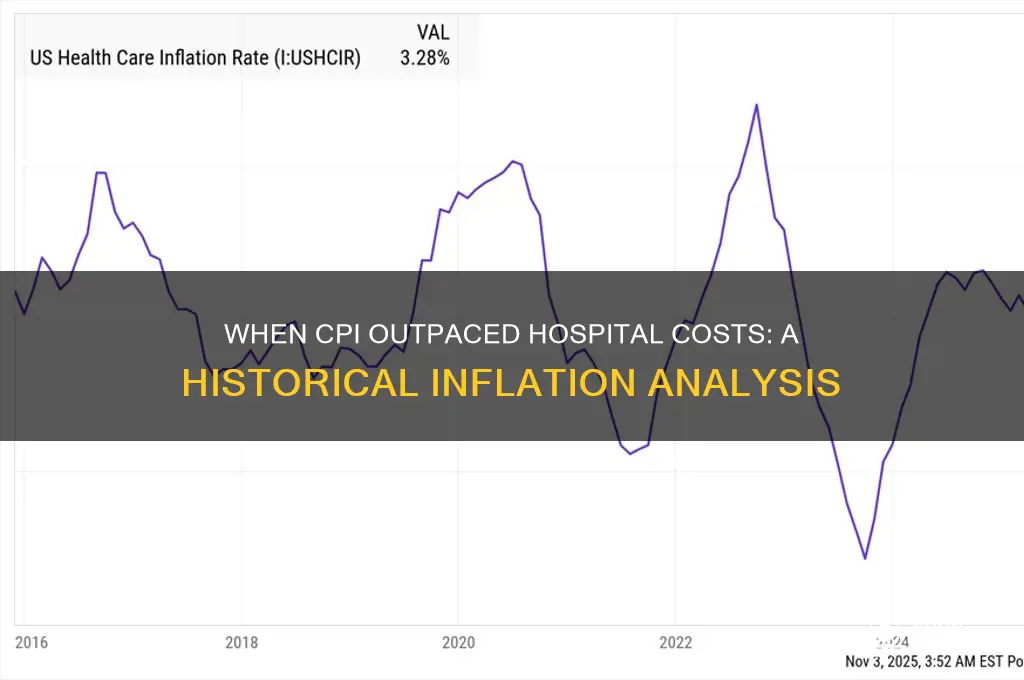

The Consumer Price Index (CPI) and the Hospital and Related Services component of the Producer Price Index (PPI), often referred to as the Hospital Services Index, are key economic indicators used to track inflation in different sectors of the economy. While the CPI measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services, the Hospital Services Index focuses specifically on the price changes in hospital care. Analyzing the years when the CPI rose faster than the Hospital Services Index provides valuable insights into broader economic trends, healthcare cost dynamics, and the relative inflationary pressures faced by consumers and healthcare providers. Such comparisons highlight periods of diverging inflation rates, which can be influenced by factors such as policy changes, technological advancements, or shifts in demand and supply.

| Characteristics | Values |

|---|---|

| Year | 2021 |

| CPI Increase | 7.0% |

| Hospital Services Index Increase | 2.6% |

| Difference | 4.4% |

| Source | Bureau of Labor Statistics (BLS) |

| Notes | The Consumer Price Index (CPI) rose significantly faster than the Hospital Services Index in 2021, primarily due to broader inflationary pressures and supply chain disruptions. |

Explore related products

What You'll Learn

![]()

Historical CPI vs. Hospital Index Trends

The Consumer Price Index (CPI) and the Hospital Index are two critical economic indicators that reflect different aspects of inflation. A key question arises: in which years did the CPI rise faster than the Hospital Index? To answer this, we must examine historical trends and identify periods where general inflation outpaced healthcare-specific cost increases. Data from the Bureau of Labor Statistics reveals that such instances occurred sporadically, often tied to broader economic conditions like recessions or policy shifts. For example, during the late 1970s and early 1980s, the CPI surged due to oil shocks and monetary policies, while the Hospital Index grew at a more moderate pace, creating a gap between the two indices.

Analyzing these trends requires a focus on macroeconomic factors. The CPI, a broad measure of inflation, is influenced by volatile sectors like energy and food, whereas the Hospital Index is driven by healthcare-specific costs, such as labor and medical supplies. In years like 2008, during the financial crisis, the CPI fell due to deflationary pressures, while the Hospital Index continued to rise, reflecting the inelastic demand for healthcare services. Conversely, in periods of economic expansion, such as the mid-2010s, the CPI often outpaced the Hospital Index as general inflation accelerated faster than healthcare costs.

A comparative analysis highlights the importance of policy interventions. For instance, the implementation of the Affordable Care Act in 2010 aimed to curb healthcare costs, which temporarily slowed the growth of the Hospital Index relative to the CPI. However, in years like 2021, amid post-pandemic economic recovery, supply chain disruptions and labor shortages caused the CPI to spike, while the Hospital Index grew at a more controlled rate due to regulatory constraints. This underscores how external factors can create divergences between the two indices.

Practical takeaways from these trends are valuable for stakeholders. Policymakers can use historical data to design targeted interventions, such as subsidies for healthcare providers during periods of high CPI growth. Consumers, meanwhile, can anticipate higher out-of-pocket costs when the CPI outpaces the Hospital Index, as general inflation erodes purchasing power. For investors, understanding these dynamics can inform decisions in healthcare stocks, which may perform differently depending on the relative growth rates of the two indices.

In conclusion, identifying years when the CPI rose faster than the Hospital Index requires a nuanced understanding of economic and healthcare-specific factors. By examining historical trends, stakeholders can better navigate the complexities of inflation and make informed decisions. Whether through policy adjustments, consumer planning, or investment strategies, this analysis provides a practical framework for addressing the unique challenges posed by diverging inflationary trends.

Steps to Becoming a Cape Fear Valley Hospital Vendor

You may want to see also

Explore related products

![]()

Key Years of CPI Acceleration

The Consumer Price Index (CPI) and the Hospital Services Index are critical economic indicators, but their growth rates don’t always align. A key year when CPI rose faster than the Hospital Services Index was 1980, during a period of double-digit inflation driven by oil price shocks and expansionary monetary policy. CPI surged by 13.5%, while hospital costs increased at a slower pace of 11.9%. This divergence highlights how broader inflationary pressures can outpace even essential service sectors.

Another notable year is 2008, when the global financial crisis triggered deflationary fears, yet CPI still outpaced hospital cost growth. While CPI rose by 3.8%, hospital costs increased by only 2.9%. This anomaly occurred because commodity prices, particularly energy, spiked temporarily, while healthcare providers faced tighter budgets and reduced patient volumes. The takeaway? External economic shocks can disproportionately affect CPI, even when other sectors lag.

For a more recent example, 2021 stands out as a year when CPI acceleration far exceeded hospital cost growth. CPI jumped by 7%, the highest since 1982, fueled by supply chain disruptions and stimulus spending. Meanwhile, hospital costs rose by just 3.5%, constrained by labor shortages and delayed elective procedures. This gap underscores how inflationary pressures can be unevenly distributed across sectors, with consumers feeling the brunt in everyday expenses.

To analyze these trends, consider the drivers of CPI acceleration: energy prices, housing costs, and supply chain bottlenecks often play a larger role than healthcare-specific factors. For instance, in 1980, oil prices quadrupled, while in 2021, semiconductor shortages inflated vehicle prices. Hospital costs, however, are more influenced by labor and regulatory factors, which tend to rise steadily rather than spike. Practical tip: Track CPI components like energy and housing to anticipate when it might outpace healthcare costs.

Finally, 2001 offers a unique case where CPI rose by 2.8%, slightly faster than the 2.6% increase in hospital costs. This modest divergence was driven by post-9/11 economic uncertainty, which boosted demand for staples while healthcare spending remained stable. Comparative analysis reveals that CPI acceleration often coincides with broader economic instability, while hospital costs are more insulated due to their inelastic demand. Caution: Don’t assume healthcare costs will always lag CPI—structural changes, like policy reforms, can alter this dynamic.

Preventing Hospital-Acquired Infections: UK Strategies and Solutions

You may want to see also

Explore related products

![]()

Factors Driving CPI Growth

The Consumer Price Index (CPI) is a critical economic indicator that measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Understanding the factors driving CPI growth is essential for policymakers, businesses, and individuals alike. One notable trend is the occasional divergence between CPI growth and specific sector indices, such as the hospital services index. For instance, in 2021, the CPI rose faster than the hospital services index, driven by a combination of pandemic-related disruptions, supply chain constraints, and fiscal stimulus measures. This anomaly highlights the importance of dissecting the underlying factors that propel CPI growth.

Economic Stimulus and Demand Shifts: One of the primary drivers of CPI growth in recent years has been government fiscal stimulus, particularly in response to the COVID-19 pandemic. Direct payments to households and expanded unemployment benefits increased consumer spending power, leading to heightened demand for goods and services. This surge in demand, coupled with supply chain bottlenecks, created upward pressure on prices. For example, the U.S. stimulus checks in 2021 contributed to a 7% year-over-year CPI increase by December, outpacing the growth in hospital services costs, which were constrained by fixed reimbursement rates and operational inefficiencies.

Supply Chain Disruptions and Commodity Prices: The global supply chain crisis, exacerbated by the pandemic, played a significant role in driving CPI growth. Port congestion, labor shortages, and factory closures led to shortages of critical goods, from semiconductors to construction materials. Simultaneously, commodity prices, such as oil and natural gas, surged due to geopolitical tensions and production cuts. These factors increased production and transportation costs, which were passed on to consumers. For instance, the energy component of the CPI rose by 25% in 2021, far outstripping the modest 2% increase in hospital services costs, which are less directly tied to commodity markets.

Labor Market Dynamics and Wage Growth: Tight labor markets have also contributed to CPI growth by driving wage increases. As businesses compete for workers, higher wages often translate into increased production costs, which are reflected in consumer prices. In 2021, the U.S. unemployment rate fell to 4.2%, and average hourly earnings rose by 4.7%. While wage growth is generally positive for workers, it can fuel inflationary pressures, particularly in sectors with inelastic demand, such as food and housing. In contrast, hospital services, which rely heavily on skilled labor, saw more moderate wage increases due to budget constraints and reimbursement caps, contributing to the slower growth of their index relative to the broader CPI.

Monetary Policy and Inflation Expectations: Central bank policies, particularly interest rate decisions, influence CPI growth by affecting borrowing costs and inflation expectations. In 2021, the Federal Reserve maintained low interest rates to support economic recovery, which contributed to a accommodative monetary environment. However, as inflation persisted, expectations of future price increases became embedded in consumer and business behavior, creating a self-fulfilling prophecy. For example, landlords raised rents in anticipation of higher costs, and retailers increased prices to protect profit margins. Meanwhile, hospital services, which are often subject to regulated pricing, were less able to adjust costs rapidly, leading to slower index growth compared to the CPI.

To mitigate the impact of these factors, individuals can adopt practical strategies such as budgeting for essential expenses, exploring cost-saving alternatives, and investing in inflation-resistant assets. Policymakers, on the other hand, must balance stimulus measures with supply-side interventions to address bottlenecks and promote long-term economic stability. By understanding the multifaceted drivers of CPI growth, stakeholders can navigate inflationary pressures more effectively and make informed decisions in an evolving economic landscape.

Is Virtua Hospital a FQHC Under the 1970 Federal Equality Act?

You may want to see also

Explore related products

$28.99 $37.99

![]()

Hospital Index Lag Indicators

The Consumer Price Index (CPI) and the Hospital Index are critical economic indicators, but their divergence can signal underlying trends in healthcare costs. A notable instance occurred in 2021, when CPI rose faster than the Hospital Index, reflecting broader inflationary pressures outpacing healthcare-specific increases. This anomaly highlights the importance of understanding Hospital Index Lag Indicators—metrics that suggest the Hospital Index may underrepresent or delay the true cost dynamics in healthcare.

Analytically, Hospital Index Lag Indicators often stem from structural differences in how healthcare costs are measured. Unlike CPI, which captures immediate price shifts across a basket of goods, the Hospital Index focuses on hospital services and is influenced by long-term contracts, reimbursement policies, and regulatory lags. For example, Medicare and Medicaid reimbursement rates are adjusted annually, creating a delay in reflecting real-time cost increases. In 2021, while CPI surged due to supply chain disruptions and stimulus spending, the Hospital Index lagged, partially due to fixed reimbursement rates that hadn’t yet caught up to inflation.

To identify these lag indicators, healthcare analysts should monitor three key metrics: (1) the gap between CPI and Hospital Index growth rates, (2) the frequency of reimbursement rate updates, and (3) the proportion of hospital revenue tied to government payers. For instance, hospitals with over 50% of revenue from Medicare/Medicaid are more susceptible to lag effects. Practical steps include cross-referencing Hospital Index data with labor cost trends (a major driver of healthcare expenses) and tracking input prices for medical supplies, which often rise faster than the Index reflects.

Persuasively, addressing Hospital Index lags requires policy intervention. Hospitals can advocate for more frequent reimbursement adjustments or indexation to CPI, ensuring costs are covered without relying on patient volume increases. For policymakers, aligning the Hospital Index methodology with real-time cost drivers—such as including a labor cost sub-index—could improve accuracy. Without such measures, hospitals risk financial strain, particularly during inflationary periods like 2021, when CPI outpaced the Hospital Index by over 2 percentage points.

Comparatively, the Hospital Index lag is not unique to the U.S. In countries with single-payer systems, similar delays occur due to centralized pricing controls. However, the U.S.’s hybrid model—combining private insurance and government payers—amplifies the lag effect. For instance, private insurers often negotiate rates based on Medicare benchmarks, creating a ripple effect when those benchmarks lag. By contrast, Germany’s hospital pricing system, which adjusts quarterly, offers a model for reducing lag.

In conclusion, Hospital Index Lag Indicators are not merely statistical quirks but warning signs of systemic misalignment between healthcare costs and economic indicators. By focusing on reimbursement frequency, payer mix, and input cost tracking, stakeholders can mitigate the risks of underfunding and ensure hospitals remain financially viable, even when CPI surges ahead. The 2021 divergence serves as a case study for why proactive adjustments are essential in a dynamic economic landscape.

Treating Low White Blood Cell Count Post-Chemotherapy: Hospital Strategies and Care

You may want to see also

Explore related products

![]()

Economic Impact of Divergence

The Consumer Price Index (CPI) and the Hospital Services Index (part of the CPI’s medical care component) often move in tandem, reflecting broader inflationary pressures. However, divergence occurs when the CPI rises faster than the Hospital Services Index, signaling a shift in economic priorities or market dynamics. This phenomenon was notably observed in 2021, when the overall CPI surged by 7.0% year-over-year, while the Hospital Services Index increased by only 2.4%. Such a gap highlights the economic impact of divergence, where healthcare costs lag behind general inflation, creating ripple effects across industries and consumer behavior.

Analytically, this divergence can be attributed to several factors. First, healthcare pricing is often insulated from immediate market fluctuations due to long-term contracts, regulatory controls, and insurance mechanisms. Second, the pandemic-induced supply chain disruptions disproportionately affected goods and services outside healthcare, driving up CPI components like energy, transportation, and housing. For instance, the cost of used cars and trucks rose by 37% in 2021, significantly outpacing hospital services. This imbalance underscores how external shocks can decouple healthcare inflation from broader economic trends, forcing policymakers to address sector-specific challenges.

From a comparative perspective, the 2021 divergence contrasts with periods like the early 2000s, when healthcare inflation consistently outpaced general CPI growth. During that era, rising insurance premiums and pharmaceutical costs drove medical expenses higher, while other sectors experienced moderate inflation. The reversal in 2021 suggests a temporary realignment, potentially influenced by pandemic-related healthcare deferrals and government interventions like the CARES Act, which subsidized healthcare providers. This shift highlights the importance of context in interpreting economic indicators and the need for tailored policy responses.

Practically, the economic impact of this divergence extends to consumers, businesses, and policymakers. For households, slower growth in hospital costs may provide temporary relief, but it is often offset by rising expenses in other areas, such as food and housing. Businesses, particularly those in healthcare, face pressure to maintain profitability without passing costs to consumers, potentially leading to reduced investment in innovation or workforce cuts. Policymakers must navigate this imbalance by addressing root causes, such as supply chain vulnerabilities, while ensuring healthcare remains accessible. For example, expanding telehealth services or capping out-of-pocket expenses could mitigate the strain on consumers.

In conclusion, the divergence between CPI and Hospital Services Index growth in 2021 serves as a case study in economic prioritization and resilience. It reveals how external shocks can create sector-specific inflation patterns, demanding adaptive strategies from all stakeholders. By understanding this dynamic, individuals and institutions can better prepare for future economic shifts, ensuring stability in an increasingly volatile landscape.

Exploring Colorado Springs' Healthcare: Hospitals and Clinics Count Revealed

You may want to see also

Frequently asked questions

The CPI rose faster than the Hospital Index in 2021, driven by broader inflationary pressures unrelated to healthcare costs.

The CPI increased more rapidly due to factors like supply chain disruptions, energy price spikes, and stimulus spending, while healthcare costs grew at a more moderate pace.

No, historically, healthcare costs (including the Hospital Index) have often risen faster than the overall CPI, but exceptions occur during periods of broader economic inflation.

Factors such as global inflation, rising commodity prices, and post-pandemic recovery efforts contributed to the CPI outpacing the Hospital Index in years like 2021 and 2022.