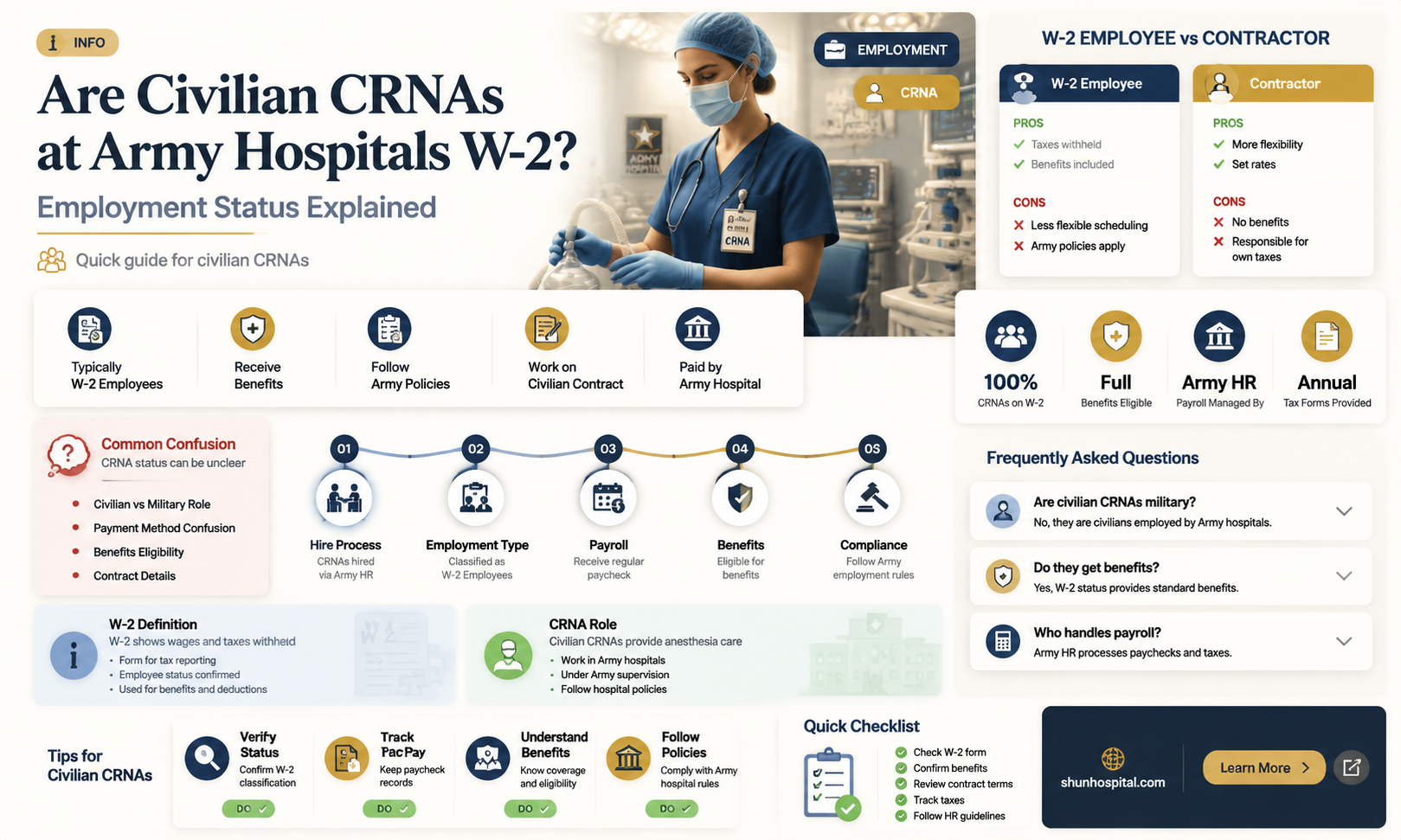

The employment status of civilian Certified Registered Nurse Anesthetists (CRNAs) working at Army hospitals is a topic of interest, particularly regarding their classification as W-2 employees. Civilian CRNAs play a crucial role in providing anesthesia services alongside military personnel, but their contractual arrangements differ from those of active-duty military members. Typically, civilian CRNAs at Army hospitals are employed through contracts with the federal government or third-party agencies, which often categorize them as W-2 employees. This classification means they receive a regular paycheck with taxes withheld, similar to traditional employees, rather than being classified as independent contractors. Understanding this employment structure is essential for CRNAs considering such positions, as it impacts tax obligations, benefits, and legal protections.

| Characteristics | Values |

|---|---|

| Employment Status | Civilian CRNAs at Army hospitals are typically federal employees. |

| Tax Form | They receive a W-2 tax form, as they are classified as employees of the federal government. |

| Employer | U.S. Army Medical Command (MEDCOM) or other military health system entities. |

| Benefits | Eligible for federal employee benefits, including health insurance, retirement plans (e.g., FERS), and paid leave. |

| Salary | Paid through the federal government's payroll system, with salaries determined by the General Schedule (GS) pay scale or equivalent. |

| Job Security | Subject to federal employment protections and regulations, including civil service rules. |

| Union Representation | May be represented by federal employee unions, depending on the specific hospital and location. |

| Contract Type | Full-time, part-time, or temporary positions, depending on the hiring needs of the Army hospital. |

| Tax Withholding | Federal, state, and Social Security taxes are withheld from their paychecks, as with other W-2 employees. |

| Retirement | Participate in the Federal Employees Retirement System (FERS) or, in some cases, the Civil Service Retirement System (CSRS). |

| Leave Accrual | Accrue annual and sick leave based on federal employee guidelines. |

| Hiring Process | Must go through the federal hiring process, including background checks and security clearances. |

| Job Classification | Classified as healthcare professionals under the federal government's occupational series. |

| Portability of Benefits | Benefits may be transferable if they move to another federal position. |

| Performance Evaluations | Subject to federal performance evaluation systems, such as the Performance Management Appraisal Program (PMAP). |

| Continuing Education | May have access to federal funding or programs for continuing education and professional development. |

Explore related products

What You'll Learn

![]()

Employment Status of Civilian CRNAs

The employment status of civilian Certified Registered Nurse Anesthetists (CRNAs) working at Army hospitals is a nuanced topic that requires careful examination of their contractual and tax obligations. Civilian CRNAs employed in military healthcare facilities often fall under specific employment classifications that distinguish them from both active-duty military personnel and traditional private-sector employees. These individuals are typically hired through contracts managed by the U.S. Department of Defense (DoD) or its affiliated agencies, such as the Defense Health Agency (DHA). Understanding whether they are classified as W-2 employees is essential for tax purposes, benefits eligibility, and legal protections.

Civilian CRNAs at Army hospitals are generally considered W-2 employees, meaning their employers withhold federal and state taxes, Social Security, and Medicare contributions from their paychecks. This classification is consistent with their status as federal employees or contractors working under the authority of the DoD. Unlike independent contractors, who receive a 1099 form, W-2 employees are subject to greater employer control and are entitled to certain benefits, such as health insurance, retirement plans, and paid leave. The W-2 designation also ensures that these CRNAs are covered under the Federal Employees' Compensation Act (FECA) for work-related injuries or illnesses.

The employment contracts for civilian CRNAs often specify their roles, responsibilities, and compensation packages, which align with federal employment guidelines. These contracts may be managed through third-party staffing agencies or directly by the DoD, but the W-2 status remains consistent. It is important for CRNAs to review their employment agreements to understand the terms of their engagement, including whether they are classified as federal employees or contractors. This distinction can impact their eligibility for certain federal benefits, such as the Thrift Savings Plan (TSP) or access to the Federal Employees Health Benefits (FEHB) program.

While civilian CRNAs at Army hospitals are typically W-2 employees, there may be exceptions based on the specific terms of their contracts. For instance, some CRNAs might be hired on a temporary or part-time basis, which could alter their employment classification. In such cases, it is crucial for individuals to consult with their employers or a tax professional to determine their correct tax status and ensure compliance with IRS regulations. Additionally, CRNAs should be aware of any state-specific tax laws that may apply, as these can vary depending on their primary work location.

In summary, civilian CRNAs working at Army hospitals are generally classified as W-2 employees, reflecting their federal employment or contractual relationship with the DoD. This status provides them with tax withholding, benefits, and legal protections akin to those of other federal workers. However, CRNAs must carefully review their employment contracts to confirm their classification and understand the implications for their taxes and benefits. By doing so, they can ensure compliance with federal and state regulations while maximizing their professional and financial security.

Newborn Care: Hospitals' Least Profitable Service

You may want to see also

Explore related products

![]()

W-2 Classification in Army Hospitals

Civilian Certified Registered Nurse Anesthetists (CRNAs) working in Army hospitals often find themselves navigating the complexities of employment classification, particularly whether they are considered W-2 employees. Understanding the W-2 classification is crucial for these professionals, as it impacts their tax obligations, benefits, and legal rights. In Army hospitals, civilian CRNAs are typically employed under specific government contracts or agreements, which dictate their employment status. The W-2 classification is generally applicable to employees who receive a regular wage, have taxes withheld by their employer, and are subject to the employer’s control over their work. For civilian CRNAs, this classification is often relevant because they are integrated into the hospital’s workforce, performing essential anesthesia services alongside military personnel.

The determination of W-2 status for civilian CRNAs in Army hospitals hinges on several factors, including the terms of their employment contract and the nature of their work. These professionals are usually hired through federal programs or staffing agencies that contract with the military, and their employment agreements often specify whether they are classified as employees or independent contractors. Since Army hospitals operate under federal guidelines, civilian CRNAs are more likely to be treated as W-2 employees rather than 1099 contractors. This is because the government typically prefers clear employment relationships to ensure compliance with labor laws and to maintain control over the workforce. As W-2 employees, civilian CRNAs benefit from tax withholdings, eligibility for certain federal benefits, and protections under labor laws.

One key aspect of W-2 classification for civilian CRNAs is the tax implications. As W-2 employees, their employers (often the federal government or a contracting agency) are responsible for withholding federal and state income taxes, Social Security, and Medicare taxes from their paychecks. This simplifies the tax filing process for CRNAs, as they receive a W-2 form at the end of the year summarizing their earnings and withholdings. In contrast, independent contractors receive a 1099 form and are responsible for paying their own taxes, including self-employment taxes. For civilian CRNAs, the W-2 classification provides financial stability and reduces the administrative burden associated with tax compliance.

Another important consideration is the eligibility for benefits and protections afforded to W-2 employees. Civilian CRNAs classified under W-2 status may qualify for federal employee benefits, such as health insurance, retirement plans, and paid leave, depending on their specific employment agreement. Additionally, they are covered under workers’ compensation and unemployment insurance, which provides a safety net in case of injury or job loss. These benefits are not typically available to independent contractors, making W-2 classification more advantageous for civilian CRNAs working in Army hospitals. It also ensures they are protected under federal labor laws, including those related to minimum wage, overtime, and workplace safety.

In conclusion, civilian CRNAs working in Army hospitals are generally classified as W-2 employees due to the nature of their employment contracts and the federal guidelines governing military healthcare facilities. This classification offers them significant advantages, including tax withholdings, eligibility for federal benefits, and legal protections. While the specifics may vary depending on the terms of their contract, understanding their W-2 status is essential for these professionals to manage their finances, access benefits, and ensure compliance with federal regulations. For civilian CRNAs, clarity on their employment classification is a critical aspect of their role in supporting military healthcare operations.

Hospitality Room Essentials: A Complete Guide

You may want to see also

Explore related products

![]()

Civilian vs. Military Employee Benefits

When comparing Civilian vs. Military Employee Benefits in the context of civilian CRNAs (Certified Registered Nurse Anesthetists) working at Army hospitals, it’s essential to understand the distinctions in employment status and the associated benefits. Civilian CRNAs employed at Army hospitals are typically W-2 employees, meaning they are classified as federal civilian employees rather than military personnel. This classification significantly impacts their benefits package, which differs from that of active-duty military members. Civilian employees receive benefits through the federal government’s civilian employee system, including health insurance, retirement plans (such as the Federal Employees Retirement System, FERS), and paid leave. These benefits are structured similarly to those of other federal workers but differ from the military’s active-duty benefits.

One key difference in Civilian vs. Military Employee Benefits is the retirement system. Civilian CRNAs contribute to FERS, which includes a pension, Social Security, and the Thrift Savings Plan (TSP), a 401(k)-style retirement savings plan. In contrast, military personnel participate in the military retirement system, which offers a pension after 20 years of service but does not include Social Security contributions. Additionally, military members have access to the Blended Retirement System (BRS), which combines a pension with a government contribution to the TSP. Civilian employees, however, do not have access to the military’s defined benefit pension after 20 years, making their retirement planning more aligned with traditional federal civilian employment.

Health insurance is another area where Civilian vs. Military Employee Benefits diverge. Civilian CRNAs at Army hospitals are eligible for the Federal Employees Health Benefits (FEHB) program, which offers a variety of health insurance plans. Military personnel, on the other hand, receive healthcare through TRICARE, a military-specific health insurance program. While both systems provide comprehensive coverage, TRICARE is tailored to the needs of active-duty service members and their families, often with lower out-of-pocket costs. Civilian employees must choose and pay premiums for their FEHB plans, though the government contributes a portion of the cost.

Paid leave and work-life balance also differ between civilian and military employees. Civilian CRNAs accrue annual and sick leave based on federal guidelines, typically starting with 13 days of annual leave per year, increasing with tenure. Military personnel, however, do not accrue leave in the same way; instead, they receive 30 days of paid leave annually, regardless of rank or years of service. Additionally, military members may be subject to deployment or relocation, which can impact their work-life balance, whereas civilian employees generally have more stability in their assignments.

Lastly, Civilian vs. Military Employee Benefits extend to additional perks and considerations. Civilian CRNAs may have access to federal employee discounts, flexible work schedules, and job security protections under federal employment laws. Military personnel, however, receive benefits such as commissary and exchange privileges, housing allowances, and access to military bases’ amenities. Civilian employees do not receive these military-specific perks but benefit from the stability and protections of federal civilian employment. Understanding these differences is crucial for CRNAs considering positions at Army hospitals, as it directly impacts their compensation, retirement planning, and overall job satisfaction.

Tourism & Hospitality: Unique Challenges and Opportunities in a People-Centric Industry

You may want to see also

Explore related products

![]()

Tax Implications for CRNAs

Civilian CRNAs working at Army hospitals often find themselves in a unique employment situation, which can have significant tax implications. As W-2 employees, these CRNAs are subject to the same federal tax laws as other employees, but their specific circumstances may offer certain advantages or complexities. Understanding these tax implications is crucial for financial planning and compliance.

Firstly, as W-2 employees, civilian CRNAs at Army hospitals have federal income taxes, Social Security, and Medicare taxes automatically withheld from their paychecks. This simplifies the tax filing process, as they typically receive a W-2 form at the end of the year, summarizing their earnings and withholdings. However, it’s important to review this form for accuracy to avoid discrepancies when filing taxes. Additionally, these CRNAs may be eligible for certain tax deductions or credits, such as the student loan interest deduction or the Child and Dependent Care Credit, depending on their personal situation.

One notable tax advantage for civilian CRNAs working in Army hospitals is the potential exclusion of certain income from federal taxes. For instance, if they are stationed overseas or in specific designated zones, a portion of their income may qualify for the Foreign Earned Income Exclusion (FEIE). This exclusion allows individuals to exclude up to a certain amount of their foreign-earned income from U.S. taxes, reducing their overall tax liability. However, eligibility for this exclusion depends on meeting specific criteria, such as the Physical Presence Test or the Bona Fide Residence Test.

Another consideration is state taxation. While federal taxes are consistent across the U.S., state tax laws vary widely. Civilian CRNAs working at Army hospitals may be subject to state income tax in the state where they work, their state of residency, or both, depending on tax reciprocity agreements. Some states offer tax exemptions or credits for military-related income, which could apply to civilian employees working in military facilities. It’s essential to research the specific state tax laws to ensure compliance and optimize tax savings.

Lastly, retirement planning and tax-advantaged accounts are important considerations for CRNAs. As W-2 employees, they typically have access to employer-sponsored retirement plans, such as a 401(k) or Thrift Savings Plan (TSP), which offer tax-deferred growth or tax-free withdrawals in retirement. Contributing to these plans can reduce taxable income in the current year while saving for the future. Additionally, CRNAs may consider Health Savings Accounts (HSAs) if they have a high-deductible health plan, as HSAs provide triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

In summary, civilian CRNAs at Army hospitals, as W-2 employees, face a mix of standard and unique tax implications. Understanding federal and state tax obligations, exploring exclusions like the FEIE, and leveraging tax-advantaged retirement and health savings accounts are key strategies for managing their tax liabilities effectively. Consulting a tax professional familiar with military-related employment can provide personalized guidance tailored to their specific circumstances.

Hospitals' Charitable Donations: Who Benefits and Why?

You may want to see also

Explore related products

![]()

Contractual Agreements in Military Settings

In military settings, contractual agreements play a crucial role in defining the employment status and responsibilities of civilian personnel working within military institutions, such as Certified Registered Nurse Anesthetists (CRNAs) at Army hospitals. Civilian CRNAs employed in these settings often operate under specific contractual arrangements that outline their roles, compensation, benefits, and tax obligations. One of the primary questions that arises is whether these civilian CRNAs are classified as W-2 employees. Based on available information, civilian CRNAs at Army hospitals are typically considered W-2 employees, meaning their employers withhold federal and state taxes, Social Security, and Medicare from their paychecks. This classification ensures compliance with tax regulations and provides these professionals with certain employment protections and benefits.

The contractual agreements for civilian CRNAs in military settings are usually established through partnerships between the Department of Defense (DoD) and civilian staffing agencies or direct hiring by military medical facilities. These contracts are designed to meet the unique demands of military healthcare, ensuring that CRNAs provide critical anesthesia services to military personnel, veterans, and their families. The agreements often include provisions for competitive salaries, health insurance, retirement plans, and other benefits comparable to those of military personnel. Additionally, these contracts may specify the duration of employment, work hours, and deployment requirements, if applicable, to align with the operational needs of the military.

Taxation is a key component of these contractual agreements, as it directly impacts the employment classification of civilian CRNAs. As W-2 employees, they receive a Form W-2 at the end of the tax year, which reports their annual wages and the taxes withheld. This contrasts with independent contractors, who receive a Form 1099 and are responsible for their own tax payments. The W-2 classification for civilian CRNAs reflects their status as employees of the military healthcare system, even though they are not active-duty military personnel. This distinction is important for understanding their legal rights, tax obligations, and eligibility for benefits such as unemployment insurance and workers' compensation.

Another critical aspect of contractual agreements in military settings is the scope of practice for civilian CRNAs. These agreements clearly define the clinical responsibilities and authority of CRNAs, ensuring they operate within the guidelines of both civilian healthcare standards and military medical protocols. The contracts may also include provisions for continuing education, licensure maintenance, and adherence to military-specific training requirements. This ensures that civilian CRNAs remain competent and prepared to deliver high-quality care in the unique context of military healthcare.

Finally, contractual agreements in military settings often address liability and malpractice coverage for civilian CRNAs. Given the high-stakes nature of military healthcare, these contracts typically provide malpractice insurance through the Federal Tort Claims Act (FTCA) or other government-sponsored programs. This protects civilian CRNAs from personal liability while performing their duties and ensures that patients have recourse in the event of medical errors. Understanding these contractual provisions is essential for civilian CRNAs to navigate their roles effectively and with confidence in Army hospitals.

In summary, contractual agreements in military settings are meticulously structured to define the employment status, responsibilities, and benefits of civilian CRNAs working in Army hospitals. These agreements classify civilian CRNAs as W-2 employees, ensuring proper tax withholding and access to employment benefits. By addressing taxation, scope of practice, and liability, these contracts provide a clear framework for civilian CRNAs to contribute to military healthcare while safeguarding their professional and legal interests.

Locating Clinic G: A Guide to Aintree Hospital's Layout

You may want to see also

Frequently asked questions

Yes, civilian CRNAs working at Army hospitals are typically classified as W-2 employees, as they are employed by the federal government or its contractors.

No, civilian CRNAs receive federal employee benefits, which differ from military benefits. They are not entitled to military-specific perks like housing allowances or GI Bill benefits.

No, civilian CRNAs are not subject to military orders or deployments. They are civilian employees and do not serve in a military capacity.

Civilian CRNAs receive a W-2 form for tax purposes, as they are employees of the federal government or its contractors, and their taxes are withheld accordingly.

Yes, civilian CRNAs can apply to join the military as CRNAs, but they must meet military eligibility requirements and complete the necessary enlistment or commissioning process.