When it comes to choosing a Medicare plan, it's important to consider your specific needs and preferences. Comparing Medicare Advantage plans requires thinking about your budget, health care requirements, and preferred methods of care. These plans, offered by private insurers, serve as an alternative to Original Medicare, bundling together Medicare Part A (hospital coverage), Part B (medical insurance), and often Part D (drug coverage). To make an informed decision, individuals can utilise the Medicare.gov comparison tool, which provides information on coverage, costs, and benefits for various plan options in their area. This tool allows users to input their regular prescriptions and cross-reference their healthcare providers to determine the most suitable plan. Additionally, it is essential to review the plan's website and understand all the terms before signing up.

| Characteristics | Values |

|---|---|

| Budget | Consider your budget and the plan's premiums, out-of-pocket costs, and limits. |

| Health Care Needs | Think about your specific health care needs, including medications, and how you prefer to receive care (e.g., through specialists or a primary care physician). |

| Provider Network | Cross-reference your preferred healthcare providers to ensure they are included in the plan's network. |

| Plan Coverage | Utilize the plan comparison tool on Medicare.gov or private comparison sites to determine coverage for your regular prescriptions and other specific needs. |

| Plan Benefits | Consider the additional benefits offered, such as coverage for hearing, dental, and vision care, as well as any cost-sharing or extra benefits beyond Original Medicare. |

| Plan Type | Decide between Original Medicare (Parts A and B) and Medicare Advantage Plans (Part C), which bundle different coverage options and may offer more flexibility or restrictions. |

| Plan Details | Visit the plan's website to understand all the fine print and terms before signing up. |

Explore related products

What You'll Learn

![]()

Compare costs and coverage using Medicare.gov's online tool

Medicare Advantage plans are an alternative to Original Medicare, which is offered by private insurers that have been approved by Medicare. These plans include Medicare Part A (hospital coverage), Medicare Part B (medical insurance), and usually Medicare Part D (drug coverage).

When comparing Medicare plans, it is important to consider your budget, health care needs, and personal preferences for receiving care. The plan comparison tool on Medicare.gov allows you to compare costs and coverage of different plans. You can enter your regular prescriptions to determine plan coverage and costs. Additionally, you can cross-reference your healthcare providers to ensure they are included in the plan's network.

Before selecting a plan, it is recommended to review the plan's website and understand all the associated terms and conditions. Medicare Advantage plans may offer lower premiums, limits on out-of-pocket costs, and additional benefits such as coverage for hearing, dental, and vision care. However, they may also restrict your freedom to choose medical providers and require you to stay within the plan's geographic service area.

Medicare.gov's online tool provides specific cost information for different plan types, allowing you to download and print a table for reference. This tool empowers you to make informed decisions about your healthcare coverage by providing comprehensive insights into the costs and coverage associated with Medicare Advantage plans.

Switching Hospitals During Pregnancy: What You Need to Know

You may want to see also

Explore related products

![]()

Consider your budget and health needs

When comparing Medicare plans, it's important to consider your budget and health needs. This involves evaluating the costs associated with different plans and ensuring that your specific healthcare requirements will be covered. Here are some key factors to keep in mind:

Understand the Different Types of Medicare Plans

Medicare offers various plans, each with its own coverage and cost structure. Familiarize yourself with the options, such as Original Medicare (Parts A and B), Medicare Advantage Plans (Part C), Medicare Part D (drug coverage), and Medigap (Medicare Supplement Insurance). Each type of plan has different benefits and limitations, so understanding these will help you make an informed decision based on your budget and health needs.

Evaluate the Costs

Consider the specific costs associated with each plan. Review the premiums, deductibles, copayments, and out-of-pocket expenses. Medicare Advantage Plans, for example, may offer lower premiums and limits on out-of-pocket costs. In contrast, Original Medicare with a Medigap policy may provide more flexibility in choosing healthcare providers but could result in higher out-of-pocket costs in certain years. Examine your financial situation and determine which cost structure aligns better with your budget.

Analyze Coverage and Benefits

Different Medicare plans offer varying levels of coverage and benefits. Consider your specific health needs, including hospital coverage, medical insurance, and drug coverage. For example, if you require regular prescription medications, look for plans that include Medicare Part D or offer additional benefits like coverage for hearing, dental, and vision care. Review the specific benefits of each plan to ensure they align with your health needs and budget.

Compare Plan Details

Utilize the plan comparison tool on Medicare.gov to compare different Medicare plans. Enter your regular prescriptions to determine plan coverage and cost. Cross-reference your healthcare providers to ensure they are included in the plan's network. Review the fine print and understand the limitations and requirements of each plan, such as geographic restrictions or referral processes for specialist visits.

Choose a Plan that Fits Your Needs

Ultimately, the best Medicare plan for you is one that balances your budget and health needs. Consider how you prefer to receive care and the frequency of your healthcare visits. If you require frequent specialist visits, a plan with more flexibility in provider choice might be preferable. On the other hand, if you primarily visit your primary care physician, a more affordable plan with limited provider choices may suffice.

Remember, there is no one-size-fits-all approach to choosing a Medicare plan. By carefully considering your budget and health needs, you can make a well-informed decision that provides you with the coverage and benefits that are most suitable for your situation.

Hospital Care on Cruise Ships: What's the Deal?

You may want to see also

Explore related products

![]()

Check if your preferred healthcare providers are included in the plan

When comparing Medicare plans, it's essential to check if your preferred healthcare providers are included in the plan's network. This includes confirming that your doctors, specialists, hospitals, and even pharmacies are part of the network. Here are some detailed steps to guide you through this process:

First, understand that different types of Medicare plans have varying provider networks. For instance, Original Medicare (Part A and Part B) offers broad access to healthcare providers across the nation, and over 90% of US healthcare providers accept it. On the other hand, Medicare Advantage Plans (Part C) are typically offered as Health Maintenance Organizations (HMOs) or Preferred Provider Organizations (PPOs), each with its own network of doctors, hospitals, and providers.

Second, identify the specific type of Medicare Advantage Plan you are considering. Some plans, like Special Needs Plans (SNPs), require you to use doctors and hospitals within their network, except in emergencies or for urgent care. Other plans may offer more flexibility, allowing you to use out-of-network providers at a higher cost. It's crucial to check the specific rules and restrictions of each plan.

Third, verify if your preferred healthcare providers are in the plan's network. You can do this by contacting the insurance company offering the Medicare Advantage Plan or checking their website. Additionally, you can ask your preferred providers directly if they accept the specific Medicare Advantage Plan you are considering.

Finally, consider the financial implications of using in-network versus out-of-network providers. In-network providers typically offer more cost-effective options, resulting in lower out-of-pocket expenses for you. Out-of-network care, while sometimes possible, usually comes with higher costs and less coordination in your healthcare management.

By following these steps, you can make an informed decision about whether your preferred healthcare providers are included in the Medicare plan you are considering, ensuring that your healthcare needs and personal preferences are met.

The Truth Behind the Meaning of "Hospital

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Understand the limitations of Medicare Advantage plans

Medicare Advantage plans are an alternative to Original Medicare, offered by private insurers. While they can be attractive due to their supplemental benefits and low premiums, there are several limitations and trade-offs to consider. Firstly, you may face restrictions on your choice of medical providers and have less freedom to choose your doctors, specialists, and facilities. Medicare Advantage plans often require you to stick with the doctors in the plan's network, and you may incur higher out-of-network care costs. Additionally, you are more likely to need pre-approval for expensive care, and your plan can change unexpectedly, including the benefits offered and the providers covered.

Another limitation is the geographical restriction on non-emergency medical care. Medicare Advantage plans typically require you to live and receive your non-emergency medical treatment within the plan's geographic service area. This can impact your access to care if you travel outside of the state. Switching plans or back to Original Medicare with Medigap can be difficult. There may be limitations on your ability to change plans later, and you might face restrictions on care access and benefits.

Out-of-pocket costs can be a significant consideration with Medicare Advantage plans. While there are limits on these costs, in years with major medical situations, you may still need to pay a substantial amount out of pocket. Additionally, Medicare Advantage plans may have higher out-of-pocket costs compared to Original Medicare, especially if you require specialized or out-of-network care. Prior authorization requirements are also more common with Medicare Advantage. In 2023, about two out of every one hundred enrollees had to obtain prior authorization, and of those requests, 3.2 million resulted in full or partial denial.

When comparing Medicare Advantage plans, it is crucial to consider your budget, health care needs, and preferred method of receiving care. Utilize tools like Medicare.gov and private comparison sites to cross-reference your health care providers and determine the coverage and costs associated with your regular prescriptions. Understanding the limitations and trade-offs of Medicare Advantage plans will help you make an informed decision about your health care coverage.

VA Hospitals: Non-Profit Healthcare for Veterans

You may want to see also

Explore related products

![]()

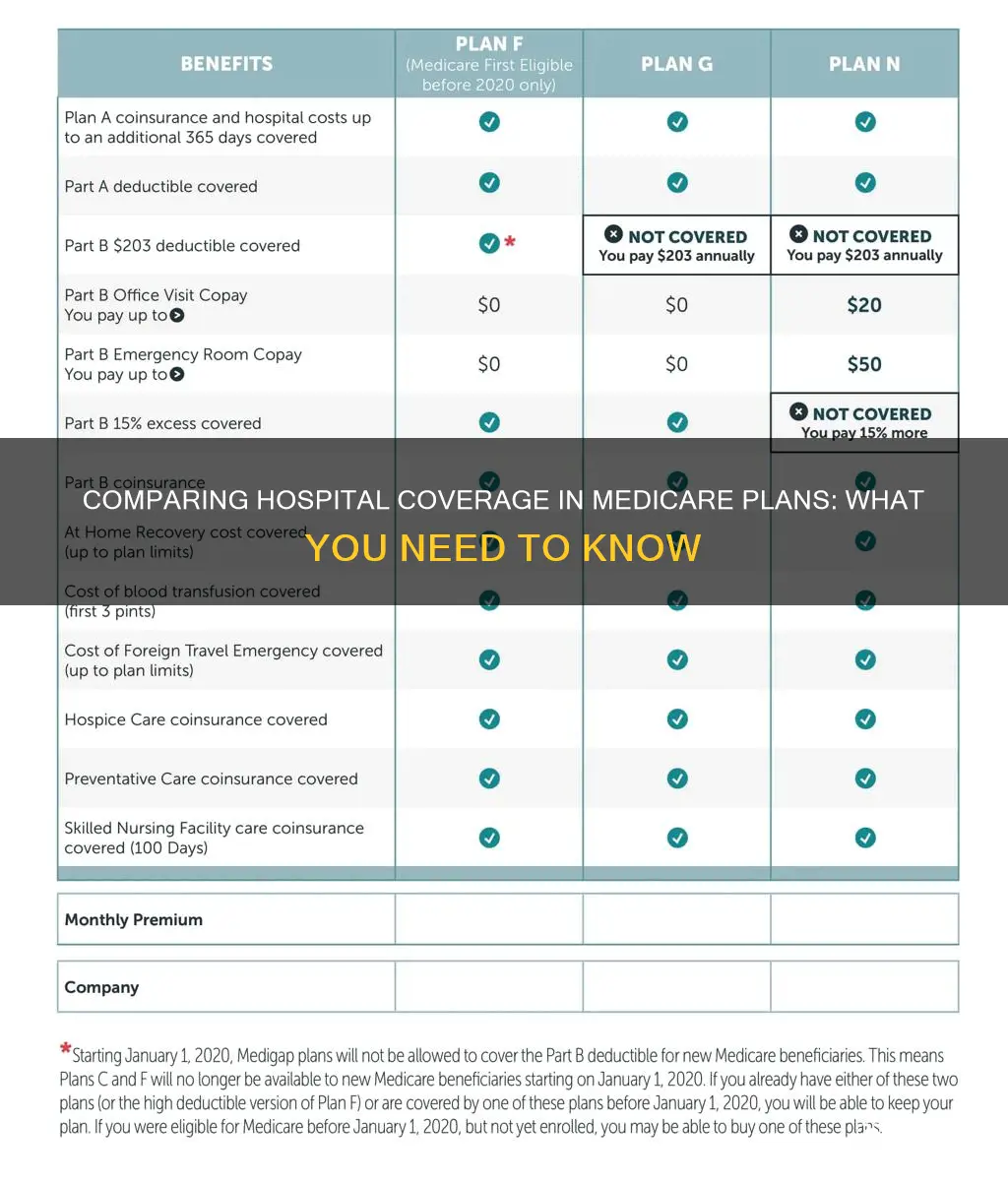

Compare Medigap plans and their benefits

Medicare Supplement insurance plans, also known as Medigap plans, help with some of the out-of-pocket expenses not covered by Original Medicare. Medigap plans work with your Medicare Part A (hospital stays) and Medicare Part B (doctor visits) to lower the out-of-pocket medical costs that Original Medicare doesn't cover.

There are ten standardized Medicare Supplement plans, lettered A–N, each covering a different set of gaps in Medicare. The plan that is right for you will depend on your medical needs and budget, as each plan's premium and coverage vary. Some Medigap plans will have higher premiums and offer more coverage.

Medigap Plan B covers everything that Plan A covers, but it also includes the Medicare Part A hospital deductible. Plan B is a Medigap plan that pays after Medicare pays. Don't confuse it with Part B, which is part of your Original Medicare benefits that pay for outpatient medical. Medigap Plan C is one of the most comprehensive supplements. It covers everything except Medicare excess charges. This means it pays both your deductibles and the 20% that you would normally owe toward all outpatient expenses. Plan D covers most things but does not pay the Part B deductible or any Medicare excess charges. Medigap Plan F has long been the most popular Medigap plan, but Plan C and Plan F are no longer available to anyone new to Medicare after January 1, 2020. Plans K and L are cost-sharing plans offering lower monthly premiums. The premiums are typically lower because, for some services, they pay a percentage of the coinsurance instead of the full amount. Once the out-of-pocket limit is reached, these plans pay 100% of covered services for the rest of the calendar year. Plan N covers the Medicare Part B coinsurance, but you pay copayments for covered doctor office and emergency room visits.

To compare Medigap plans, you can use the Medicare Supplement Plans comparison chart, which is published by Medicare each year. The Centers for Medicare and Medicaid Services updates the Medigap plans comparison chart annually, although most plans do not have benefit changes from year to year. You can also use the plan comparison tool on Medicare.gov and some private comparison sites to enter your regular prescriptions to help determine plan coverage and cost.

Becoming a Hospital Chaplain: Education, Skills, and Personal Qualities

You may want to see also

Frequently asked questions

You can compare Medicare plans and their hospital coverage using the online searchable tool on the Medicare.gov website. This allows you to compare coverage, costs, and benefits in your area. You can also enroll in a Medicare Advantage plan or a Medicare Part D plan on the same website.

Original Medicare includes Medicare Part A (hospital insurance) and Part B (medical insurance). Medicare Advantage plans are offered by private insurers and include Medicare Part A, Part B, and usually Part D (drug coverage). Medicare Advantage plans often have lower premiums and out-of-pocket costs but offer less freedom to choose your medical providers.

You should consider your budget, health care needs, and how you like to receive care. Think about your regular prescriptions, your network of caregivers and medical facilities, and whether you frequently see specialists.

Plan F and Plan G offer a high-deductible plan in some states. However, Plan F is not available if you turned 65 on or after January 1, 2020.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)