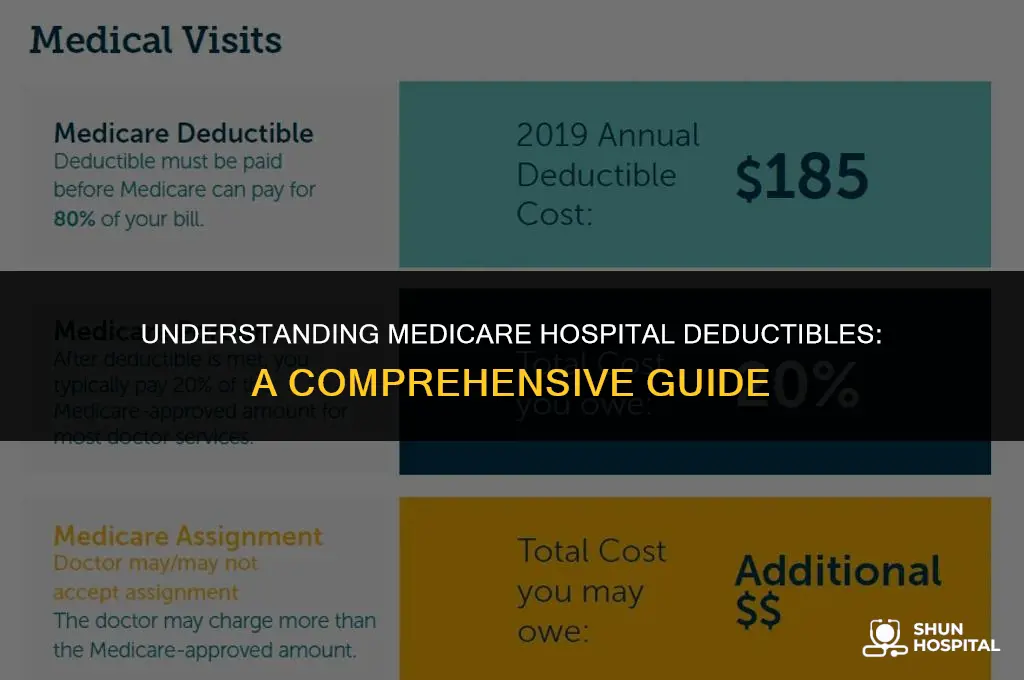

Medicare is a federal health insurance program primarily for individuals aged 65 and older, as well as for certain younger people with disabilities. The Medicare hospital deductible is a key component of the program's cost-sharing structure. This deductible is the amount a beneficiary must pay out-of-pocket for hospital services before Medicare begins to cover the costs. Understanding the Medicare hospital deductible is crucial for beneficiaries to anticipate and manage their healthcare expenses effectively.

| Characteristics | Values |

|---|---|

| Deductible Type | Hospital Deductible |

| Program | Medicare |

| Year | 2024 |

| Standard Deductible Amount | $1,600 |

| Coinsurance | 20% after deductible |

| Maximum Out-of-Pocket | $7,100 |

| Applies To | Inpatient services, Skilled Nursing Facility (SNF) care |

| Does Not Apply To | Outpatient services, Prescription drugs |

| Exceptions | No exceptions for standard deductible |

| Additional Costs | May vary based on hospital charges and length of stay |

| Coverage Period | Calendar year |

| Enrollment | Automatically enrolled when eligible for Medicare |

| Premium | Included in Medicare Part A premium |

| Provider Network | Any Medicare-approved hospital |

| Claim Filing | Filed by hospital or SNF |

| Appeal Process | Available for denied claims |

| Resources | Medicare website, 1-800-MEDICARE |

Explore related products

What You'll Learn

- Definition: The amount beneficiaries pay before Medicare starts covering hospital expenses

- Annual Limit: The maximum deductible amount changes yearly, reflecting healthcare cost adjustments

- Coverage Gaps: Beneficiaries are responsible for costs until the deductible is met, creating potential coverage gaps

- Supplemental Insurance: Medigap policies can help cover the deductible and other out-of-pocket costs

- Impact on Beneficiaries: High deductibles can lead to financial strain, influencing healthcare decisions and access

![]()

Definition: The amount beneficiaries pay before Medicare starts covering hospital expenses

The Medicare hospital deductible is a critical component of the Medicare program, specifically designed to manage the financial burden of hospital care for beneficiaries. It represents the initial amount that beneficiaries must pay out-of-pocket before Medicare begins to cover their hospital expenses. This deductible serves as a form of cost-sharing, ensuring that beneficiaries have some financial investment in their healthcare, which can help to control overall healthcare costs.

For 2023, the Medicare hospital deductible is set at $1,484. This amount can vary from year to year, adjusted for inflation and other economic factors. It's important for beneficiaries to be aware of this deductible as it can significantly impact their out-of-pocket healthcare costs. The deductible applies to each benefit period, which typically starts the day you are admitted to the hospital and ends 60 days after you are discharged.

Understanding the Medicare hospital deductible is essential for effective financial planning. Beneficiaries should consider this deductible when budgeting for potential healthcare expenses. Additionally, it's crucial to note that this deductible is separate from other Medicare costs, such as premiums and copayments. Therefore, even if a beneficiary has paid their monthly premium, they will still need to cover the deductible before Medicare benefits kick in.

To manage the hospital deductible, beneficiaries may choose to purchase a Medicare Supplement plan, also known as Medigap. These plans are offered by private insurance companies and can help cover some or all of the deductible, as well as other out-of-pocket costs associated with Medicare. Alternatively, beneficiaries may opt for a Medicare Advantage plan, which often includes hospital coverage with a lower deductible than traditional Medicare.

In conclusion, the Medicare hospital deductible is a significant aspect of the Medicare program that beneficiaries must understand to effectively manage their healthcare costs. By being aware of the deductible amount and exploring options such as Medicare Supplement or Advantage plans, beneficiaries can better prepare for and mitigate the financial impact of hospital care.

Cincinnati's Healthcare Excellence: Are Its Hospitals Among the Best?

You may want to see also

Explore related products

![]()

Annual Limit: The maximum deductible amount changes yearly, reflecting healthcare cost adjustments

The Medicare hospital deductible is subject to an annual limit, which is adjusted yearly to reflect changes in healthcare costs. This limit is crucial for beneficiaries to understand, as it directly impacts their out-of-pocket expenses for hospital care. For instance, in 2023, the Medicare Part A hospital deductible was $1,556. This amount is the maximum a beneficiary would pay for hospital services in a given year, after which Medicare covers the remaining costs.

The annual adjustment of the deductible is based on the Social Security Administration's (SSA) calculation of the Consumer Price Index for All Urban Consumers (CPI-U). This index measures the average change in prices over time for goods and services, including healthcare. By linking the deductible to the CPI-U, Medicare ensures that the deductible remains aligned with the current cost of living and healthcare expenses.

For beneficiaries, understanding the annual limit is essential for financial planning. It allows them to anticipate their potential healthcare costs and budget accordingly. Additionally, knowing the deductible limit can help beneficiaries make informed decisions about their healthcare, such as whether to seek treatment at a hospital or an outpatient facility, which may have different cost structures.

Moreover, the annual limit provides a measure of protection against catastrophic healthcare costs. By capping the deductible amount, Medicare helps to prevent beneficiaries from facing exorbitant expenses that could lead to financial hardship. This is particularly important for older adults and individuals with limited incomes, who may be more vulnerable to the financial burden of healthcare costs.

In conclusion, the annual limit on the Medicare hospital deductible is a critical component of the Medicare system. It ensures that beneficiaries are protected from excessive out-of-pocket expenses while also allowing for adjustments to reflect changes in healthcare costs. Understanding this limit is essential for beneficiaries to effectively manage their healthcare expenses and make informed decisions about their care.

Is Pink in Sydney Hospital? Unraveling the Mystery Behind the Rumor

You may want to see also

Explore related products

![]()

Coverage Gaps: Beneficiaries are responsible for costs until the deductible is met, creating potential coverage gaps

Beneficiaries are often unaware of the coverage gaps that exist within their Medicare plans, particularly when it comes to hospital deductibles. These gaps can lead to unexpected out-of-pocket expenses, which can be financially burdensome for many individuals. It's essential to understand these coverage gaps to make informed decisions about your healthcare and to plan accordingly.

One of the primary coverage gaps in Medicare is the hospital deductible. This is the amount that beneficiaries must pay out-of-pocket before their Medicare coverage kicks in. In 2023, the standard hospital deductible is $1,484. This deductible applies to each benefit period, which means that if you are hospitalized multiple times within a single benefit period, you will only need to meet the deductible once. However, if you are hospitalized in a new benefit period, you will need to meet the deductible again.

Another coverage gap that beneficiaries should be aware of is the coinsurance requirement. After meeting the hospital deductible, Medicare typically covers 80% of the remaining hospital costs. This leaves beneficiaries responsible for the remaining 20%, which can add up quickly, especially for extended hospital stays or high-cost procedures. Additionally, Medicare does not cover certain services, such as dental care, vision care, and hearing aids, which can also create coverage gaps for beneficiaries who require these services.

To mitigate these coverage gaps, beneficiaries may choose to enroll in a Medicare Supplement plan, also known as a Medigap plan. These plans are designed to fill in the gaps in Medicare coverage, including the hospital deductible and coinsurance requirements. Medigap plans are offered by private insurance companies and come in a variety of options, each with different levels of coverage and premiums. By enrolling in a Medigap plan, beneficiaries can reduce their out-of-pocket expenses and have more predictable healthcare costs.

In conclusion, understanding the coverage gaps in Medicare, particularly the hospital deductible, is crucial for beneficiaries to make informed decisions about their healthcare. By being aware of these gaps and exploring options such as Medigap plans, beneficiaries can better manage their healthcare costs and ensure that they have the coverage they need.

Writing a Compelling Hospital Financial Assistance Letter: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Supplemental Insurance: Medigap policies can help cover the deductible and other out-of-pocket costs

Medicare's hospital deductible can be a significant financial burden for many beneficiaries. In 2023, the standard deductible is $1,484, which must be paid out-of-pocket before Medicare coverage kicks in. This can be particularly challenging for those with limited savings or fixed incomes. Fortunately, there are supplemental insurance options available that can help cover this deductible and other out-of-pocket costs.

Medigap policies, also known as Medicare Supplement Insurance, are designed to fill the gaps in Medicare coverage. These policies are offered by private insurance companies and can help pay for expenses that Medicare doesn't cover, including deductibles, copayments, and coinsurance. Medigap policies can be particularly beneficial for those who have high medical expenses or who want to avoid the financial uncertainty of unexpected healthcare costs.

When considering a Medigap policy, it's important to understand the different plan options available. There are 10 standardized Medigap plans, each with its own set of benefits and premiums. Plan F is the most comprehensive plan, covering the Medicare deductible, copayments, coinsurance, and even the Part B deductible. However, it's also the most expensive plan. Other plans, such as Plan G and Plan N, offer similar benefits but with lower premiums.

To determine which Medigap plan is right for you, it's essential to evaluate your healthcare needs and budget. Consider factors such as your age, health status, and expected medical expenses. You may also want to consult with a licensed insurance agent who can help you compare plans and find the best option for your specific situation.

In conclusion, supplemental insurance options like Medigap policies can provide valuable financial protection for Medicare beneficiaries. By understanding the different plan options and carefully evaluating your healthcare needs, you can find a policy that helps cover the Medicare hospital deductible and other out-of-pocket costs, giving you peace of mind and financial security.

Highland Hospital Denture Services: What You Need to Know

You may want to see also

Explore related products

![]()

Impact on Beneficiaries: High deductibles can lead to financial strain, influencing healthcare decisions and access

High deductibles under Medicare can significantly impact beneficiaries, leading to financial strain and influencing their healthcare decisions and access. This is particularly true for those with limited incomes or those who require frequent medical care. When faced with high out-of-pocket costs, beneficiaries may be forced to make difficult choices about their healthcare, potentially delaying or forgoing necessary treatments.

For instance, a beneficiary with a high deductible may decide to postpone a medical procedure or skip a recommended test due to the cost, which can lead to worsening health conditions and more expensive treatments down the line. Additionally, high deductibles can create a barrier to accessing preventive care, which is crucial for maintaining good health and preventing more serious illnesses.

The financial strain caused by high deductibles can also lead to stress and anxiety for beneficiaries, affecting their overall well-being. This is especially concerning for older adults who may be living on fixed incomes and have limited resources to cover unexpected medical expenses. In some cases, beneficiaries may even have to dip into their savings or retirement funds to cover their deductibles, which can have long-term financial consequences.

Furthermore, high deductibles can exacerbate health disparities, as those with lower incomes or minority populations may be more likely to face financial barriers to accessing healthcare. This can lead to a widening gap in health outcomes between different demographic groups, which is a significant concern for public health.

In conclusion, the impact of high deductibles on Medicare beneficiaries cannot be overstated. It is essential for policymakers and healthcare providers to consider the financial burden that high deductibles place on beneficiaries and to explore ways to mitigate this strain, such as through policy changes or innovative healthcare delivery models. By doing so, we can help ensure that all beneficiaries have access to the healthcare they need without facing undue financial hardship.

GI Clinic Location at Ford Hospital Detroit: Floor Guide

You may want to see also

Frequently asked questions

The Medicare hospital deductible is the amount you must pay out-of-pocket before Medicare starts to cover your hospital expenses. For 2023, the deductible is $1,484 per benefit period.

You have to pay the Medicare hospital deductible once per benefit period. A benefit period starts the day you are admitted to the hospital and ends when you have been out of the hospital for 60 days in a row.

After you pay the deductible, Medicare covers most hospital expenses, including room and board, nursing care, and medications. However, you may still be responsible for coinsurance and copayments for certain services.

Yes, you can buy a Medicare supplement plan, also known as Medigap, to cover the hospital deductible. Medigap plans are sold by private insurance companies and can help fill in the gaps in Medicare coverage, including deductibles, coinsurance, and copayments.