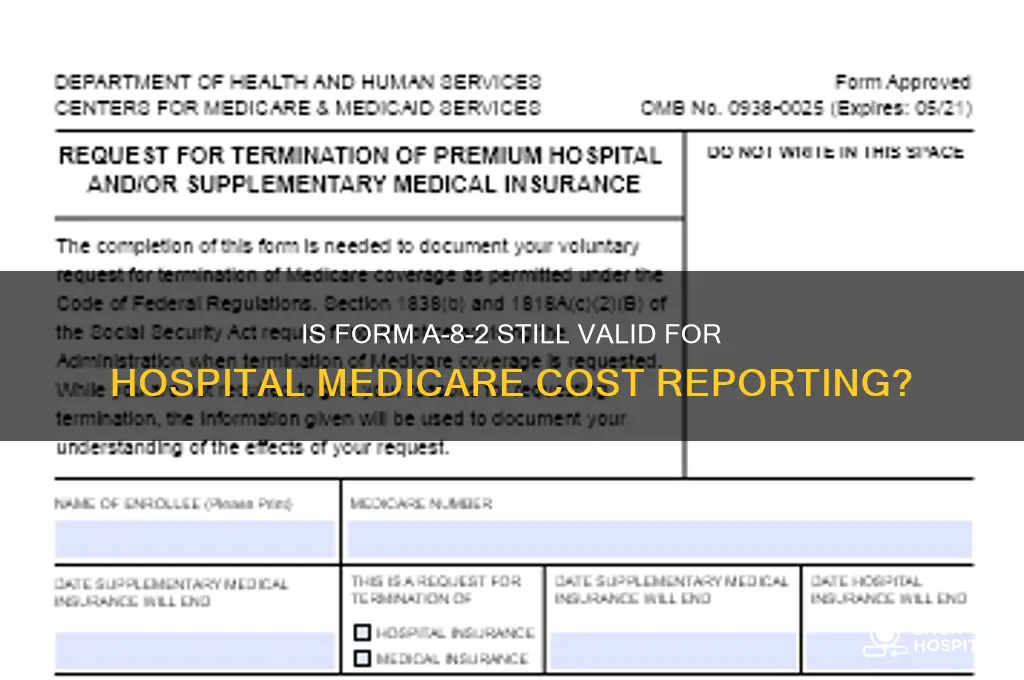

The question of whether Form A-8-2 remains applicable for hospital Medicare cost reporting is a critical concern for healthcare providers navigating the complexities of Medicare reimbursement. As Medicare regulations and reporting requirements evolve, it is essential to verify the current status and relevance of specific forms like A-8-2, which historically played a role in cost reporting processes. Hospitals must stay informed about updates from the Centers for Medicare & Medicaid Services (CMS) to ensure compliance and avoid potential financial penalties. Consulting the latest CMS guidelines or seeking expert advice can provide clarity on whether Form A-8-2 is still required or if alternative reporting mechanisms have been introduced.

Explore related products

What You'll Learn

![]()

Current A-8-2 Form Validity

The A-8-2 form, historically integral to Medicare cost reporting for hospitals, has undergone significant scrutiny in recent years. As of the latest updates from the Centers for Medicare & Medicaid Services (CMS), the form’s applicability hinges on specific conditions and reporting periods. Hospitals must verify whether their fiscal year aligns with CMS’s current requirements, as the agency has phased out certain sections of the A-8-2 in favor of streamlined reporting mechanisms. For instance, Worksheet A, Part III, which previously detailed bad debt calculations, is no longer mandatory for all providers, reducing administrative burden but requiring careful attention to alternative reporting methods.

To determine the form’s validity, hospitals should cross-reference their fiscal year-end with CMS’s Transition Period guidelines. Providers with fiscal years ending on or after September 30, 2023, are exempt from using the A-8-2 for certain cost centers, such as inpatient services, where the Healthcare Common Procedure Coding System (HCPCS) now governs reimbursement. However, critical access hospitals (CAHs) and facilities in rural areas may still need to file specific sections of the A-8-2, particularly for outpatient services and swing-bed utilization. This disparity underscores the importance of tailoring compliance efforts to facility type and location.

Practical steps for ensuring compliance include conducting a fiscal year audit to confirm reporting obligations and consulting CMS’s Provider Reimbursement Manual (Part 2, Chapter 27) for detailed instructions. Hospitals should also leverage software tools that integrate HCPCS coding with legacy A-8-2 requirements, ensuring seamless transitions during the phase-out period. For example, systems like Meditech and Cerner offer modules that flag outdated form sections while auto-populating relevant data into newer formats, minimizing errors and saving time.

A comparative analysis reveals that while the A-8-2’s obsolescence is evident in urban, large-scale hospitals, smaller facilities face a steeper learning curve. Rural providers, often reliant on the A-8-2 for decades, must invest in staff training and system upgrades to adapt to HCPCS-based reporting. CMS workshops and webinars provide invaluable resources, offering step-by-step guidance on transitioning from the A-8-2 to modern frameworks. Hospitals that proactively address these changes can avoid penalties and optimize Medicare reimbursements.

In conclusion, the A-8-2 form’s validity is contingent on a hospital’s fiscal year, facility type, and geographic location. While its role is diminishing, residual sections remain applicable for specific providers and services. By staying informed, leveraging technology, and engaging with CMS resources, hospitals can navigate this transition effectively, ensuring compliance without sacrificing operational efficiency.

NYC Hospitals: Abortion Access and Availability

You may want to see also

Explore related products

![OMNIHIL [UL Listed] 8 Feet Long AC Power Cord Compatible with Formlabs Form 2 SN OrganicFinch 3D Printer.](https://m.media-amazon.com/images/I/61xPTu7UgXL._AC_UL320_.jpg)

![]()

Medicare Cost Reporting Changes

The Medicare cost reporting landscape has undergone significant changes in recent years, leaving many hospitals questioning the relevance of Form A-8-2. This form, once a cornerstone of Medicare cost reporting, has been largely replaced by the UB-04 claim form for inpatient hospital services. The Centers for Medicare & Medicaid Services (CMS) made this transition to streamline the billing process and reduce administrative burden on healthcare providers.

One of the primary drivers behind this change is the increasing complexity of Medicare reimbursement methodologies. The introduction of the Medicare Severity Diagnosis Related Group (MS-DRG) system, for instance, requires hospitals to report more detailed patient data, including diagnosis codes, procedure codes, and severity of illness. The UB-04 form is better equipped to capture this information, enabling CMS to calculate reimbursement rates more accurately. In contrast, Form A-8-2 was designed for a simpler reimbursement system and lacks the necessary fields to accommodate the nuances of MS-DRG.

To navigate these changes, hospitals must ensure their billing and coding staff are well-versed in the UB-04 form and the associated coding guidelines. This includes understanding the importance of accurate diagnosis coding, as it directly impacts MS-DRG assignment and reimbursement. For example, a patient with a principal diagnosis of pneumonia (J18.9) and a secondary diagnosis of respiratory failure (J96.90) would be assigned to a different MS-DRG than a patient with only the pneumonia diagnosis. The resulting reimbursement difference can be substantial, highlighting the need for meticulous coding practices.

A comparative analysis of the two forms reveals that while Form A-8-2 may still be required for certain non-inpatient services, such as outpatient therapy or home health, its applicability to hospital Medicare cost reporting is limited. Hospitals should focus on optimizing their UB-04 submission processes, including implementing robust quality checks to minimize claim denials and delays. This may involve investing in revenue cycle management software or providing ongoing training to billing staff on the latest CMS guidelines and coding updates.

In conclusion, while Form A-8-2 may hold historical significance, its role in hospital Medicare cost reporting has been largely superseded by the UB-04 form. Hospitals must adapt to these changes by prioritizing accurate and efficient UB-04 submissions, ensuring compliance with CMS regulations, and staying abreast of evolving reimbursement methodologies. By doing so, they can maximize their Medicare reimbursements and maintain financial stability in an increasingly complex healthcare landscape. To facilitate this transition, hospitals should consider the following practical tips: review CMS's quarterly updates to the UB-04 form, conduct regular coding audits, and establish a cross-functional team to address reimbursement challenges.

CSU Hospital at Kaiser: Understanding Its Unit and Role

You may want to see also

Explore related products

![]()

Hospital Compliance Requirements

Hospitals navigating Medicare cost reporting must remain vigilant about compliance requirements, as oversight can lead to financial penalties or audits. One critical aspect involves understanding the role of Form A-8-2, historically used for reporting bad debts. While the form itself is no longer in active use, its underlying principles remain embedded in current Medicare cost reporting guidelines. Hospitals must now report bad debts directly on Worksheet B, Part III of the Medicare cost report, ensuring alignment with the Centers for Medicare & Medicaid Services (CMS) regulations. Failure to accurately document and justify bad debts can result in disallowed costs, directly impacting reimbursement.

To maintain compliance, hospitals should establish robust internal processes for identifying, tracking, and documenting bad debts. This includes verifying patient eligibility for Medicare, exhausting all reasonable collection efforts, and maintaining detailed records of these attempts. For instance, hospitals should retain documentation such as billing statements, collection agency correspondence, and patient communication logs for at least five years. Additionally, hospitals must ensure that bad debts are reported within the required timeframe, typically within 180 days of the end of the cost reporting period.

A comparative analysis of compliance strategies reveals that hospitals adopting automated systems for bad debt tracking tend to fare better in audits. These systems streamline documentation, reduce human error, and provide real-time visibility into collection efforts. For example, integrating electronic health record (EHR) systems with billing platforms can automatically flag accounts meeting bad debt criteria, ensuring timely reporting. Hospitals should also conduct periodic internal audits to identify discrepancies and address compliance gaps proactively.

Persuasively, hospitals must recognize that compliance with Medicare cost reporting requirements is not merely a regulatory obligation but a strategic imperative. Accurate reporting directly influences reimbursement rates, which are critical for financial sustainability. Hospitals that invest in compliance training for staff, leverage technology, and maintain transparent documentation practices are better positioned to navigate CMS audits successfully. For instance, dedicating resources to a compliance officer or team can provide oversight and ensure adherence to evolving regulations.

In conclusion, while Form A-8-2 is no longer applicable, its legacy underscores the importance of meticulous bad debt reporting in Medicare cost reporting. Hospitals must adapt to current CMS guidelines by implementing structured processes, leveraging technology, and fostering a culture of compliance. By doing so, they not only mitigate risks but also optimize reimbursement, ensuring long-term financial health in an increasingly complex healthcare landscape.

R. Kelly Hospitalized: What Happened?

You may want to see also

Explore related products

![]()

A-8-2 vs. New Reporting Forms

The Medicare cost reporting landscape has evolved significantly, leaving many hospitals questioning the relevance of Form A-8-2. This form, once a cornerstone of Medicare cost reporting, has been largely superseded by newer, more streamlined options.

Understanding the differences between A-8-2 and its modern counterparts is crucial for hospitals seeking efficient and compliant reporting.

The Rise of the New Guard: Streamlined Reporting

Newer Medicare cost reporting forms prioritize efficiency and data accuracy. Forms like the UB-04 and the Cost Report Worksheet (CRW) offer several advantages over A-8-2. The UB-04, for instance, is a standardized claim form used across healthcare settings, simplifying data submission and reducing the risk of errors. The CRW, a web-based platform, provides real-time validation and error checking, ensuring data integrity and expediting the review process. These modern forms are designed to integrate seamlessly with electronic health record (EHR) systems, further streamlining data collection and submission.

For example, the CRW allows hospitals to directly import cost data from their EHR, eliminating manual data entry and minimizing the potential for transcription errors.

A-8-2: A Legacy Form with Limited Applicability

While A-8-2 served its purpose in the past, its limitations are evident in today's healthcare environment. The form's paper-based format is cumbersome and prone to errors. Manual data entry increases the risk of inaccuracies, potentially leading to costly audits and reimbursement delays. Additionally, A-8-2 lacks the data validation features of newer forms, making it more susceptible to submission errors.

Transitioning to Modern Reporting: A Strategic Move

Hospitals still relying on A-8-2 should strongly consider transitioning to newer reporting forms. The benefits are clear: improved efficiency, enhanced data accuracy, and reduced administrative burden. The initial investment in training and system integration will be offset by long-term savings in time and resources.

Practical Considerations for the Transition

Transitioning from A-8-2 requires careful planning. Hospitals should:

- Assess their current reporting processes: Identify areas where A-8-2 creates inefficiencies or errors.

- Evaluate available options: Research the features and benefits of UB-04, CRW, and other modern forms to determine the best fit for their needs.

- Invest in training: Ensure staff are proficient in using the new reporting system.

- Test and validate: Conduct thorough testing to ensure accurate data submission before fully transitioning.

By embracing modern reporting forms, hospitals can streamline their Medicare cost reporting processes, improve data accuracy, and ultimately optimize their reimbursement. While A-8-2 may hold historical significance, its time has largely passed, making way for more efficient and effective reporting solutions.

Clarksville's Blanchfield Army Community Hospital: Serving Military Personnel and Families

You may want to see also

Explore related products

![]()

CMS Updates & Guidelines

The Centers for Medicare & Medicaid Services (CMS) periodically updates its guidelines to ensure accurate and efficient Medicare cost reporting by hospitals. One critical area of focus is the standardization and simplification of reporting forms. While Form A-8-2, historically used for Medicare cost reporting, has been a cornerstone for decades, recent CMS updates have shifted the landscape. Hospitals must now navigate a new set of forms and requirements, rendering Form A-8-2 largely obsolete for most reporting purposes.

CMS’s transition to the Healthcare Cost Report (HCR) system exemplifies this shift. The HCR, introduced in 2019, consolidates multiple cost reporting forms into a single, streamlined platform. This change aims to reduce administrative burden and improve data accuracy. For instance, Worksheet A-8, which previously required manual calculations for wage index adjustments, is now integrated into the HCR’s automated system. Hospitals must adapt to this digital transformation, ensuring their staff are trained to use the new interface and understand the updated data submission protocols.

Another significant update is the enhanced focus on data validation and audit compliance. CMS has tightened its scrutiny on cost reporting discrepancies, particularly in areas like bad debt and disproportionate share hospital (DSH) payments. Hospitals must now provide more detailed documentation to support their claims. For example, bad debt reporting now requires itemized lists of unpaid Medicare claims, along with proof of reasonable collection efforts. Failure to comply can result in payment adjustments or audits, making it imperative for hospitals to stay abreast of these guidelines.

Practical tips for hospitals include conducting regular internal audits to identify potential discrepancies before CMS reviews. Additionally, leveraging CMS’s Provider Reimbursement Manual (Part 2) as a reference can help clarify complex reporting requirements. Hospitals should also designate a compliance officer to monitor CMS updates, ensuring timely implementation of new rules. By proactively addressing these changes, hospitals can minimize financial risks and maintain compliance with Medicare cost reporting standards.

In conclusion, while Form A-8-2 may no longer be applicable, its legacy underscores the evolving nature of CMS guidelines. Hospitals must embrace the new HCR system, prioritize data accuracy, and stay informed about ongoing updates. Doing so not only ensures compliance but also optimizes Medicare reimbursement in an increasingly complex healthcare landscape.

Ulrich's Emotional Visit: Inside Helge's Hospital Room in Dark

You may want to see also

Frequently asked questions

No, Form A-8-2 is no longer applicable for hospital Medicare cost reporting. It has been replaced by the CMS-2552-10 form, which is the current form used for Medicare cost reporting by hospitals.

Form A-8-2 was phased out in the early 2000s. The CMS-2552-10 form was introduced as its replacement to streamline and modernize the Medicare cost reporting process.

No, hospitals cannot use Form A-8-2 for any Medicare-related reporting. All Medicare cost reporting must be done using the CMS-2552-10 form as per current CMS guidelines.

Hospitals should retain old Form A-8-2 documents for historical or audit purposes but should not use them for current Medicare cost reporting. All new reporting must be done using the CMS-2552-10 form.

There are no exceptions; Form A-8-2 is completely obsolete for Medicare cost reporting. Hospitals must use the CMS-2552-10 form for all applicable reporting requirements.