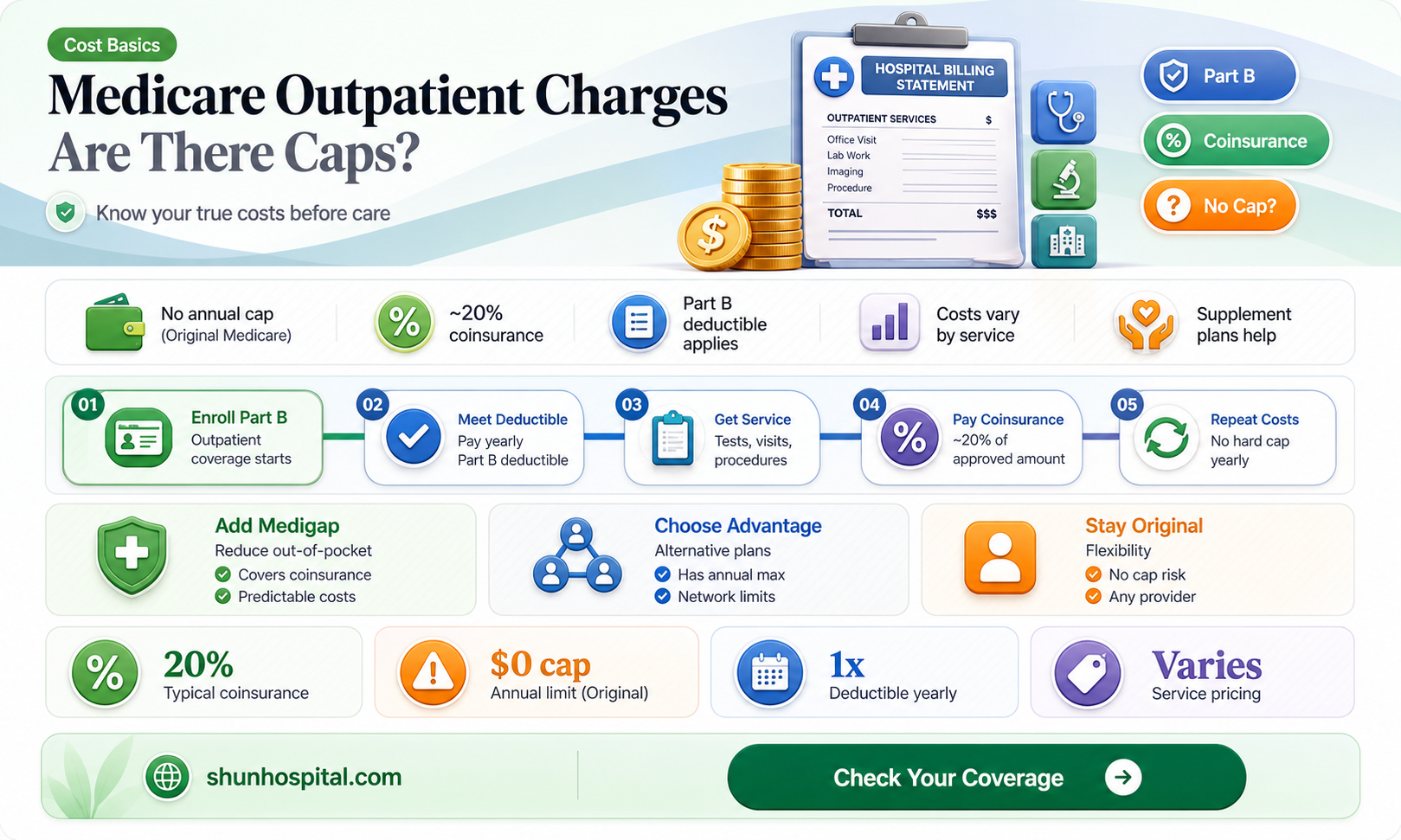

Medicare, the federal health insurance program for individuals aged 65 and older, as well as certain younger people with disabilities, plays a crucial role in covering healthcare costs. However, one common question among beneficiaries is whether charges for outpatient hospital services are capped by Medicare. Outpatient services, which include procedures, tests, and treatments that do not require an overnight hospital stay, are covered under Medicare Part B. While Medicare does set limits on how much it will pay for these services, it does not cap the total amount beneficiaries may be charged. Instead, Medicare typically covers 80% of the Medicare-approved amount for outpatient services after the annual deductible is met, leaving beneficiaries responsible for the remaining 20% coinsurance. Additionally, providers can charge more than the Medicare-approved amount, a practice known as balance billing, which can result in higher out-of-pocket costs for patients. Understanding these nuances is essential for Medicare beneficiaries to navigate their healthcare expenses effectively.

| Characteristics | Values |

|---|---|

| Medicare Outpatient Payment System | Medicare pays for outpatient hospital services using the Outpatient Prospective Payment System (OPPS), which sets specific payment rates for services. |

| Payment Caps | Medicare does not impose a specific dollar cap on total outpatient charges. However, payments are capped per service based on the OPPS fee schedule. |

| Annual Out-of-Pocket Limit | As of 2023, there is no annual out-of-pocket maximum for Medicare Part B (outpatient services). Beneficiaries are responsible for 20% of the Medicare-approved amount after meeting the Part B deductible. |

| Part B Deductible | For 2023, the Part B deductible is $226. Beneficiaries pay this amount before Medicare starts covering its share of outpatient services. |

| Coinsurance | Beneficiaries typically pay 20% of the Medicare-approved amount for most outpatient services after the deductible is met. |

| Medicare Advantage Plans | Some Medicare Advantage plans may offer out-of-pocket maximums for outpatient services, but these vary by plan and are not a standard Medicare feature. |

| High-Cost Services | Certain high-cost services, like chemotherapy or dialysis, may have specific payment limits or bundled payments under the OPPS. |

| Provider Billing Limits | Providers cannot charge more than 115% of the Medicare-approved amount for non-participating providers, but this does not cap total beneficiary costs. |

| Financial Assistance | Programs like Medicare Savings Programs or Extra Help may reduce costs for low-income beneficiaries but do not cap charges directly. |

| Updates to OPPS | CMS updates the OPPS annually, which may adjust payment rates but does not introduce a cap on total outpatient charges. |

Explore related products

What You'll Learn

![]()

Medicare Part B Coverage Limits

Medicare Part B plays a crucial role in covering outpatient hospital services, but it’s important to understand that it does not cap charges in the same way some might expect. Instead, Medicare Part B operates on a fee schedule and covers a portion of the Medicare-approved amount for services, typically 80% after the beneficiary meets their annual deductible. This means beneficiaries are responsible for the remaining 20% coinsurance, which is not capped. For outpatient hospital services, this can include emergency room visits, diagnostic tests, and certain medical procedures performed without an overnight stay. While Medicare Part B helps manage costs, it does not impose a maximum out-of-pocket limit for these services, leaving beneficiaries potentially exposed to higher expenses depending on the frequency and complexity of care.

One key aspect of Medicare Part B coverage limits is the concept of the Medicare-approved amount. Hospitals and providers are required to accept this amount as full payment for services, but they can only charge beneficiaries up to the remaining 20% coinsurance. However, if a provider does not accept Medicare assignment, they may charge up to 15% above the Medicare-approved amount, a practice known as "excess charging." This can further increase out-of-pocket costs for beneficiaries, as these additional charges are not covered by Medicare Part B. Understanding these nuances is essential for beneficiaries to anticipate potential expenses and plan accordingly.

Another important consideration is the absence of an annual out-of-pocket maximum for Medicare Part B. Unlike Medicare Advantage plans, which often include out-of-pocket caps, Original Medicare (Part A and Part B) does not provide such protection. This means that beneficiaries with frequent or high-cost outpatient services may face significant financial liability, especially if they require multiple procedures or treatments throughout the year. To mitigate this risk, many beneficiaries opt for supplemental coverage, such as Medigap plans, which can help cover the 20% coinsurance and other cost-sharing responsibilities.

It’s also worth noting that certain outpatient services may have specific coverage limitations under Medicare Part B. For example, some preventive services, like screenings and vaccinations, are fully covered without cost-sharing, but other services, such as physical therapy or durable medical equipment, may have utilization limits or require prior authorization. Beneficiaries should review their Medicare coverage documents or consult with their healthcare provider to understand which services are covered and under what conditions. This proactive approach can help avoid unexpected charges and ensure that necessary care is received within the scope of Medicare Part B benefits.

In summary, while Medicare Part B provides essential coverage for outpatient hospital services, it does not cap charges in a way that protects beneficiaries from unlimited out-of-pocket expenses. The program covers 80% of the Medicare-approved amount, leaving beneficiaries responsible for the remaining 20% coinsurance, which can add up quickly without an annual maximum. Excess charges from non-participating providers and specific service limitations further complicate cost management. Beneficiaries are encouraged to explore supplemental coverage options and stay informed about their benefits to navigate these limitations effectively and minimize financial strain.

Visiting Family in the Hospital: Rules, Restrictions, and What You Need to Know

You may want to see also

Explore related products

![Unisex Polypropylene Bouffant Caps [100 | 1000 | WHITE | BLUE | 21" | 24" | 28"]](https://m.media-amazon.com/images/I/71X4ik0aW2L._AC_UL320_.jpg)

![]()

Outpatient Service Cost Thresholds

Medicare, the federal health insurance program for individuals aged 65 and older, as well as certain younger people with disabilities, does impose limits on the amount that beneficiaries pay for outpatient hospital services. These limits, often referred to as Outpatient Service Cost Thresholds, are designed to protect beneficiaries from excessively high out-of-pocket expenses while ensuring access to necessary medical care. Understanding these thresholds is crucial for Medicare beneficiaries to navigate their healthcare costs effectively.

One of the key mechanisms Medicare uses to cap outpatient costs is the Part B deductible and coinsurance. In 2023, the Part B deductible is $226, which beneficiaries must pay before Medicare coverage begins. After meeting the deductible, beneficiaries typically pay 20% of the Medicare-approved amount for most outpatient services. However, it’s important to note that Medicare-approved amounts are often lower than the hospital’s billed charges, as Medicare sets specific reimbursement rates for services. This means that while there isn’t a direct cap on the hospital’s charges, the beneficiary’s out-of-pocket costs are limited based on the Medicare-approved amount.

Another critical aspect of outpatient cost thresholds is the Outpatient Prospective Payment System (OPPS), which Medicare uses to reimburse hospitals for outpatient services. Under OPPS, hospitals are paid a predetermined amount for each service based on its classification into Ambulatory Payment Categories (APCs). This system helps standardize costs and prevents hospitals from charging exorbitant fees for common outpatient procedures. However, beneficiaries should be aware that certain services, such as chemotherapy or advanced imaging, may have higher cost-sharing requirements, even within the OPPS framework.

For beneficiaries with Medigap (Medicare Supplement Insurance), additional protection against outpatient service costs is available. Medigap plans can cover the 20% coinsurance and other out-of-pocket expenses not covered by Original Medicare. While Medigap itself doesn’t cap hospital charges, it significantly reduces the financial burden on beneficiaries by covering a portion of their cost-sharing responsibilities. It’s essential for beneficiaries to review their Medigap coverage to understand how it interacts with Medicare’s outpatient cost thresholds.

Lastly, beneficiaries enrolled in Medicare Advantage (Part C) plans may experience different outpatient service cost thresholds. These plans, offered by private insurers, often have their own out-of-pocket maximums, which can provide additional financial protection beyond what Original Medicare offers. However, the specific thresholds and coverage details vary by plan, so beneficiaries should carefully review their plan’s benefits and limitations. In summary, while Medicare does not directly cap hospital charges for outpatient services, it employs various mechanisms to limit beneficiary out-of-pocket costs, ensuring that healthcare remains accessible and affordable.

Does VCA Weymouth Animal Hospital Employ an On-Staff Allergist?

You may want to see also

Explore related products

$13.58 $14.99

![]()

Annual Out-of-Pocket Maximums

Medicare, the federal health insurance program for individuals aged 65 and older and certain younger people with disabilities, includes provisions to protect beneficiaries from excessive out-of-pocket expenses. One such protection is the Annual Out-of-Pocket Maximum, which caps the amount beneficiaries must pay for covered services within a given year. However, it’s important to note that traditional Medicare (Part A and Part B) does not have an annual out-of-pocket maximum for outpatient hospital services or other covered care. This means that without additional coverage, beneficiaries could face unlimited out-of-pocket costs for deductibles, coinsurance, and copayments.

For outpatient hospital services under Medicare Part B, beneficiaries are responsible for 20% of the Medicare-approved amount after meeting the annual deductible. Since there is no cap on these expenses, costs can accumulate quickly, especially for individuals requiring frequent or high-cost outpatient care. This lack of an out-of-pocket maximum in traditional Medicare is a significant consideration for beneficiaries, as it can lead to financial strain in the event of serious illness or injury. To mitigate this risk, many beneficiaries opt for supplemental coverage, such as Medigap plans, which can help cover some of these out-of-pocket costs.

In contrast, Medicare Advantage (Part C) plans are required by law to include an annual out-of-pocket maximum for all covered services, including outpatient care. For 2023, the maximum out-of-pocket limit for in-network services is $8,300, though many plans set their caps lower. Once beneficiaries reach this limit, the plan covers all additional costs for the remainder of the year. This feature makes Medicare Advantage an attractive option for those seeking predictable and limited out-of-pocket expenses. However, it’s essential to review each plan’s specifics, as out-of-network services may not count toward the out-of-pocket maximum.

For beneficiaries enrolled in traditional Medicare, understanding the absence of an annual out-of-pocket maximum is crucial for financial planning. Without a cap, expenses for outpatient hospital services, doctor visits, and other Part B-covered care can add up significantly. To address this gap, beneficiaries may consider purchasing a Medigap policy, which can cover deductibles, coinsurance, and copayments. While Medigap plans themselves do not have out-of-pocket maximums, they can substantially reduce overall costs by covering many of the expenses that traditional Medicare does not.

In summary, while traditional Medicare does not cap charges for outpatient hospital services or other covered care, Medicare Advantage plans offer an annual out-of-pocket maximum, providing financial predictability. Beneficiaries on traditional Medicare can explore supplemental coverage options like Medigap to manage potential high costs. Understanding these differences is essential for making informed decisions about healthcare coverage and ensuring financial protection against unexpected medical expenses.

Exploring the Truth: Crips Presence Near Southside Hospital Cemetery

You may want to see also

Explore related products

$9.99

![]()

Medicare Advantage Plan Caps

Medicare Advantage Plans, also known as Medicare Part C, are an alternative to Original Medicare (Part A and Part B) offered by private insurance companies approved by Medicare. These plans often include additional benefits such as vision, dental, and prescription drug coverage, but they also come with specific rules regarding costs, including caps on certain services. One common question is whether charges for outpatient hospital services are capped under Medicare Advantage Plans. The answer is yes, but the specifics depend on the plan’s structure and the beneficiary’s utilization of services.

Medicare Advantage Plans typically use a network of healthcare providers and may require prior authorization for certain outpatient services. These plans are required by law to cover at least the same benefits as Original Medicare, but they can impose different cost-sharing mechanisms, such as copayments, coinsurance, or deductibles. Importantly, Medicare Advantage Plans have an annual out-of-pocket maximum, which caps the total amount a beneficiary pays for covered services, including outpatient hospital services, in a given year. This out-of-pocket maximum varies by plan but provides a financial safeguard for beneficiaries.

Outpatient hospital services, such as emergency room visits, diagnostic tests, and same-day surgeries, are covered under Medicare Advantage Plans. However, the cost-sharing for these services can differ significantly from one plan to another. Some plans may have lower copayments or coinsurance for in-network providers, while others might offer more comprehensive coverage with higher premiums. Beneficiaries should carefully review their plan’s Summary of Benefits to understand how outpatient services are covered and what their potential out-of-pocket costs might be.

It’s important to note that while Medicare Advantage Plans cap out-of-pocket expenses, these limits do not apply to services not covered by the plan or to care received outside the plan’s network (unless it’s an emergency). Additionally, the out-of-pocket maximum does not include premiums, which are separate costs. Beneficiaries should also be aware that some plans may have separate caps or limits for specific services, such as physical therapy or durable medical equipment, which could affect their overall costs.

In summary, Medicare Advantage Plans do cap charges for outpatient hospital services through their annual out-of-pocket maximums, providing beneficiaries with financial protection. However, the specifics of coverage and cost-sharing vary widely among plans, making it essential for individuals to carefully evaluate their options. By understanding their plan’s structure and limitations, beneficiaries can make informed decisions about their healthcare and manage their expenses effectively. Always consult the plan’s documentation or contact the insurance provider directly for detailed information on coverage and caps.

When Urgent Care Isn't Enough: Recognizing Signs for Hospital Referral

You may want to see also

Explore related products

![Unisex Polypropylene Bouffant Caps [100 | 1000 | WHITE | BLUE | 21" | 24" | 28"]](https://m.media-amazon.com/images/I/71NgVhF9bIL._AC_UL320_.jpg)

![]()

Exclusions from Outpatient Charge Limits

While Medicare does impose limits on certain outpatient hospital service charges through the Outpatient Prospective Payment System (OPPS), not all services fall under these caps. Understanding these exclusions is crucial for both healthcare providers and patients to navigate billing accurately.

Here’s a breakdown of key exclusions from Medicare's outpatient charge limits:

- Services Paid Under Other Payment Systems: Medicare utilizes various payment methodologies for different service types. Services reimbursed through systems like the Physician Fee Schedule (PFS), the Ambulatory Surgical Center (ASC) payment system, or the End-Stage Renal Disease (ESRD) Prospective Payment System are excluded from OPPS charge limits. For instance, physician consultations, certain surgical procedures performed in ASCs, and dialysis treatments fall outside the scope of OPPS and have their own distinct payment structures.

- Non-Covered Services: Medicare only covers medically necessary services. Procedures deemed experimental, cosmetic, or not meeting Medicare's coverage criteria are excluded from OPPS and won't be subject to its charge limits. Patients receiving such services are typically responsible for the full cost.

- Services Furnished by Excluded Providers: Medicare excludes certain types of providers from participating in the OPPS. Services rendered by these providers, even if they are outpatient services, are not subject to OPPS charge limits. Examples include services provided by non-participating hospitals or providers who have opted out of Medicare.

- Services Billed Under a Different APC: The OPPS categorizes outpatient services into Ambulatory Payment Classifications (APCs). Each APC has its own payment rate. Services that fall into a different APC than the one initially assigned may not be subject to the same charge limits. This can occur due to coding errors, changes in service complexity, or other factors.

- Services with Pass-Through Status: Medicare occasionally grants "pass-through" status to new technologies or drugs. This means the cost of these items is reimbursed separately from the APC payment, allowing for higher charges beyond the standard OPPS limits.

Understanding these exclusions is essential for accurate billing and avoiding potential payment denials or patient confusion. Both healthcare providers and patients should carefully review Medicare coverage policies and consult with billing specialists when dealing with outpatient services that may fall outside the standard OPPS charge limits.

Adopting EHR Systems: Hospital Count and Benefits

You may want to see also

Frequently asked questions

Yes, Medicare caps charges for outpatient hospital services through the Outpatient Prospective Payment System (OPPS), which sets fixed rates for specific services based on Ambulatory Payment Classifications (APCs).

No, while Medicare covers many outpatient services, beneficiaries are typically responsible for deductibles, coinsurance (usually 20% of the Medicare-approved amount), and any charges above the Medicare-approved amount if the provider does not accept assignment.

Hospitals that accept Medicare assignment cannot charge more than the Medicare-approved amount. However, non-participating providers may charge up to 115% of the Medicare rate, leaving beneficiaries responsible for the excess balance.