It can be challenging to keep track of medical bills, especially when you've received care from multiple providers. To check if you owe a hospital, you can start by logging into the hospital's online portal, where you may be able to view any outstanding balances. You can also contact the hospital directly and ask if they can review your financial situation and consider waiving part or all of the bill. If you have health insurance, it's worth contacting your insurance company, as they may have records of any medical bills they've partially paid or can provide information on outstanding payments. Checking your credit reports from major credit bureaus is another way to identify any unpaid medical debts, as these reports will include entries from collection agencies, detailing the original creditor and the amount owed. It's important to address unpaid medical bills promptly, as they can negatively impact your credit score and lead to legal consequences if left unresolved.

| Characteristics | Values |

|---|---|

| Checking credit reports | Check credit reports from all three credit bureaus (Equifax, Experian, and Transunion) to identify any unpaid medical debt. |

| Online portals | Log into hospital or healthcare provider online portals to check for any outstanding medical balances. |

| Contact hospitals/clinics | Contact hospitals or clinics directly and provide basic information to inquire about any outstanding payments. |

| Contact insurance company | Reach out to your insurance company to review records of any medical bills they have paid or partially paid. |

| Review bills | Review medical bills closely to ensure accuracy and dispute any errors or discrepancies. |

| Payment plans | Discuss payment plans or financial assistance programs with the hospital or healthcare provider if you are unable to pay the full amount. |

| Debt collection rights | Understand your rights regarding debt collection practices, such as verifying the debt and disputing inaccurate information. |

Explore related products

What You'll Learn

![]()

Check your credit reports from major credit bureaus

Checking your credit reports from major credit bureaus is an important step in maintaining your financial health. Credit reports play a significant role in your financial life, and it's crucial to review them regularly to ensure accuracy and protect your credit history. Here are some detailed steps and information to guide you through the process:

Understanding Credit Reports and Their Impact

Credit reports are comprehensive records of your credit history. They include information about your existing credit, such as credit card accounts, mortgages, car loans, and student loans. Additionally, they may contain public records, court judgments, tax liens, and inquiries about you. Personal information, such as your name, address, Social Security number, date of birth, and employment details, is also included in credit reports. This information is used by lenders, employers, landlords, and insurance providers to make decisions about loan approvals, credit card applications, rentals, and insurance offerings. Therefore, maintaining a positive credit history is essential for your financial well-being.

Obtaining Your Credit Reports

You are entitled to receive free credit reports from the three major credit reporting agencies: Equifax, Experian, and TransUnion. Federal law directs you to access these reports through AnnualCreditReport.com or by calling 877-322-8228. You can request free weekly or annual credit reports from each of these agencies. It is recommended to stagger your requests throughout the year to continuously monitor the accuracy and completeness of the information.

Reviewing and Disputing Credit Reports

When reviewing your credit reports, pay close attention to the details. Check for suspicious activities, unfamiliar accounts, late payments, and any discrepancies. If you identify errors or signs of potential fraud or identity theft, you have the right to dispute the information. Each credit reporting agency provides dispute instructions on their website or over the phone. You can also contact the business that supplied the information to initiate the correction process. Regularly reviewing your credit reports helps you catch problems early and ensures that your credit remains in good standing when you need it.

Protecting Your Credit and Identity

In addition to checking your credit reports, consider taking proactive measures to protect your credit and identity. Some credit bureaus offer credit monitoring and identity theft protection services for a fee. These services can help you keep informed about changes to your credit report and safeguard your personal information. However, always remember that checking your own credit will not harm your credit score.

Maintaining Good Credit Practices

Maintaining good credit involves responsible financial habits. This includes making timely payments, managing your debt effectively, and being mindful of hard inquiries when applying for new credit or loans. Understanding how your credit behaviour impacts your credit score is essential for building and maintaining a strong financial profile.

Remember, checking your credit reports from major credit bureaus is a crucial step in financial management. By following the steps outlined above, you can proactively monitor your credit health, dispute inaccuracies, and protect your financial well-being.

Palliative Care: Home or Hospital?

You may want to see also

Explore related products

![]()

Contact the hospital's billing department

If you are unsure whether you owe a hospital money, one of the best things you can do is contact the hospital's billing department directly. Hospitals are often made up of many different departments, each billing patients separately, so you may receive multiple bills for a single hospital stay.

When you contact the billing department, they will be able to tell you whether you have an existing account with them and whether you owe them any money. They may ask you for some basic information to check their records, such as your name, birth date, and address.

If you have received treatment from multiple providers, it can be hard to keep track of all the different bills. In this case, it is a good idea to call the hospital and ask them who else may be billing you for their services. Then, you can call those entities to ask what they are charging you for. Once you have all the bills in front of you, you can add up the total amount you owe.

If you are unable to pay the bill, you can ask the hospital about financial assistance programs or payment plans. Nonprofit hospitals are required by law to offer financial assistance, and many other providers are willing to work out payment arrangements. You can also contact your state or local social services to see if more help is available.

If you have health insurance, it is a good idea to contact your insurance company to see if they have a record of any medical bills they have paid partially. This can help you get an idea of which healthcare provider to start with when looking for an unpaid bill.

Conquering Municipal Hospital: Zero City

You may want to see also

Explore related products

![]()

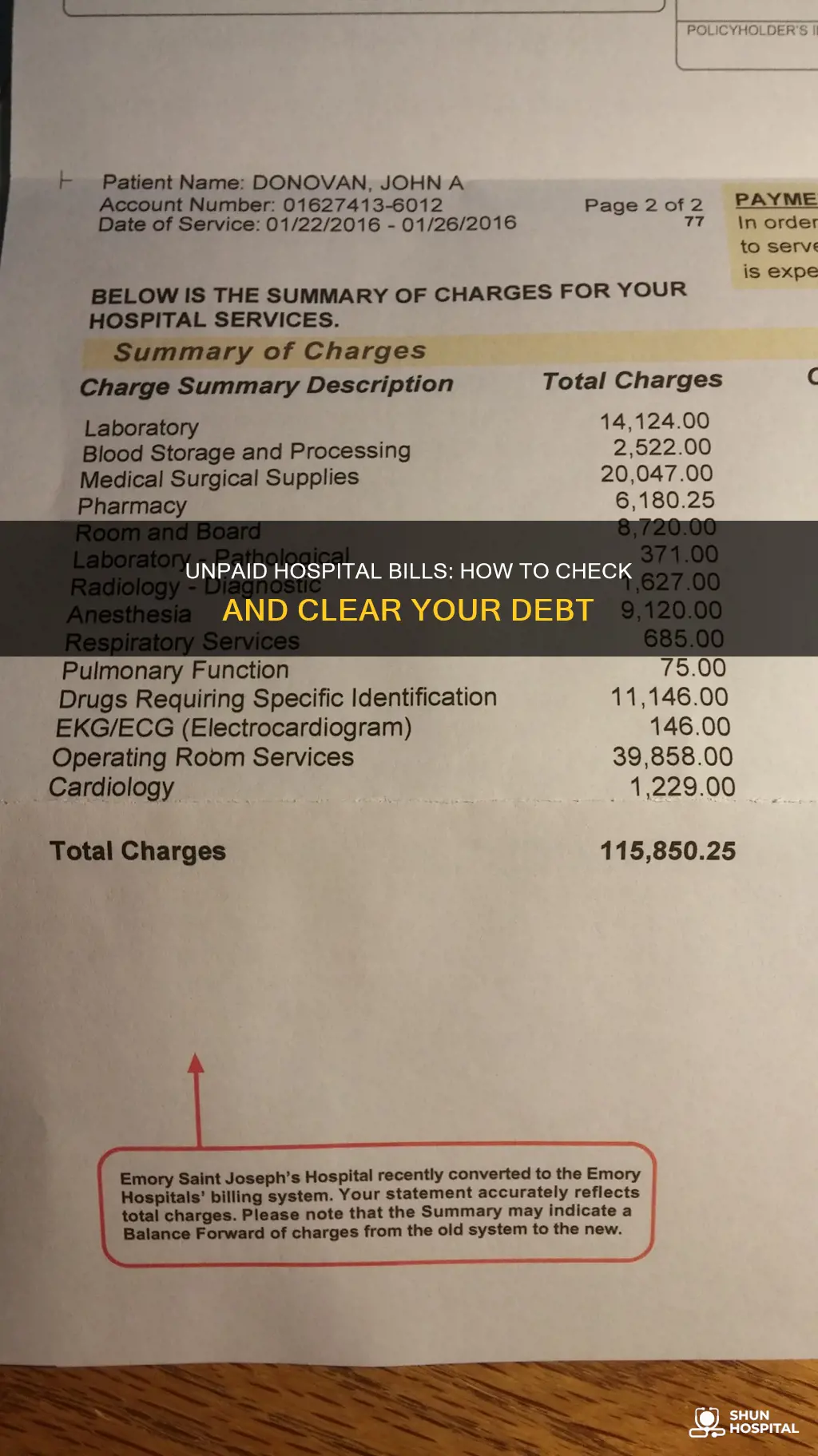

Review your medical bill

Receiving a medical bill can be overwhelming, but reviewing it thoroughly can help you identify errors and save money. Here are some detailed steps to guide you through the process of reviewing your medical bill:

Understand the Components of Your Medical Bill

Medical bills typically include basic information such as the services or procedures you received and the dates of service. Each service or supply provided will have an associated cost, and you will be able to see the total amount you owe. Keep in mind that you may receive separate bills from different specialists involved in your care, such as surgeons, radiologists, or anesthesiologists.

Compare with Explanation of Benefits (EOB)

Before paying your medical bill, it is crucial to compare it with the Explanation of Benefits (EOB) provided by your health insurance company. The EOB outlines the services or supplies covered by your plan and the corresponding costs. Make sure the charges on your bill match the information on the EOB. If you have insurance, check the amount your insurance company is expected to pay and your share of the cost.

Check for Errors and Discrepancies

Medical billing errors are common, and it's important to review your bill for any inaccuracies. Look out for coding errors, duplicate charges, incorrect dates of service, or unwarranted charges for services you didn't receive. Compare the procedures, dates, and providers on your bill with your medical records to ensure accuracy. If you notice any discrepancies, contact your provider's billing department to clarify or correct the errors.

Understand Billing Codes

Medical bills often use complex billing codes that can be challenging to interpret. If you don't understand a particular code, you can look up its description by searching for the code along with the term "medical billing code." Compare the descriptions to the services you received, and don't hesitate to contact the billing department if there are inconsistencies.

Consider Using a Medical Bill Review Service

If you find the process overwhelming or need additional support, consider utilising a medical bill review service. These services employ qualified experts who review your bill for correctness and ensure you are not being overcharged. They have strong attention to detail and are knowledgeable about medical terminology and billing practices. Medical bill reviews can identify errors and help you avoid unnecessary expenses.

By following these steps and staying organised, you can effectively review your medical bill, protect yourself from unnecessary charges, and make the payment process smoother. Remember that understanding your medical bill is your right and can help you make informed decisions about your healthcare.

El Camino Hospital: Mountain View Healthcare

You may want to see also

Explore related products

![]()

Contact your medical insurance company

If you have medical insurance, contacting your insurance company is a good way to check if you owe the hospital any money. Whenever you seek medical care, the medical provider will ask whether you have insurance, and if you do, they will send some of the bills to the insurance company. Therefore, your insurance company should have a record of any medical bills they paid partially or in full, or they may be able to give you an idea of which healthcare provider to contact about an unpaid bill.

If you have been treated at a certain hospital, you can ask the billing department to check if you have an existing account there. You should also be able to see any medical balances you have left to pay and what they are for by logging into the hospital's online portal. If you cannot pay your bill, talk to the medical care provider. Nonprofit hospitals are required by law to offer financial assistance programs, and many other providers are willing to work out payment arrangements. You could also ask the hospital if they have a way to review your financial situation so that you might be considered for having all or part of the bill waived.

If you have a network of hospitals or healthcare providers that you visit, you may have been instructed to create a login with your email or phone number so that you can log into their online portal. Here, you should be able to see any medical balances you have left to pay and what they are for. If you are unsure if you have a medical bill, you can start your search by logging online to one of these portals.

You can also contact clinics or hospitals where you have received care. With some basic information about yourself, such as your name, birth date, and address, a medical receptionist can tell you whether you owe money to that particular place for medical care.

If you are concerned about your credit score, you can check your credit reports from all three credit bureaus: Equifax, Experian, and Transunion. Unpaid medical debt does not show up on your credit reports, but if it is sent to a debt collector or debt collection agency, it will be part of your credit history and credit reports. You can get a free annual credit report from each of the credit bureaus online.

Danny Thomas: The Man Behind Shriners Hospitals

You may want to see also

Explore related products

![]()

Contact the hospital for financial assistance

If you are facing financial hardship and need assistance with your medical bills, there are several options available to you. Many hospitals and healthcare providers offer financial assistance programs, sometimes known as "charity care," which provide free or discounted healthcare services to those who qualify. These programs are often offered by hospitals, medical care providers, or state governments, and they may be able to help you cover some or all of your medical expenses.

- Reach out to the hospital's billing department: Contact the billing department of the hospital where you received treatment. Explain your financial situation and express your interest in learning about any financial assistance programs they may offer. Ask about their written Financial Assistance Policy (FAP), which hospitals are required to have under the Affordable Care Act (ACA). The FAP should outline eligibility criteria, the application process, and whether the assistance is in the form of free or discounted care.

- Obtain and review the Financial Assistance Policy (FAP): Request a copy of the hospital's FAP, which they are legally required to provide free of charge. This document will outline the details of their financial assistance program, including eligibility requirements and the application process. Review the policy thoroughly to understand the types of assistance offered and whether you may qualify.

- Gather the necessary information for the application: Financial assistance applications typically require information about your income and expenses. Start gathering documents such as tax forms, pay stubs, rent or mortgage statements, utility bills, credit card statements, and other relevant financial information. This information will be used to assess your eligibility for financial assistance.

- Complete and submit the financial assistance application: Using the information you have gathered, carefully complete the financial assistance application form. Be thorough and accurate in your responses, providing all the requested information. Submit the application to the hospital or healthcare provider in a timely manner.

- Follow up on the status of your application: After submitting your application, stay in communication with the hospital's billing department or financial assistance office. Follow up to check the status of your application and provide any additional information they may require. Ask about the expected timeline for receiving a decision on your application.

- Explore other options if assistance is denied: If your application for financial assistance is denied, don't lose hope. You can still explore other options, such as payment plans, applying for Medicaid or Medicare, or seeking assistance from non-profit organizations or advocacy groups. Additionally, you can discuss lower fees or alternative payment options directly with your healthcare provider.

Remember, even if you have health insurance, financial assistance programs can sometimes help cover out-of-pocket expenses. Don't hesitate to reach out and inquire about the options available to you. Dealing with medical bills can be stressful, but taking proactive steps to seek financial assistance can help alleviate some of that burden.

Kaiser Permanente: Student Shadowing Opportunities?

You may want to see also

Frequently asked questions

You can check your credit reports from the three major credit bureaus: Equifax, Experian, and Transunion. If the hospital has sent your bill to a debt collector, it will be part of your credit history and will appear on your credit report.

You can get a free annual credit report from each of the three credit bureaus online.

Contact the hospital's billing department to discuss payment options. Nonprofit hospitals are required by law to offer financial assistance programs, and many other providers are willing to work out payment arrangements. You can also contact your state or local social services to see if more help is available.

You can contact the billing/medical collections department of the hospital to work out a payment plan. You can also hire a billing advocate, similar to a financial advisor, to negotiate and contact medical providers to help save you money and work out a plan to pay off your medical debt.